- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

3 High Yield Dividend Stocks For More Resilient Income

With inflation trends mixed, bond markets reacting to every oil price headline, and central banks keeping policy decisions tightly tied to data, many investors are looking for income sources that feel more resilient than short term market sentiment. That is where high yield dividend fortresses come in. This screener focuses on stocks offering 5%+ dividend yields, with an emphasis on stability rather than speculation. In this article, you will see three of the strongest candidates from the Dividend Fortresses list and how they might help anchor a portfolio that wants income without chasing the latest market story.

Halyk Bank of Kazakhstan (LSE:HSBK)

Overview: Halyk Bank of Kazakhstan is a universal bank headquartered in Almaty that provides corporate, SME, retail and investment banking services across Kazakhstan, Kyrgyzstan, Georgia and Uzbekistan, offering everything from everyday accounts and cards to mortgages, business loans, trade finance and investment products.

Operations: The bank generates most of its revenue from Corporate Banking at KZT 751.4b and Investment Banking at KZT 329.7b, with additional contributions from SME Banking at KZT 194.1b, Retail Banking at KZT 154.1b and KZT 378.0b from unallocated activities, primarily in Kazakhstan which accounts for KZT 3,386.1b of revenue.

Market Cap: KZT 8.4b

Halyk Bank of Kazakhstan stands out in this high yield dividend fortress shortlist because it combines very strong profitability metrics with a low P/E and a large, established franchise in its home market. High returns on equity, wide net interest margins and a sizeable dividend suggest the bank is currently converting its market position into meaningful cash returns for shareholders, even as earnings growth has cooled and bad loans sit at a relatively high 8.3% with modest coverage. At the same time, rising regulation, heavy exposure to Kazakhstan and growing fintech competition mean this is not a simple income stock to buy and hold without ongoing monitoring. The key issue for investors is how the balance of income, valuation and risk aligns with their individual objectives and risk tolerance at today’s price.

High returns on equity, a low P/E and a sizeable dividend suggest Halyk Bank of Kazakhstan might be priced as if its risks outweigh its strengths, but the 4 key rewards and 3 important warning signs could reveal a twist investors are missing

Admiral Group (LSE:ADM)

Overview: Admiral Group is a Cardiff based financial services company that focuses on car, home and other personal insurance, alongside personal lending products, serving customers across the UK, France, Italy and Spain through brands like Admiral, ConTe.it, L’olivier and Qualitas Auto.

Operations: Admiral Group generates most of its revenue from UK Insurance at £4.46b, with additional contributions from European Insurance of £656.7m, Other activities of £87.5m, Admiral Money at £25.8m and £17.7m from unallocated investment and interest income.

Market Cap: £11.1b

Admiral Group may appeal to dividend focused investors because it combines a 5%+ yield with profitability metrics that include a net margin of about 14.9% and a strong return on equity, supported by investment in data, machine learning and generative AI aimed at improving pricing and claims efficiency. At the same time, analysts are divided, the stock trades on a higher P/E than many insurance peers, and the balance sheet leans on external borrowing rather than customer deposits, which raises funding risk. With recent analyst moves reflecting differing views on the UK motor pricing cycle and margins, the key issue is whether Admiral’s technology capabilities and diversification can keep underwriting discipline strong enough to support its current valuation and income profile.

Admiral Group’s strong net margin and AI driven underwriting raise the question of whether its higher P/E is fully justified, so the 3 key rewards and 2 important warning signs (1 is major!) could be the missing piece that explains what the market is really pricing in

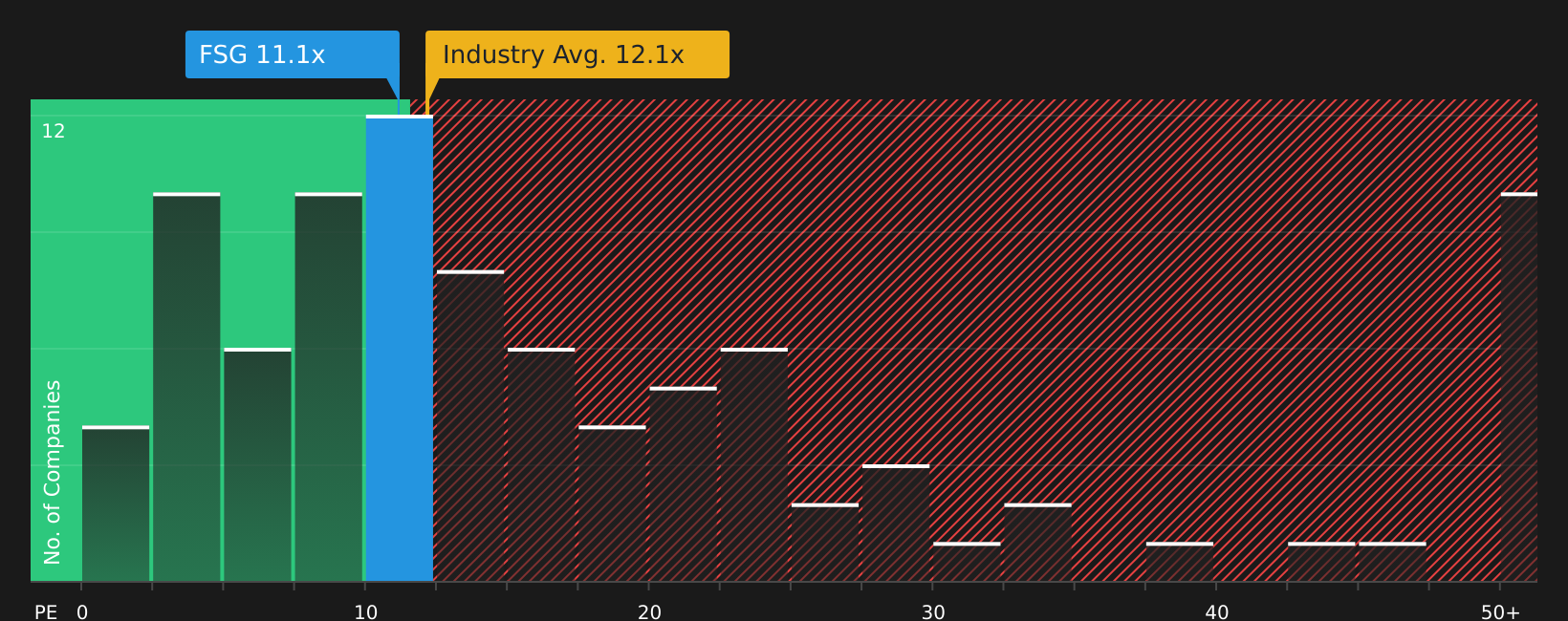

Foresight Group Holdings (LSE:FSG)

Overview: Foresight Group Holdings is a London based asset manager that runs infrastructure, private equity and listed funds for institutional and retail investors, with a focus on renewable energy, social and digital infrastructure, natural capital and smaller growth companies.

Operations: Foresight Group Holdings generates the bulk of its £164.9m revenue from Real Assets at £114.8m, with a further £50.1m from Private Equity, primarily sourced from the United Kingdom at £126.4m and Australia at £25.7m.

Market Cap: £507.0m

Foresight Group Holdings catches the eye in a dividend fortress context because it combines fee based exposure to long term themes such as energy transition and infrastructure with high profitability metrics, including net profit margins in the high 20s and a strong return on equity, while still trading at a lower P/E than many peers. At the same time, earnings are partly tied to performance fees and to policy support for renewables in the UK and Europe, and the group faces rising costs and competition for assets and capital. The real question for investors is whether Foresight’s expanding product range, growing AUM and active share buybacks are enough to offset these pressures and keep translating asset growth into resilient, shareholder friendly cash flows.

Foresight Group’s fee based exposure to energy transition and infrastructure with high margins and a lower P/E hints at something the market may be underpricing; the analysis report for Foresight Group Holdings could reveal what is quietly building beneath the surface.

The three stocks covered here are only a starting point, and the full Dividend Fortresses screener has surfaced 0 more companies with similarly robust income profiles and stories that might fit an income focused watchlist. Use Simply Wall St to identify and analyze the exact catalysts and narratives that matter most, so you can filter for the highest conviction dividend fortress ideas without getting buried in noise.

Take Control of Your Investment Journey

If Halyk Bank of Kazakhstan or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Dividends?

Markets move fast, and the next breakout stock can start flying before most investors even notice. Scan these fresh ideas while it matters and get in early.

- Spot companies quietly building momentum in smaller markets and use the 47 elite penny stocks with strong financials to catch high potential opportunities that others may overlook while they are still under the radar.

- Target businesses powering the next wave of automation. Let the 31 robotics and automation stocks surface curated stocks positioned around robotics themes before the crowd chases the story.

- Zero in on stronger balance sheets as markets keep shifting. Rely on the list of solid balance sheet and fundamentals (20 results) to quickly filter out weaker fundamentals and focus your research time.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com