- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Royal Caribbean Stock Faces Fresh Pressure From Gulf Shipping Risk

When geopolitics hits shipping lanes and energy flows, it is often the stocks most exposed to the news that move first, not always in the direction investors might expect. The closure of the Strait of Hormuz and rising military tension across key Gulf trade routes have pushed Gulf Geopolitical Risk Stocks With Energy and Trade Exposure into sharper focus, as traders reassess operational risk, funding pressure, and supply disruption. This article walks through 3 stocks that screens flag as particularly vulnerable to this shock, helping you evaluate which risks might be worth avoiding or watching more closely right now.

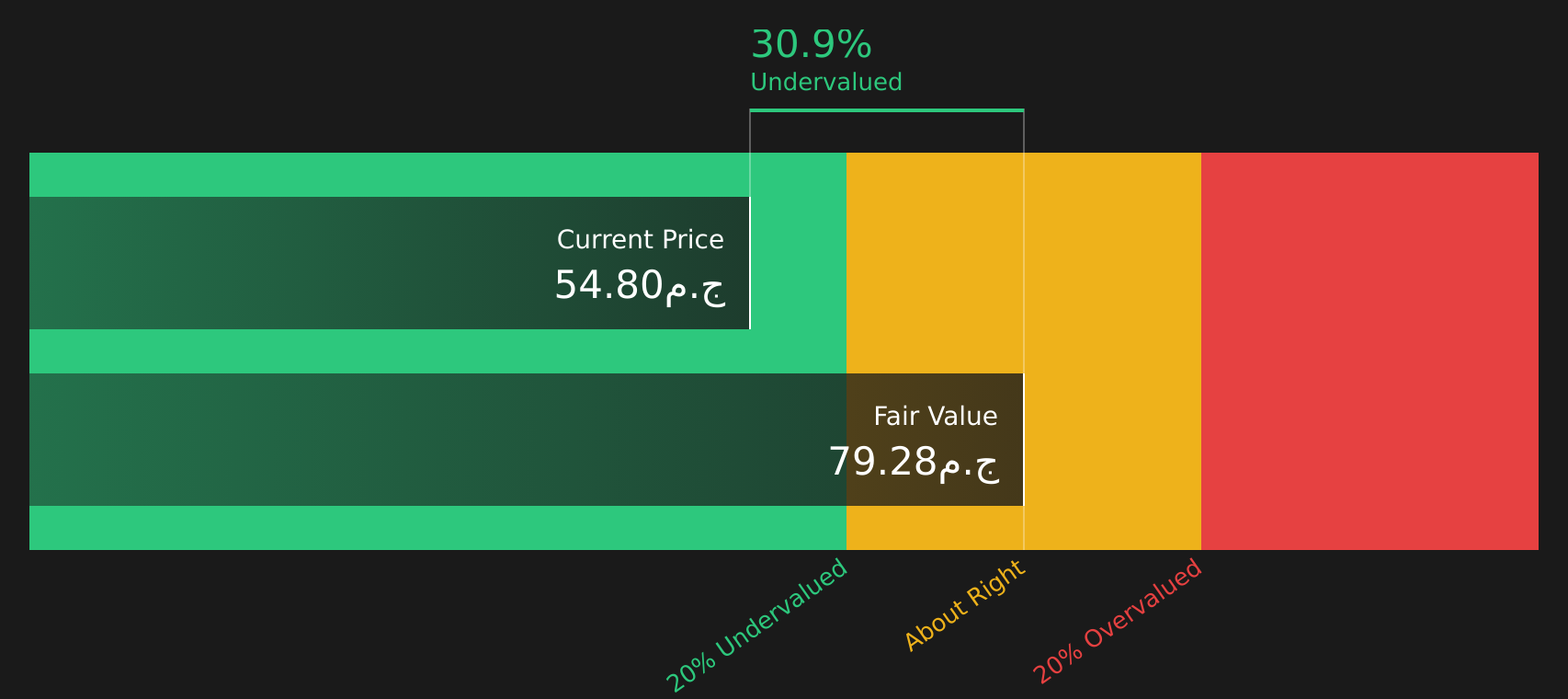

Qatar National Bank (CASE:QNBE)

Overview: Qatar National Bank is a Cairo based subsidiary of Qatar National Bank that offers a wide range of retail and corporate banking services in Egypt, from everyday current and savings accounts to cards, consumer and mortgage loans, auto finance, and project and structured finance for larger clients.

Operations: Qatar National Bank generates about EGP 56.7b in revenue in Egypt, led by Other Businesses at roughly EGP 22.1b, Individuals at EGP 16.3b, Corporate Banking at EGP 15.4b, and Investments at EGP 4.8b.

Market Cap: EGP 116.5b

Qatar National Bank screens as interesting for Gulf geopolitical risk because it combines current fundamentals with real exposure to regional shocks. Earnings and return on equity are high, and the stock trades on a low P/E with the current price sitting below one independent fair value estimate. A bad loan ratio of 3.9% points to possible credit quality pressure if Gulf tensions curb trade or raise funding costs, and limited board independence may make it harder to challenge risk taking linked to the wider group and region. For investors, the central issue is how much of this geopolitical and governance risk is priced in and how quickly that could change if conditions deteriorate further.

Qatar National Bank’s low P/E and current fundamentals may be masking how quickly credit quality could shift if Gulf stress escalates. It is therefore worth reviewing the 5 key rewards and 1 important warning sign

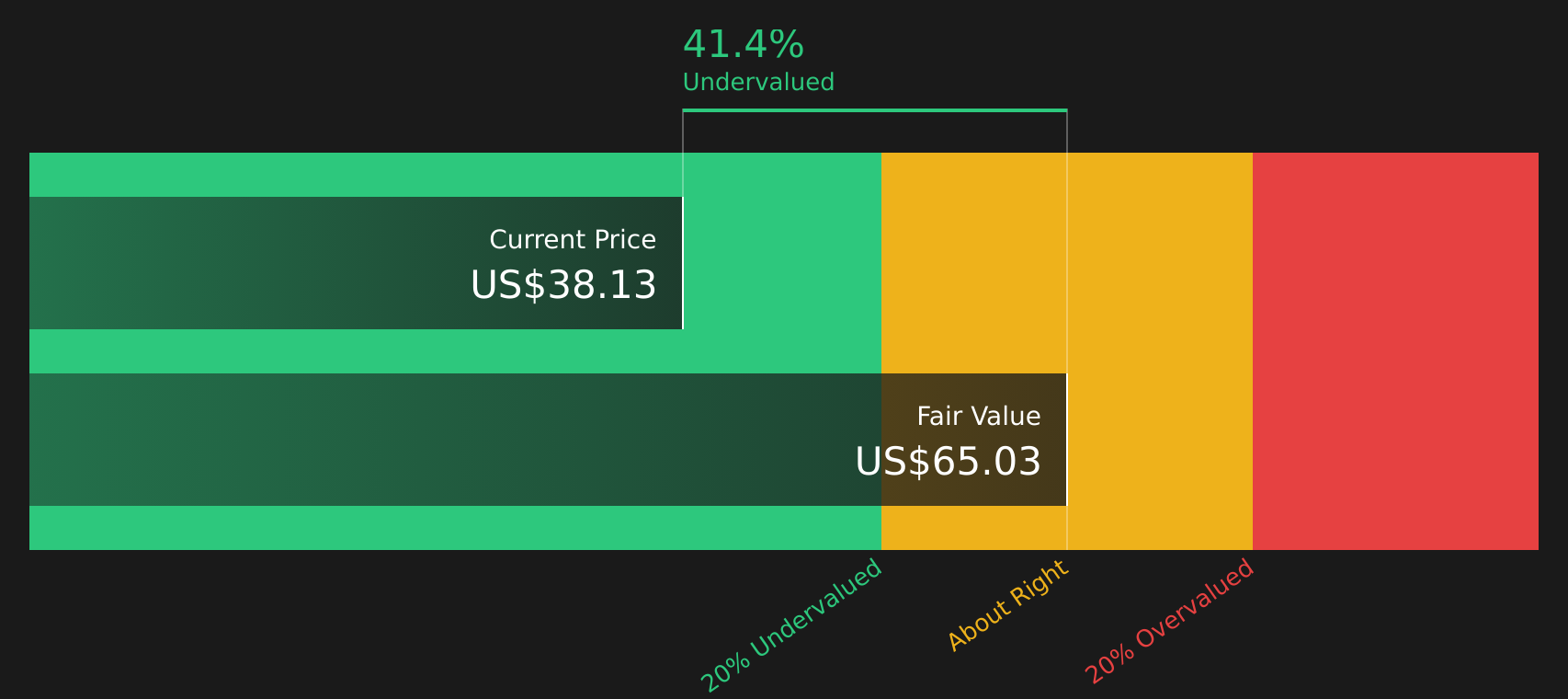

Royal Caribbean Cruises (RCL)

Overview: Royal Caribbean Cruises operates a global fleet of cruise ships under the Royal Caribbean International, Celebrity Cruises, and Silversea Cruises brands, offering a wide range of itineraries from mass market vacations to higher end, premium experiences. Founded in 1968 and headquartered in Miami, the company runs one of the largest cruise operations worldwide with dozens of ships deployed across multiple regions.

Operations: Royal Caribbean Cruises generates about US$18.4b in revenue from its cruise operations, with North America accounting for roughly US$11.9b of sales and Europe and Asia/Pacific contributing several billion dollars combined.

Market Cap: US$76.5b

Royal Caribbean Cruises may look attractive with strong recent earnings, high net margins around 24.4% and a share price that screens as well below one discounted cash flow value estimate, but the risk side of the ledger is getting heavier. The closure of the Strait of Hormuz and wider Middle East tensions feed directly into fuel price volatility, an issue management has already highlighted as a cost headwind, while a heavily debt funded balance sheet and dividends not fully covered by free cash flow leave less room for error if demand for cruises weakens or itineraries are disrupted. Investors who only focus on new ships and premium pricing may be missing how exposed Royal Caribbean Cruises is to higher funding and operating costs if geopolitical stress and consumer softness worsen.

Royal Caribbean Cruises’ premium pricing and strong margins may be masking how exposed the story is to fuel shocks and heavy debt, so it is worth reading the 4 key rewards and 2 important warning signs

Frontline (FRO)

Overview: Frontline operates a global fleet of crude and product tankers, transporting oil on major seaborne routes using very large crude carriers (VLCCs), Suezmax tankers, and LR2/Aframax vessels, and also trades ships through chartering, purchases, and sales.

Operations: Frontline generates about US$2.3b in revenue from its tanker operations.

Market Cap: US$8.5b

Frontline provides direct exposure to the oil shipping trade at a time when the Strait of Hormuz closure and wider Gulf attacks are making some of its most important routes more expensive and less predictable. Recent results show strong earnings, high margins, and an apparently cheap valuation versus fair value estimates. At the same time, analysts still expect meaningful declines in revenue and earnings over the next few years and highlight a balance sheet funded entirely by higher risk external borrowing. When insurance, rerouting, and geopolitical disruption intersect with high leverage and an unstable dividend record, the question is whether today’s strong cash generation adequately compensates investors for the risk that the tanker cycle and Gulf conflict could turn against Frontline faster than the market is currently pricing in.

Frontline’s strong cash generation and tanker exposure might be masking how quickly high leverage and Gulf route disruption could bite. It is worth reading the 3 key rewards and 3 important warning signs (1 is major!)

Take Control of Your Investment Journey

If Royal Caribbean Cruises or any of these companies are making you feel more cautious, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Momentum Flies

Markets move fast, and the next breakout list can shift before the crowd catches on. Spot fresh ideas while they matter, under the radar for now, and consider them early.

- Look at cash rich compounders that could benefit from momentum using the curated 212 high quality undervalued stocks before others notice the gap between quality, balance sheets, and current pricing.

- Consider the structural build out of next generation energy using the focused 89 nuclear energy infrastructure stocks while infrastructure stocks may still be largely flying below wider market attention.

- Follow companies involved in tomorrow’s smart grids through the curated 34 power grid technology and infrastructure stocks before capital flows fully reprice the earnings potential tied to electrification and resilience upgrades.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com