- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

How Leadership Turmoil And A Potential STAR Sale At Fiserv (FISV) Has Changed Its Investment Story

- In early July 2026, Fiserv, Inc. saw President Dhivya Suryadevara resign for good reason under her offer letter, while Executive Vice President Andrew Gelb and technology leader Srini Krish stepped in as interim heads of the Financial Solutions business.

- These leadership changes arrived alongside reports that Fiserv is exploring a sale of its STAR payment network, a move that could materially reshape the company’s portfolio focus and capital allocation priorities.

- We’ll now examine how the potential STAR network sale could influence Fiserv’s existing investment narrative and long-term business priorities.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Fiserv Investment Narrative Recap

To own Fiserv, you need to believe it can compound value by modernizing bank technology and scaling merchant payments, even as growth expectations have already been trimmed. The potential STAR network sale and Dhivya Suryadevara’s resignation appear meaningful for portfolio focus and leadership continuity, but they do not yet obviously change the near term execution risk around product rollouts, or the pressure from slower organic growth and recent margin compression.

The recent embedding of Personetics’ AI platform into Fiserv’s Experience Digital (XD) ties directly into that execution risk: XD is one of the company’s key next generation platforms. Successful adoption of these AI driven capabilities by banks and credit unions could support the existing catalyst of better monetizing software and data across the installed base, even as investors monitor whether leadership changes affect the pace and quality of these implementations.

Yet against this, investors should be aware that...

Read the full narrative on Fiserv (it's free!)

Fiserv's narrative projects $21.8 billion revenue and $3.7 billion earnings by 2029.

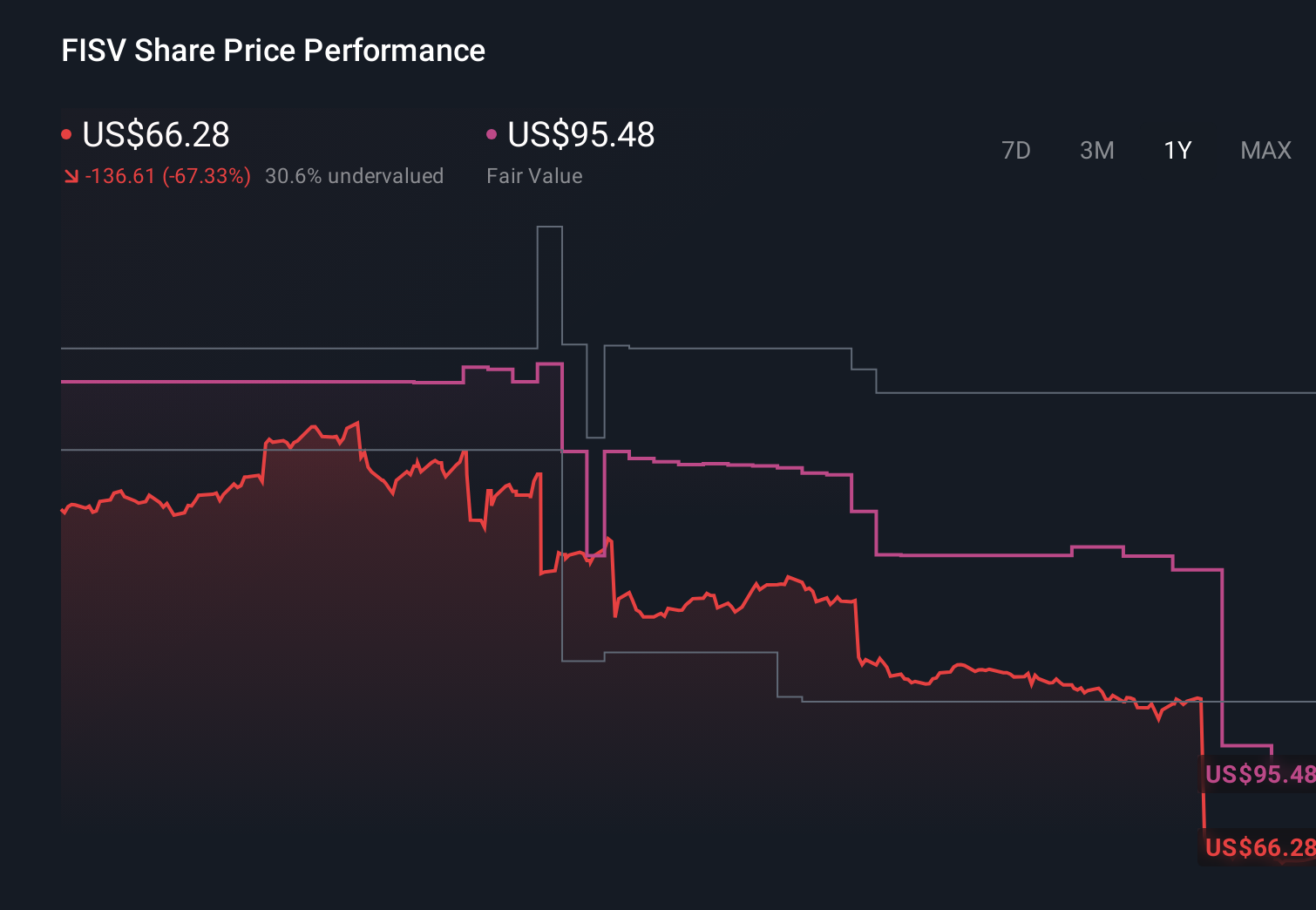

Uncover how Fiserv's forecasts yield a $68.48 fair value, a 36% upside to its current price.

Exploring Other Perspectives

Before this leadership shake up, the most optimistic analysts were banking on earnings reaching about US$4.1 billion by 2029, but if product launch delays persist, you may decide that this much rosier narrative deserves a closer second look.

Explore 17 other fair value estimates on Fiserv - why the stock might be worth 21% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Fiserv research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Fiserv research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Fiserv's overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find 45 companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com