- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

SMS (TSE:2175) Could Be 32% Below Fair Value After Its Sharp Move

SMS stock moves without a clear news catalyst

SMS (TSE:2175) has attracted attention recently as the stock moved sharply without a specific headline event, prompting investors to look more closely at its valuation, recent returns and underlying business trends.

See our latest analysis for SMS.

Recent momentum in SMS has been strong, with a 1 month share price return of 21.61%, a 90 day share price return of 41.03% and a year to date share price return of 81.78%. The 1 year total shareholder return of 73.28% contrasts with weaker 3 and 5 year total shareholder returns. This suggests that current enthusiasm is more recent and tied to changing expectations around its business performance and valuation.

If SMS’s sharp move has caught your eye and you want to see what else is gaining traction, it could be a good time to check out 12 top founder-led companies

Bulls point to SMS’s recent share price surge and strong annual revenue and net income growth, while bears focus on the current loss and gap to analyst targets. This raises the question of which side the valuation supports next.

Preferred Price-to-Sales multiple of 3.1x: Is it justified?

With SMS last closing at ¥2,454, the stock is currently tagged with a P/S multiple of 3.1x that sits above both peer and industry averages.

The P/S ratio compares the company’s market value to its revenue, so a higher figure usually reflects stronger expectations around future sales quality or growth. For SMS, that 3.1x sits above the peer average of 2.4x and far above the wider JP Professional Services industry average of 0.9x, which implies the market is putting a richer tag on its revenue stream than on many competitors.

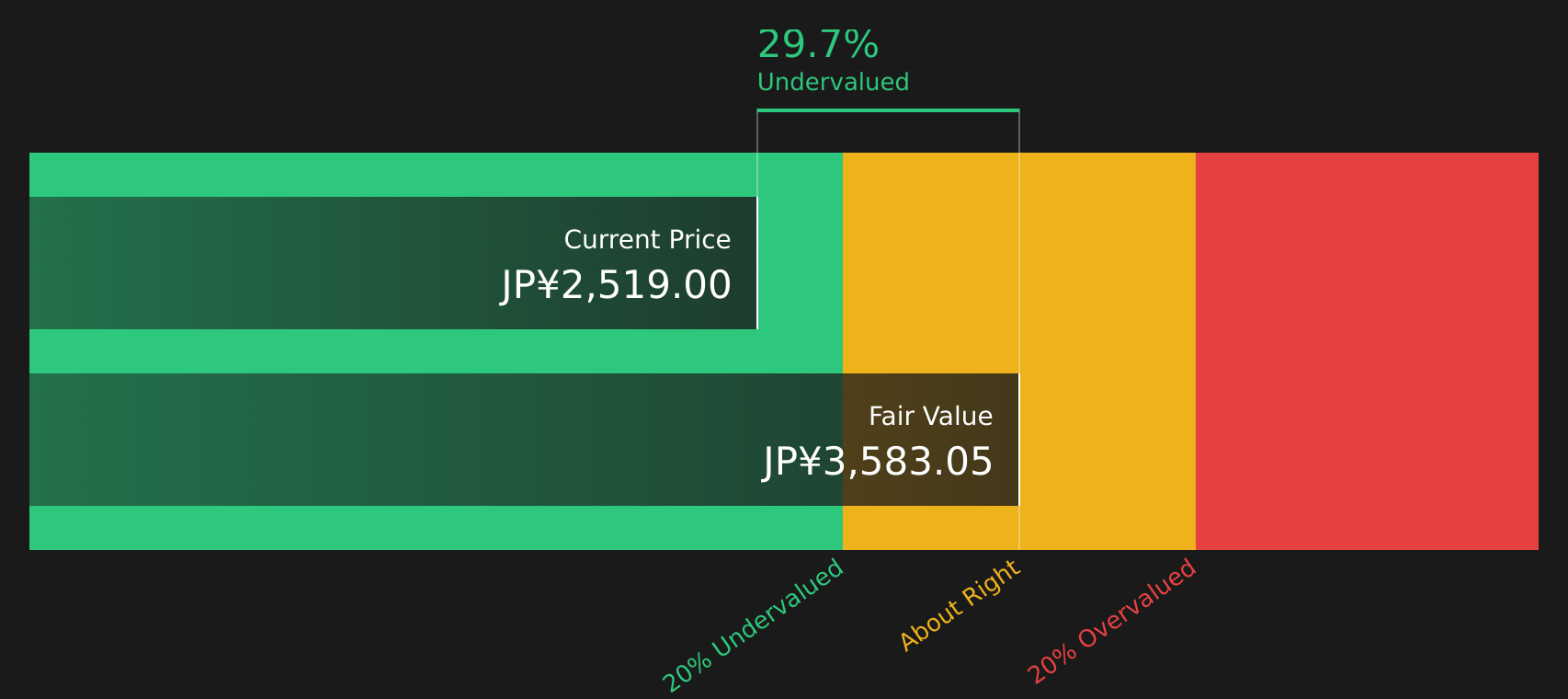

Even so, Simply Wall St’s fair P/S estimate of 4.2x suggests the current 3.1x multiple is below the level the market could eventually gravitate toward if those expectations play out. In that context, SMS also appears to be trading at a 31.5% discount to the SWS DCF fair value estimate of ¥3,584.57, which indicates the current share price does not fully line up with that cash flow based view.

Explore the SWS fair ratio for SMS

Result: Price-to-Sales of 3.1x (UNDERVALUED)

However, SMS still carries risks, including a recent net income loss of ¥14,317 and a share price that currently sits above analyst targets.

Find out about the key risks to this SMS narrative.

Another view on SMS using the SWS DCF model

While the current 3.1x P/S suggests SMS trades richer than peers, the SWS DCF model points the other way. The model shows a fair value estimate of ¥3,584.57 against the ¥2,454 share price. That gap paints SMS as undervalued on cash flows, so which signal do you treat as more important?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out SMS for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 19 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment around SMS clearly mixed, it makes sense to move quickly, review the underlying data yourself and decide what really matters for your portfolio. To see why some investors are optimistic about its potential rewards, take a closer look at the 2 key rewards

Looking for more investment ideas beyond SMS?

If SMS has sharpened your focus on opportunities, do not stop here. Broader research can help you spot stocks that better fit your goals and risk comfort.

- Target potential value opportunities by scanning 19 high quality undervalued stocks that combine quality fundamentals with pricing that may not fully reflect their financial profile.

- Strengthen your income focus by reviewing 45 dividend fortresses that prioritise robust payouts supported by underlying cash flows.

- Prioritise resilience by checking 54 resilient stocks with low risk scores that score well on balance sheet strength and volatility measures.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com