- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Did New Securities Suits Over Guidance Just Shift Photronics' (PLAB) Investment Narrative?

- In recent months, multiple law firms, including Robbins Geller, The Gross Law Firm, and The Schall Law Firm, have launched securities class actions against Photronics, alleging that earlier statements about revenue outlook, high-end product pipelines, and growth prospects were false or misleading in light of undisclosed operational bottlenecks and subsequent weaker financial results.

- This wave of litigation raises questions about the reliability of prior guidance on Photronics’ growth trajectory and operational execution, which had underpinned earlier investor expectations.

- Against this backdrop of class action allegations focused on revenue outlook and operational bottlenecks, we’ll now examine how this may reshape Photronics’ investment narrative.

The latest GPUs need a type of rare earth metal called Terbium and there are only 30 companies in the world exploring or producing it. Find the list for free.

Photronics Investment Narrative Recap

To own Photronics, you need to believe that its global photomask footprint and ongoing tech upgrades can still convert semiconductor and display design activity into durable cash flows, even as earnings forecasts soften. The recent class actions directly target the credibility of management’s outlook and highlight operational bottlenecks, which may weigh on the near term catalyst of high end node ramp up while amplifying the key risk around volatile IC demand and limited backlog visibility.

The most relevant recent announcement is Photronics’ May Q2 2026 earnings and Q3 guidance, which followed the weaker IC revenue that triggered the lawsuits and a sharp share price reaction. Management’s outlook for Q3 revenue of US$207 million to US$215 million and operating margin of 18% to 20% now sits under a cloud of legal scrutiny, making it a focal point for how quickly the company can address the operational issues alleged in the complaints and rebuild investor confidence.

Yet investors should also weigh how limited order visibility and IC cyclicality could compound these legal and operational uncertainties for Photronics...

Read the full narrative on Photronics (it's free!)

Photronics' narrative projects $930.0 million revenue and $81.2 million earnings by 2029. This requires 2.6% yearly revenue growth and a $77.9 million earnings decrease from $159.1 million.

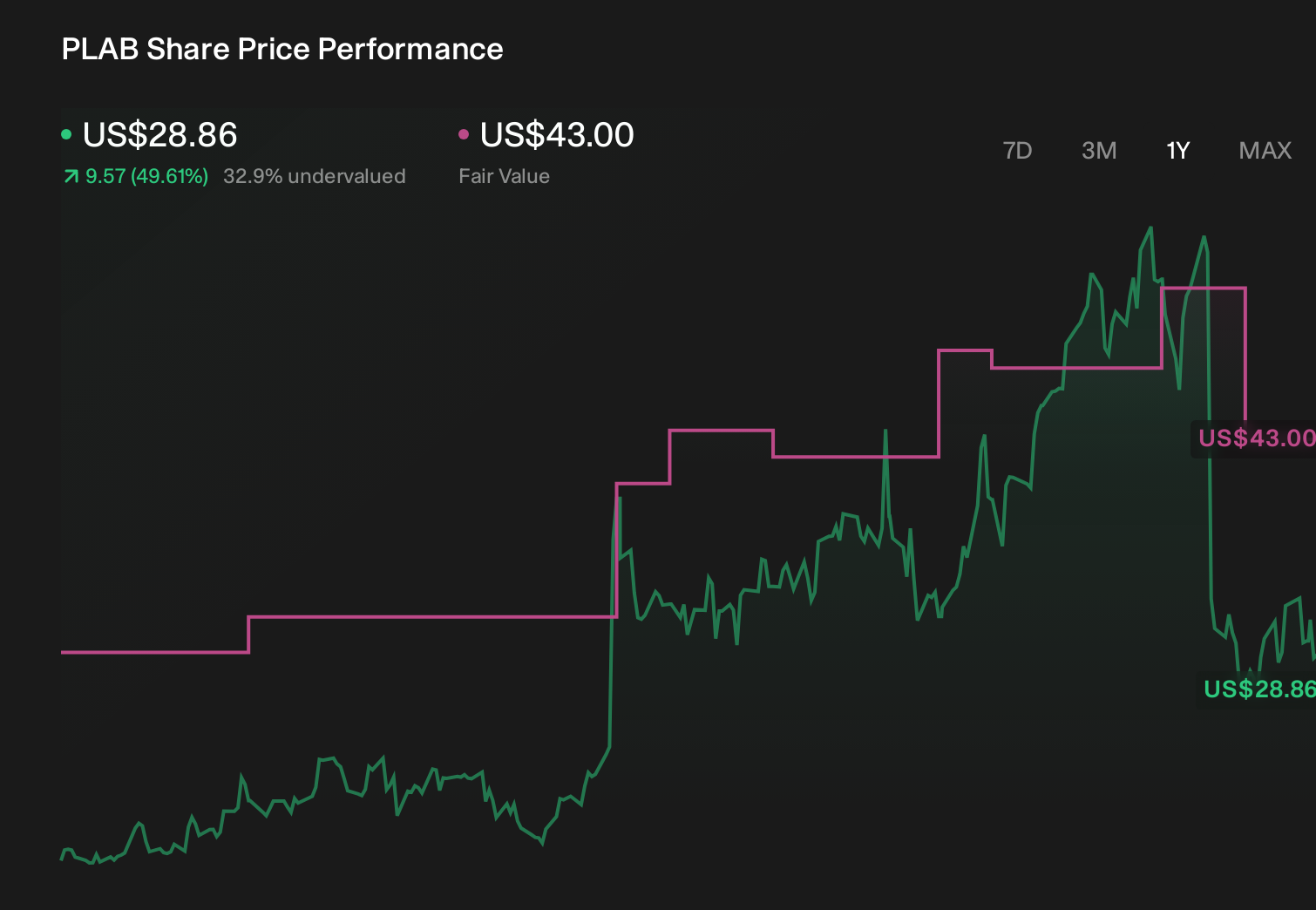

Uncover how Photronics' forecasts yield a $43.00 fair value, a 44% upside to its current price.

Exploring Other Perspectives

Five fair value estimates from the Simply Wall St Community span roughly US$21.85 to US$43, showing how far apart individual views on Photronics can be. When you set this against the current scrutiny of its revenue outlook and operational bottlenecks, it underlines why checking several alternative viewpoints on the company’s execution risk and earnings resilience really matters.

Explore 5 other fair value estimates on Photronics - why the stock might be worth as much as 44% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Photronics research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Photronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Photronics' overall financial health at a glance.

Want Some Alternatives?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com