- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Asian Companies That May Be Priced Below Intrinsic Value In July 2026

Amidst renewed geopolitical tensions and energy market volatility, Asian markets have shown mixed performance, with some sectors experiencing sharp rallies while others face challenges. In this environment, identifying stocks that may be priced below their intrinsic value can offer potential opportunities for investors seeking to capitalize on market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | HK$19.28 | HK$38.12 | 49.4% |

| Rakuten Bank (TSE:5838) | ¥5809.00 | ¥11507.47 | 49.5% |

| Rakus (TSE:3923) | ¥1019.00 | ¥2014.24 | 49.4% |

| Moshi Moshi Retail Corporation (SET:MOSHI) | THB39.00 | THB75.90 | 48.6% |

| Laopu Gold (SEHK:6181) | HK$385.20 | HK$746.36 | 48.4% |

| Huatu Cendes (SZSE:300492) | CN¥23.09 | CN¥45.69 | 49.5% |

| GreenEnergy (TSE:1436) | ¥1387.00 | ¥2707.83 | 48.8% |

| CSPC Innovation Pharmaceutical (SZSE:300765) | CN¥37.55 | CN¥74.24 | 49.4% |

| Citicore Renewable Energy (PSE:CREC) | ₱4.39 | ₱8.48 | 48.2% |

| BEAUTY GARAGE (TSE:3180) | ¥1438.00 | ¥2875.79 | 50% |

Let's explore several standout options from the results in the screener.

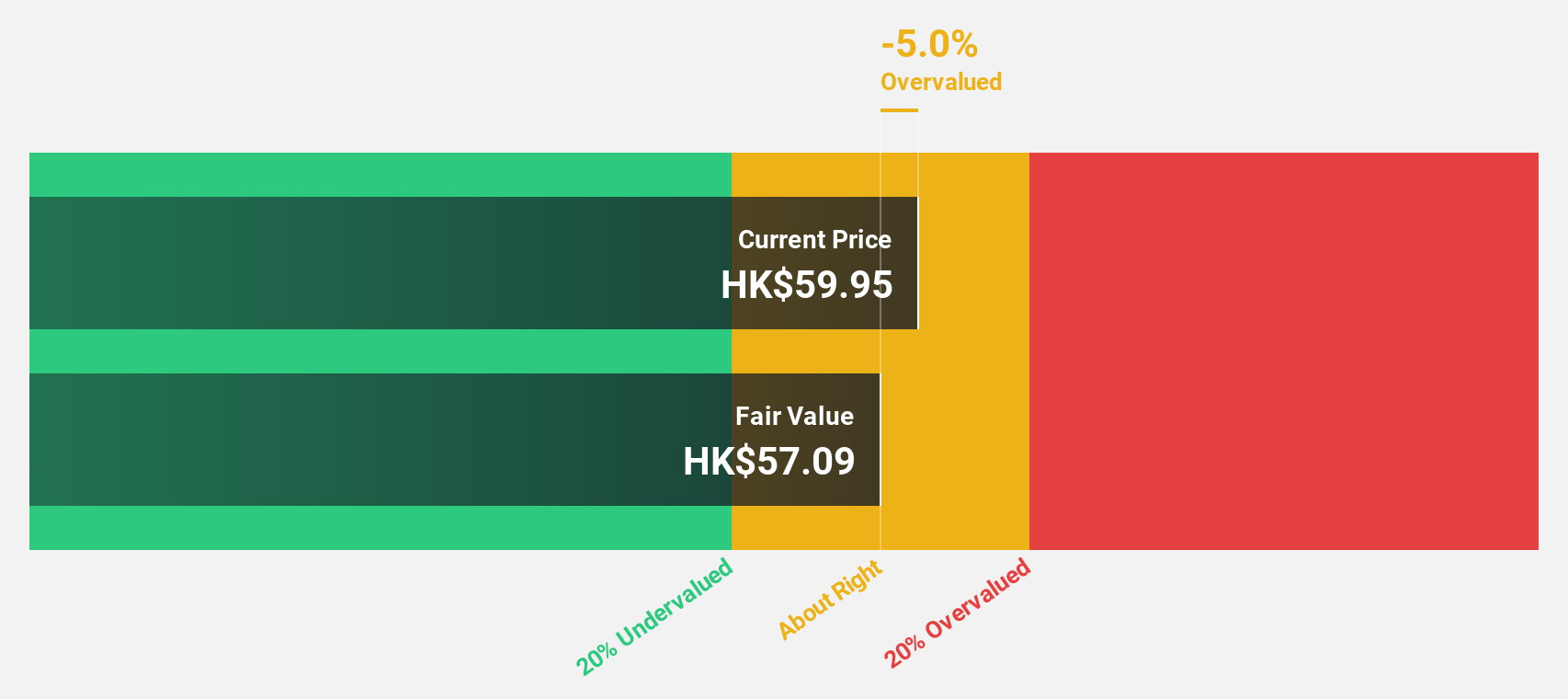

Xiaomi (SEHK:1810)

Overview: Xiaomi Corporation is an investment holding company that develops and sells smartphones in Mainland China and internationally, with a market cap of approximately HK$663.95 billion.

Operations: The company's revenue is primarily derived from smartphones (CN¥180.10 billion), IoT and lifestyle products (CN¥115.54 billion), smart EV, AI, and other new initiatives (CN¥107.35 billion), and internet services (CN¥37.83 billion).

Estimated Discount To Fair Value: 14.7%

Xiaomi appears undervalued based on cash flows, trading at HK$25.84, below its estimated fair value of HK$30.29. Despite recent declines in sales and net income, earnings are projected to grow 20.2% annually, surpassing the Hong Kong market's growth rate of 12.6%. However, return on equity is forecasted to be modest at 14.3%. Recent changes in company bylaws and leadership may influence strategic direction positively for future growth initiatives.

- Upon reviewing our latest growth report, Xiaomi's projected financial performance appears quite optimistic.

- Unlock comprehensive insights into our analysis of Xiaomi stock in this financial health report.

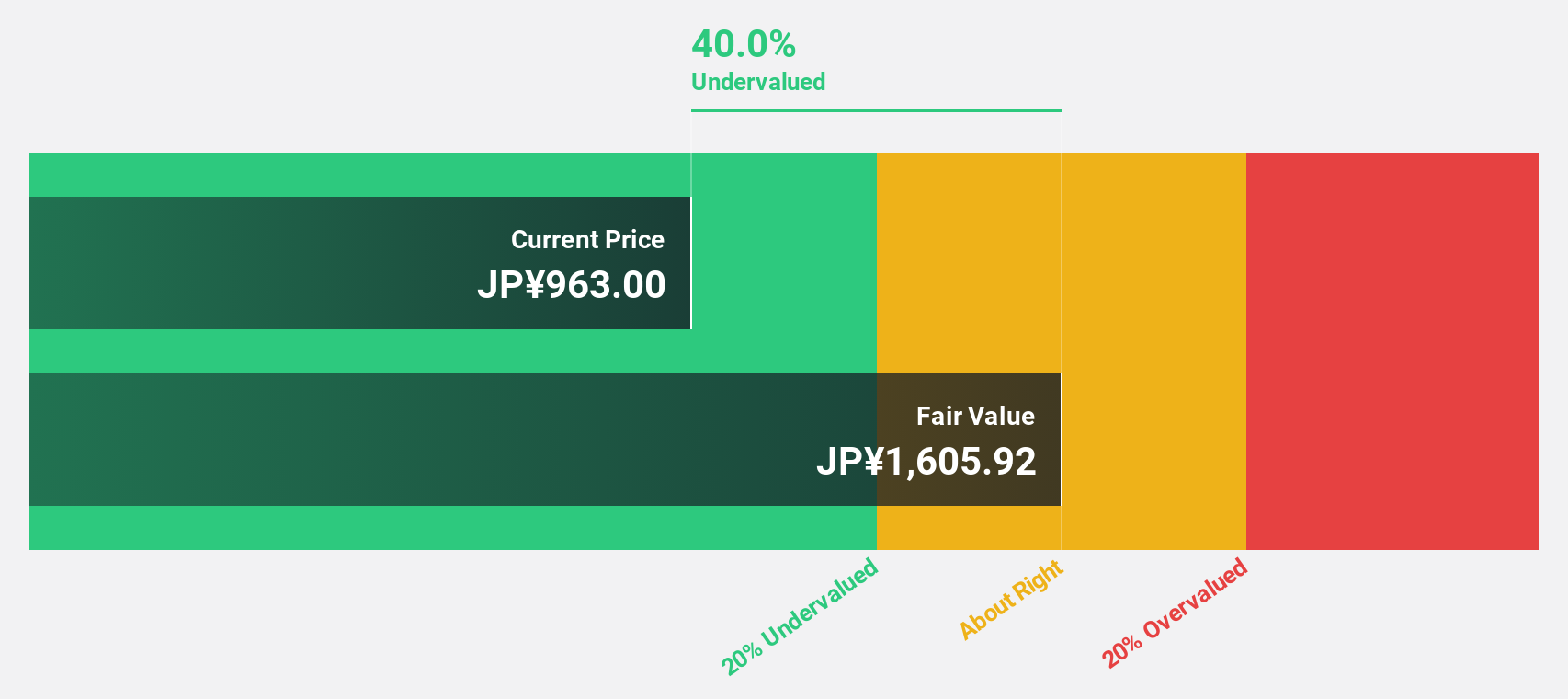

Insource (TSE:6200)

Overview: Insource Co., Ltd. operates in Japan, offering lecturer dispatch type training, open lectures, and other educational services, with a market cap of ¥52.07 billion.

Operations: The company generates revenue of ¥15.07 billion from its Education Service Business segment.

Estimated Discount To Fair Value: 34%

Insource is trading 34% below its estimated fair value of ¥938.72, indicating it may be undervalued based on cash flows. The company offers a reliable dividend yield of 4.76%. Despite a recent downward revision in earnings guidance, Insource's earnings grew by 17.4% over the past year and are forecasted to grow at 12.2% annually, outpacing the broader Japanese market's growth rate of 10.2%. Recent organizational changes aim to enhance sales efficiency and leverage AI advancements for cost management.

- The growth report we've compiled suggests that Insource's future prospects could be on the up.

- Get an in-depth perspective on Insource's balance sheet by reading our health report here.

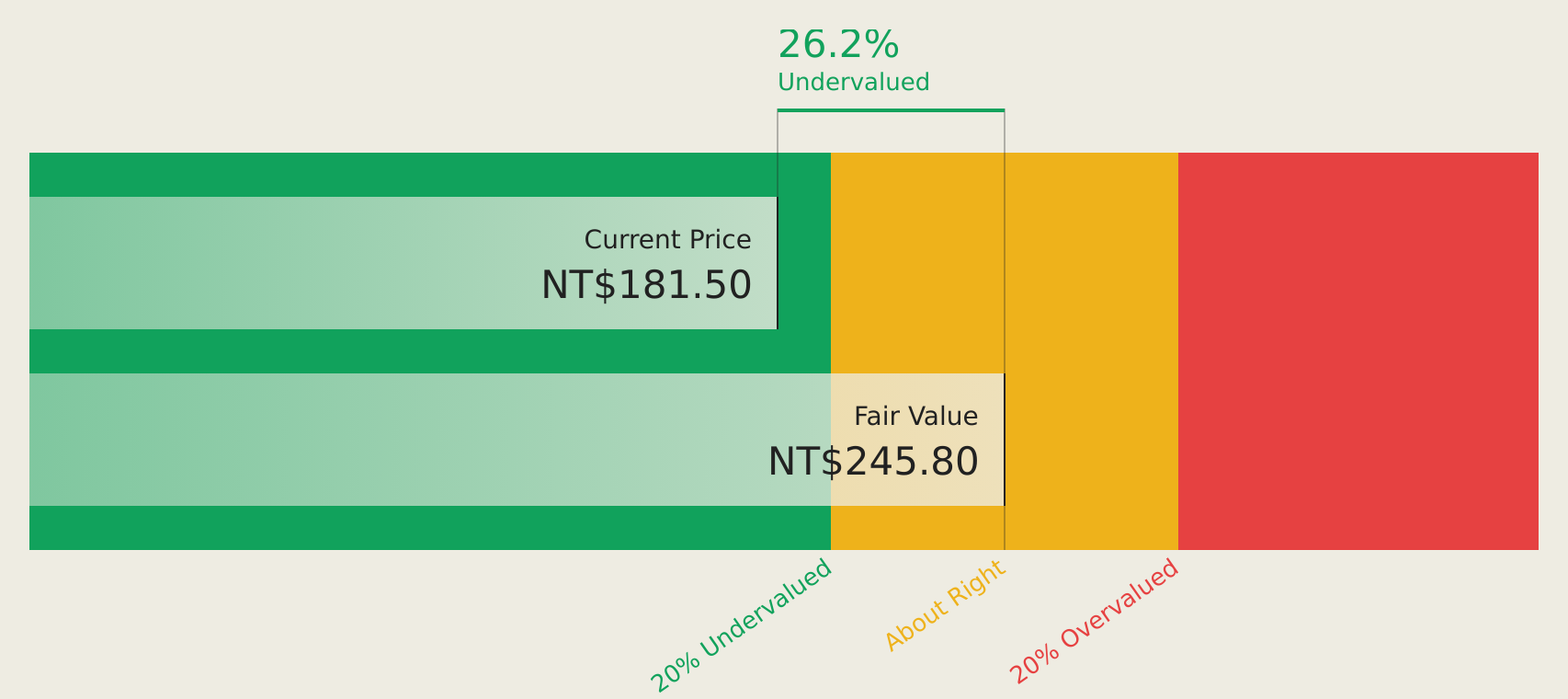

Eurocharm Holdings (TWSE:5288)

Overview: Eurocharm Holdings Co., Ltd. is engaged in the manufacturing and sale of motorcycle and auto equipment parts, medical equipment, and machine parts across Taiwan, Vietnam, the United States, and internationally with a market cap of NT$12.93 billion.

Operations: The company generates revenue of NT$6.97 billion from its operations in manufacturing and selling automobile, motorcycle parts, and medical equipment.

Estimated Discount To Fair Value: 24.4%

Eurocharm Holdings is trading at NT$185.5, significantly below its estimated cash flow value of NT$245.41, highlighting potential undervaluation based on cash flows. Despite a modest decline in net income to TWD 249.06 million for Q1 2026, revenue rose to TWD 2,061.14 million from the previous year. Earnings are expected to grow substantially at over 30% annually, surpassing Taiwan's market averages; however, dividends remain poorly covered by free cash flows.

- The analysis detailed in our Eurocharm Holdings growth report hints at robust future financial performance.

- Delve into the full analysis health report here for a deeper understanding of Eurocharm Holdings.

Key Takeaways

- Navigate through the entire inventory of 186 Undervalued Asian Stocks Based On Cash Flows here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com