- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Britannia Stock And Indian Staples Facing Higher Inflation Pressure

India’s inflation story is shifting again, with retail prices projected to breach the 4% mark in June 2026 as food and fuel costs squeeze household budgets. That kind of pressure can quietly reshape the risk and reward profile of consumer staples and food retail stocks, especially those exposed to rising input bills and cautious shoppers. This article looks at 3 stocks from the Consumer Staples and Food Retail Stocks With Inflation Exposure screener that appear more vulnerable to this trend, unpacking how sustained price pressures, policy rates on hold and sticky global food costs might weigh on their earnings quality and investor appeal.

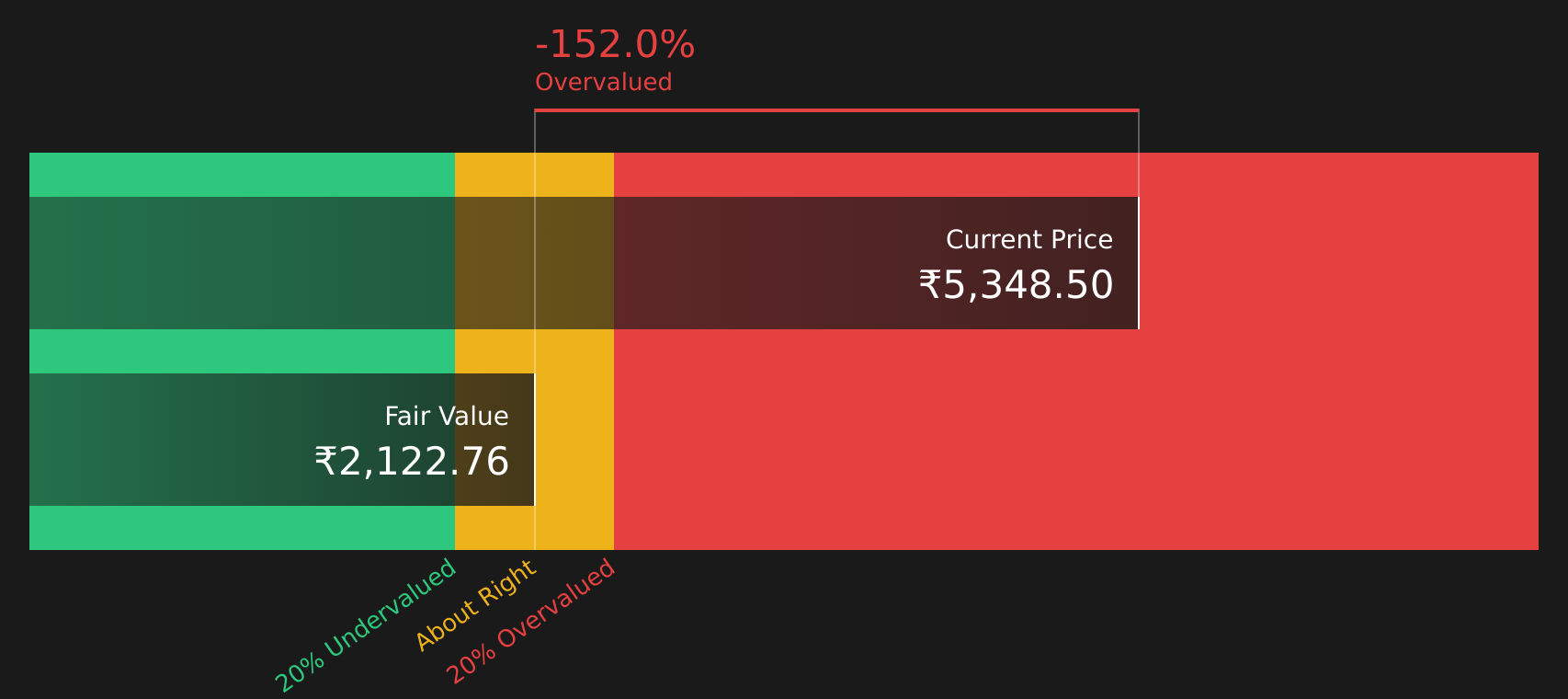

Britannia Industries (NSEI:BRITANNIA)

Overview: Britannia Industries is an Indian packaged food company that sells biscuits, cakes, rusks, croissants, wafers, snacks, dairy products and breads under a wide portfolio of brands, and exports to around 80 countries.

Operations: Britannia generates virtually all of its ₹191,515.9 million revenue from its Foods segment.

Market Cap: ₹1.29t

Investors looking at Britannia Industries in a higher inflation setting may find a mix of strong fundamentals and uncomfortable questions. The company has high profitability, with a 13.2% net margin and very strong 49.4% ROE, and is leaning into branded foods, premium launches and quick commerce. However, that quality comes with a rich P/E of 50.9x and a share price that sits well above one valuation estimate of fair value. At the same time, the business is tightly exposed to wheat, palm oil, milk and fuel, and management itself points to rising laminate, fuel and milk costs, while free cash flow coverage of the dividend is weak. With CPI expected to push above 4% and food inflation sticky, the biscuit leader is not a straightforward comfort stock in this inflation screener.

Britannia’s rich P/E and tight cost exposure could be masking where the real pressure shows up next. Before assuming it is a safe inflation anchor, scan the 2 key rewards and 1 important warning sign

Avenue Supermarts (NSEI:DMART)

Overview: Avenue Supermarts operates the D Mart supermarket chain across India, selling a wide range of groceries, packaged food, household essentials, general merchandise and apparel, supported by its online format DMart Ready for grocery and home delivery.

Operations: Avenue Supermarts generates all of its ₹688.2b revenue from retail operations in India.

Market Cap: ₹2.66t

Investors watching Avenue Supermarts in a rising inflation setting may weigh its growth credentials against growing pressure on shoppers and valuation. The company reports revenue of ₹688.9b and net income of ₹29.7b in FY2026, and recent quarters show gains in sales and profit. Net margins are 4.3%, slightly below last year, and a projected CPI break above 4% driven by food and fuel may increase the risk that discretionary baskets from general merchandise and apparel come under strain. With a P/E multiple that sits far above sector averages and funding that relies entirely on external borrowing rather than customer deposits, Avenue Supermarts may be more exposed if higher prices start to curb store traffic and spending.

Avenue Supermarts’ rich P/E and thin 4.3% margin, in a CPI setting projected above 4%, could be masking pressure points in its core model. Scan the analysis report for Avenue Supermarts for what might crack first.

Hindustan Unilever (BSE:500696)

Overview: Hindustan Unilever is a large fast moving consumer goods company that sells everyday products in India and abroad, from detergents, soaps and shampoos to tea, coffee, nutrition drinks and skincare, as well as operating beauty salons and related services.

Operations: Hindustan Unilever generates most of its revenue from Home Care (₹236.7b), Beauty & Wellbeing (₹149.9b), Foods (₹140.6b) and Personal Care Business (₹95.6b), with a smaller contribution from other activities and exports, and ₹619.5b of sales coming from India versus ₹25.2b from outside India.

Market Cap: ₹5,053.0b

Hindustan Unilever is often viewed as a classic consumer staple anchor, yet the mix of high valuation, modest earnings growth and rising inflation risk may warrant closer scrutiny. The stock trades on a relatively rich earnings multiple, while recent earnings momentum has softened and net margins at 16.5% are slightly lower than a year earlier. This comes at a time when food and palm oil costs remain elevated and rural demand faces pressure from higher CPI. Management highlights pricing power across essentials such as soaps, detergents and tea, but dividend coverage is not strong and analysts only anticipate moderate growth relative to the wider Indian market. For anyone considering Hindustan Unilever as a potential safe haven as inflation moves above 4%, the relationship between business quality and valuation is an important factor to assess.

Hindustan Unilever’s rich earnings multiple and softer momentum could be masking how much room is left before valuation and earnings quality start to clash as inflation bites. Read the analyst forecasts for Hindustan Unilever to see what might be missing

Take Control of Your Investment Journey

If Hindustan Unilever or any of these companies are making you feel more cautious, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh ideas move first, and by the time the crowd catches on, the best entry points are often gone. Scan these curated stock sets while it matters most and consider your options.

- Spot early movers in niche themes by reviewing 499 high quality undiscovered gems that are still under the radar for now but showing quiet momentum.

- Target resilient cash generators by assessing 472 dividend fortresses, which combine income potential with balance sheets designed to handle tougher conditions without panic selling.

- Follow structural shifts in critical materials by tracking 30 best rare earth metal stocks that are involved in long term technology and energy infrastructure build outs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com