- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

3M (MMM) Stock May Be 26% Undervalued On PFAS Lawsuit Risk

3M stock has more than doubled over the past three years, and today both the Discounted Cash Flow (DCF) intrinsic value estimate and market multiples indicate the shares may still be pricing in a discount rather than a premium.

- 3M has returned 102.1% over the past three years, which puts extra focus on whether the current price still leaves a margin between market value and intrinsic value.

- The new partnership as Official Material Science Partner of the Cadillac Formula 1 Team can support expectations for future cash flows, while the New York Attorney General's PFAS lawsuit highlights legal and remediation risks that may weigh on how investors assess those same cash flows.

- 3M scores 3 out of 6 on our valuation checks, which points to a mixed picture rather than a clear bargain or clear overvaluation.

The issue now is whether the current discount suggested by both the DCF intrinsic value estimate and earnings multiples offers enough compensation for the legal and operational risks in front of 3M.

Is 3M Still Cheap on Cash Flow?

The Discounted Cash Flow (DCF) model values 3M by projecting future free cash flows and discounting them back to today. On this view, 3M is treated as a mature business with recovering cash generation, moving from last twelve month free cash flow of about $1.8b to projected annual cash flows in the mid single digit billions over the coming decade.

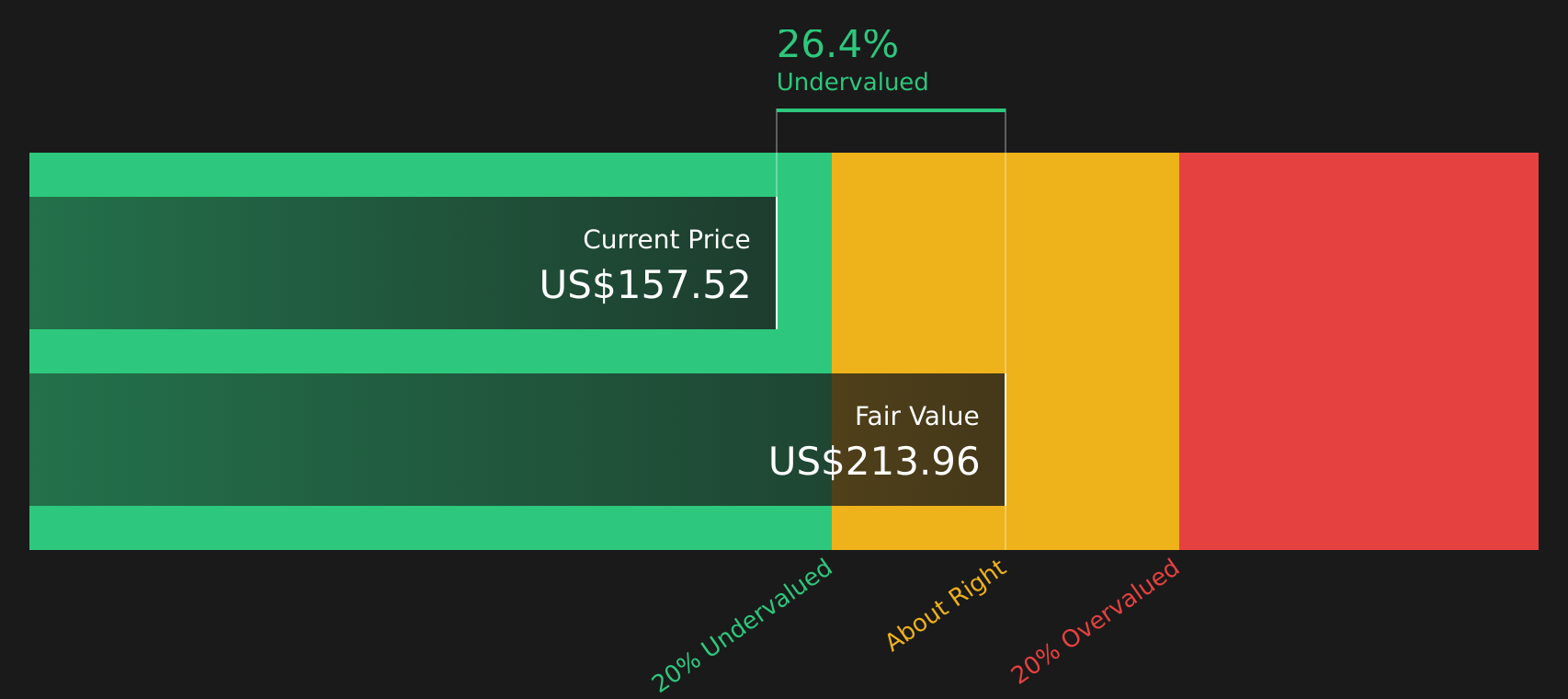

Those projections translate into an estimated intrinsic value of about $214 per share, which implies the stock trades at roughly a 26.4% discount to the DCF value. The New York Attorney General's PFAS lawsuit helps explain why the market keeps 3M below this intrinsic estimate, as potential remediation costs can weigh on how investors treat those projected cash flows.

Overall, the DCF workup suggests 3M stock appears undervalued relative to the cash flows currently included in the model.

Our Discounted Cash Flow (DCF) analysis suggests 3M is undervalued by 26.4%. Track this in your watchlist or portfolio, or discover 45 more high quality undervalued stocks.

Does 3M Look Undervalued on Earnings?

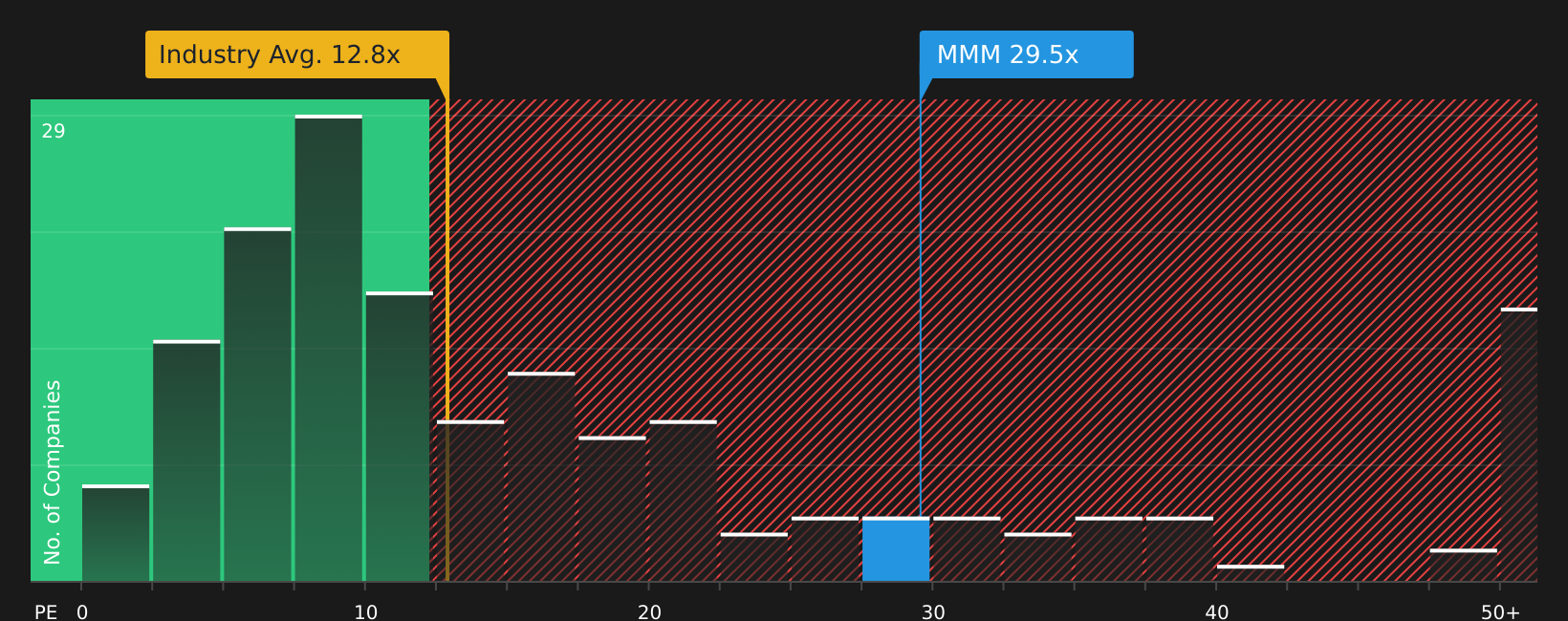

P/E tends to suit 3M because earnings remain a central yardstick for mature industrial companies. On this metric, 3M trades on a P/E of about 29.5x, slightly above the peer average of 28.2x and well above the wider Industrials sector average of 12.8x. As a result, the stock does not look optically cheap against broad industry benchmarks.

However, Simply Wall St's fair P/E estimate for 3M is higher, at about 33.6x. This fair ratio reflects what investors might be prepared to pay given the company's profile. It also sits a few turns above where the stock is currently priced, which suggests a discount on this more tailored yardstick despite the premium to sector averages.

On the P/E multiple, 3M stock currently appears undervalued relative to the fair ratio implied by its fundamentals and risk profile.

See what the numbers say about this price — find out in our valuation breakdown.

The 3M Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where this 3M valuation puzzle leaves off by spelling out which paths for 3M's growth, margins and earnings would line up with the stock being worth materially more or less than today's price, and they sit on the company's Community page. Each narrative links its number to a clear view of how 3M's growth, profitability and risks might evolve, giving you a reference point you can revisit as new information comes through.

The community is split on 3M, with one camp leaning toward a discount story and the other focused on lingering legal and restructuring pressure.

Bull case: 8% undervalued

"The acceleration in new product launches (up 70% YoY; targeting 215 for the year) and a 9% rise in five-year innovation sales, expected to surpass 15% growth for the year, positions 3M to capitalize on rising global needs for health, safety, digitalization, and sustainably-driven products, which could support both future revenue growth and margin expansion."

Read the full Bull Case to see why 3M could be undervalued

Bear case: 23% overvalued

"Intensifying regulatory and litigation headwinds related to environmental hazards, particularly PFAS, are likely to burden 3M with continued high legal, settlement, and compliance costs throughout the next decade, directly eroding free cash flow and depressing net income as liabilities could extend or escalate well beyond current settlements."

Read the full Bear Case to see why 3M could be overvalued

Do you think there's more to the story for 3M? Head over to our Community to see what others are saying!

The Bottom Line

For 3M, both the Discounted Cash Flow (DCF) intrinsic value estimate and the tailored earnings multiple point to the stock screening as undervalued, even if broader checks look mixed rather than emphatic. That discount exists alongside ongoing legal and remediation uncertainties, which are central to how investors treat future cash flows. The key question from here is whether those risks eventually ease enough for the market to close some of the implied valuation gap, or whether the current pricing is a fair reflection of the long tail of potential liabilities.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com