- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

CITIC Construction Investment: Short-term supply expectations suppress lithium prices, and downstream demand supports the off-season in the third quarter

The Zhitong Finance App learned that CITIC Construction Investment Securities released a research report saying that lithium prices fell sharply last week, and expectations of marginal supply easing were suppressed. Mainly, the resumption of lithium production in Jiangxi and lithium concentrate in Hong Kong will all be fulfilled in July, but the concentrate remains tight. Some lithium salt plants have declined due to factors such as tight raw materials and maintenance, pyroxene and mica production declined, and production continued to decline during the week; at the same time, inventory remained depreciated, and some scattered orders were reluctant to increase prices. There are not too many concerns on the demand side. On the early consumer side, more new production capacity will be initially built and production will increase in the second half of the year, amplifying the downstream inventory replenishment effect, leading to a marginal increase in consumption. On the terminal demand side, the decline in NEV subsidies in 2027 will consolidate rush during the year and push up production expectations for the second half of the year. The growth rate of commercial vehicles is optimistic. The growth rate of commercial vehicles is optimistic. In the first half of the year, 1.833 million pure electric vehicles were exported, up 114.4% year on year. Looking at the third quarter, production schedules for July and August are expected to maintain positive month-on-month growth. The off-season is not weak, and the peak season can be expected.

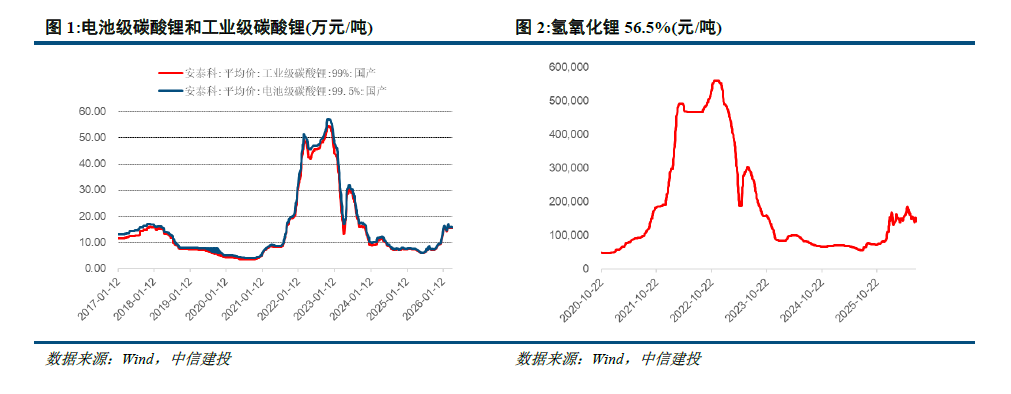

Lithium: According to Baichuan Yingfu, the average market price of industrial grade lithium carbonate was 155,000 yuan/ton last week, down 3.1% from last week; the average price of battery-grade lithium carbonate was 158,000 yuan/ton, down 3.1% from last week.

On the supply side, lithium carbonate production is expected to drop slightly last week. Mainly due to factors such as tight raw materials and maintenance in some lithium salt plants. Zimbabwe lithium concentrate has been shipped and is expected to arrive in Hong Kong in mid-late July. Signals to resume production at the Jiangxi mining terminal and related salt mills have increased, disrupting supply expectations. According to customs data, Chile exported 1,5095 tons of lithium salt to China in June, with an average export price of 18,814 US dollars/ton, which has rebounded somewhat from month to month.

In terms of inventory, last week's inventory is expected to continue the trend of elimination. Shipments from the lithium salt factory manager are stable, and some loose orders are reluctant to sell, causing inventory to accumulate slightly. Traders' turnover increased last week. Downstream purchases at dips increased, and inventory was mostly transferred from the trade chain to downstream. The number of futures warehouse orders is still relatively high. The volume of warehouse orders on the previous trading day was 4,3640 tons.

On the demand side, downstream demand remained high last week, and the overall production schedule for July is expected to increase slightly. Lithium iron phosphate production schedule increased significantly in July, and is expected to increase by about 7% month-on-month. According to a sample survey of 26 battery companies in Baichuan Yingfu, in July 2026, the total production schedule of Chinese battery companies was 296.6 GWh, an increase of 7.83% over the previous month. After prices fell back, downstream material manufacturers increased their willingness to inquire and purchase at low prices, but their willingness to stock up on a large scale was insufficient, and actual transactions were still mainly based on stocks that just needed to be replenished. On the resource side, the significance of autonomous and controllable domestic lithium resources is highlighted.

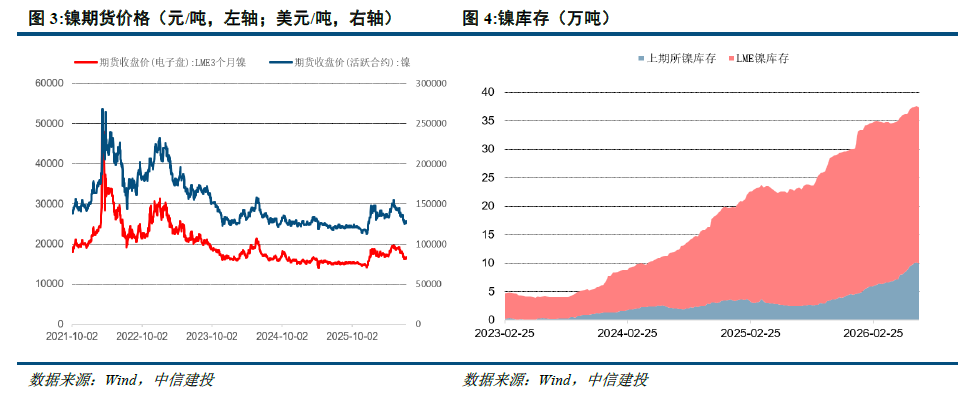

Nickel: Last week's LME nickel price was 16,655 US dollars/ton, up 1.8% from last week; nickel price in the previous period was 128,180 yuan/ton, up 0.5% from last week. SHFE nickel stocks last week were 991,000 tons, and LME nickel stocks were 274,600 tons, with a total inventory of 373,700 tons, down 0.7% from last week.

On the supply side, the overall domestic supply of nickel sulfate decreased last week, and the average operating rate of the industry decreased. Affected by downstream price pressure and cost and profit pressure, some nickel salt manufacturers took the initiative to reduce production loads. A small number of idle production lines were phased out and overhauled. The recovery in construction would have to wait for the downstream preparation to begin in the third quarter of mid-late August.

On the demand side, demand for nickel sulfate was still in a low season last week. Downstream companies mainly consumed their own inventory. They only needed to make long-term purchases. There was no large-scale centralized inventory replenishment in the market, and the phenomenon of overselling goods was common; stable demand in the electroplating sector made it difficult to hedge against weak battery side, and demand for nickel sulfate remained weak in the short term.

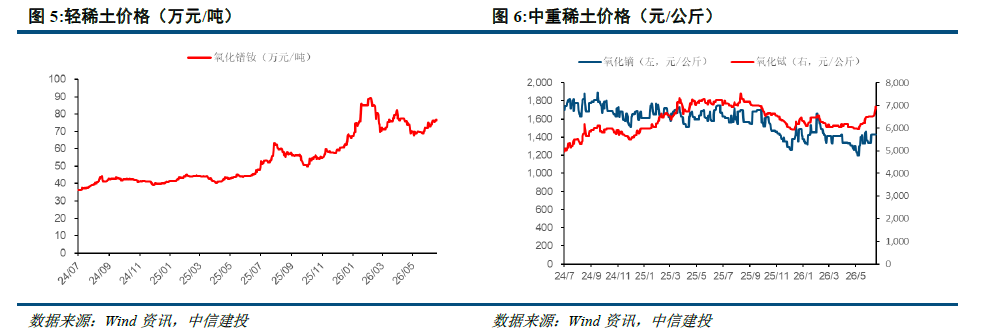

Rare earths & magnetic materials: Prices of rare earths increased last week. As of last Thursday, the average price of praseodymium oxide in the market was 767,500 yuan/ton, up 0.79% from last Thursday; the average price of dysprosium oxide in the market was 1,425,000 yuan/ton, up 0.35% from last Thursday; the average price of terbium oxide in the market was 6.775 million yuan/ton, up 3.83% from last Thursday.

Judging from the fundamentals of supply and demand, it is difficult for the supply side to increase. In the third quarter, separation companies had no production situation affected by the indicators. Construction was stable, EIA production capacity was limited, and production increases were limited. Some separation companies using chlorinated tablets as raw materials suspended production for a short time, waste recycling production companies continued to start low, and the problem of tax-containing raw materials was difficult to resolve in the short term. Overall market supply continued to be tight, and there were no incremental expectations yet. The demand side gradually improved. The downstream off-season performance in the second quarter increased. The market's demand expectations for the third quarter increased. Most major magnetic material manufacturers maintained stable production, and there were positive expectations for new export orders. The main reason was that terminal delivery prices and upstream raw material prices were deadlocked, and overall market demand was positive.