- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Pool (POOL) Stock Looks Cheap On Cash Flow While Earnings Look Rich

Pool stock is caught between two valuation stories right now, with a Discounted Cash Flow (DCF) intrinsic value estimate that points to meaningful upside while the market’s earnings multiples suggest the shares already trade at a premium. After several years of weak share price performance, investors are being asked to decide which lens to trust.

- Pool has declined 50.9% over the last 5 years, which sets expectations low and makes today’s valuation more sensitive to any change in sentiment about its long term earnings power.

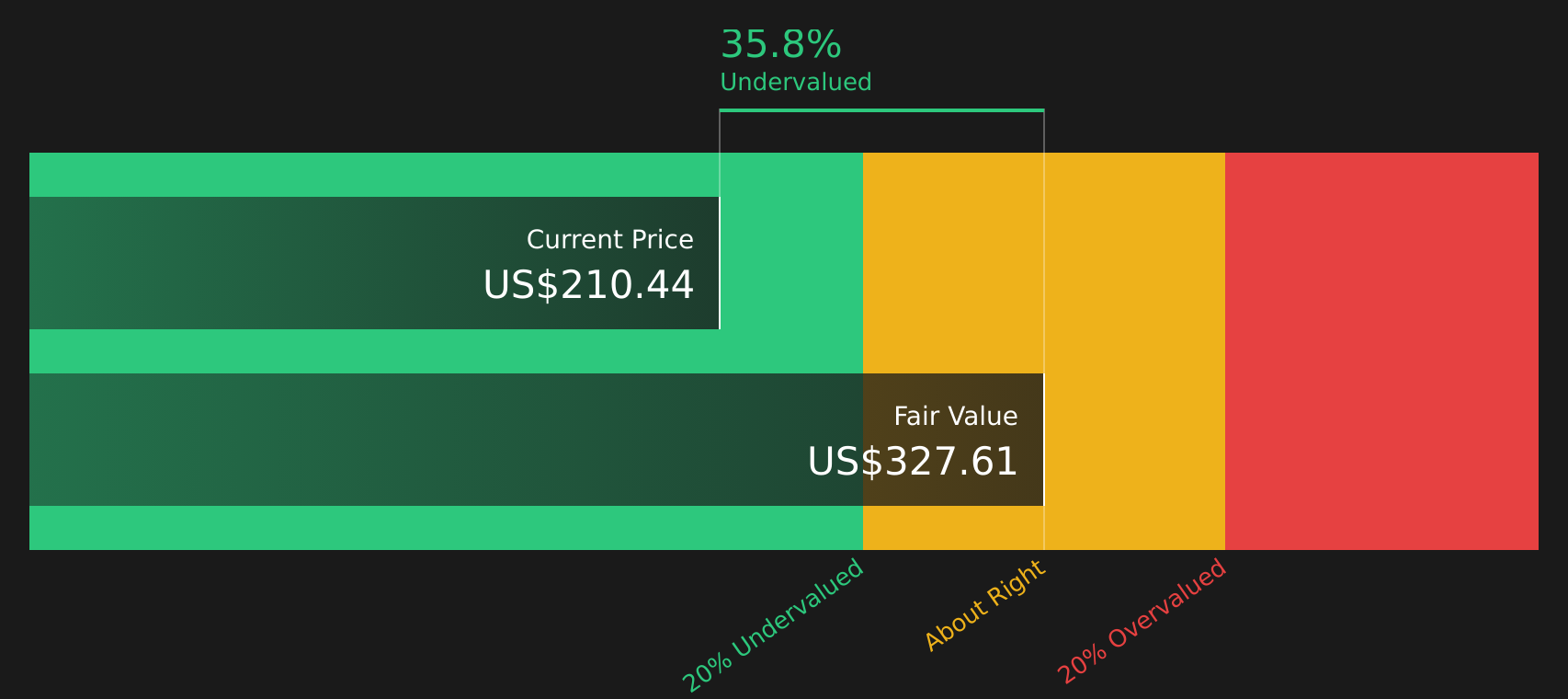

- The DCF intrinsic value estimate indicates the stock may trade at roughly a 35.8% discount to its modeled cash flows, but the richer read from market multiples highlights concern that current earnings may not fully support that gap.

- On the broader checks, Pool scores 3 out of 6 for value, which points to a mixed picture rather than a clear bargain or clear overvaluation.

The issue now is whether Pool’s current share price lines up more closely with the intrinsic value suggested by cash flow estimates or with the tighter view implied by its market multiples.

Find out why Pool's -29.8% return over the last year is lagging behind its peers.

Is Pool Still Cheap on Cash Flow?

The Discounted Cash Flow (DCF) model estimates what Pool is worth today based on the cash it is expected to generate in the future. For Pool, the model uses latest twelve month free cash flow of about $308.1 million and assumes cash flows continue to grow rather than contract, consistent with a mature but still expanding business profile.

On these assumptions, the DCF indicates an intrinsic value of about $328 per share, which is roughly 35.8% above the current share price. That difference suggests the market is applying a more cautious view of Pool’s ability to sustain or build on its current cash generation than the model does, even though the cash flow inputs used here are not extreme or high growth forecasts.

On this cash flow view, Pool stock appears undervalued relative to the DCF estimate of intrinsic worth.

Our Discounted Cash Flow (DCF) analysis suggests Pool is undervalued by 35.8%. Track this in your watchlist or portfolio, or discover 45 more high quality undervalued stocks.

Has Pool Run Too Far on Earnings?

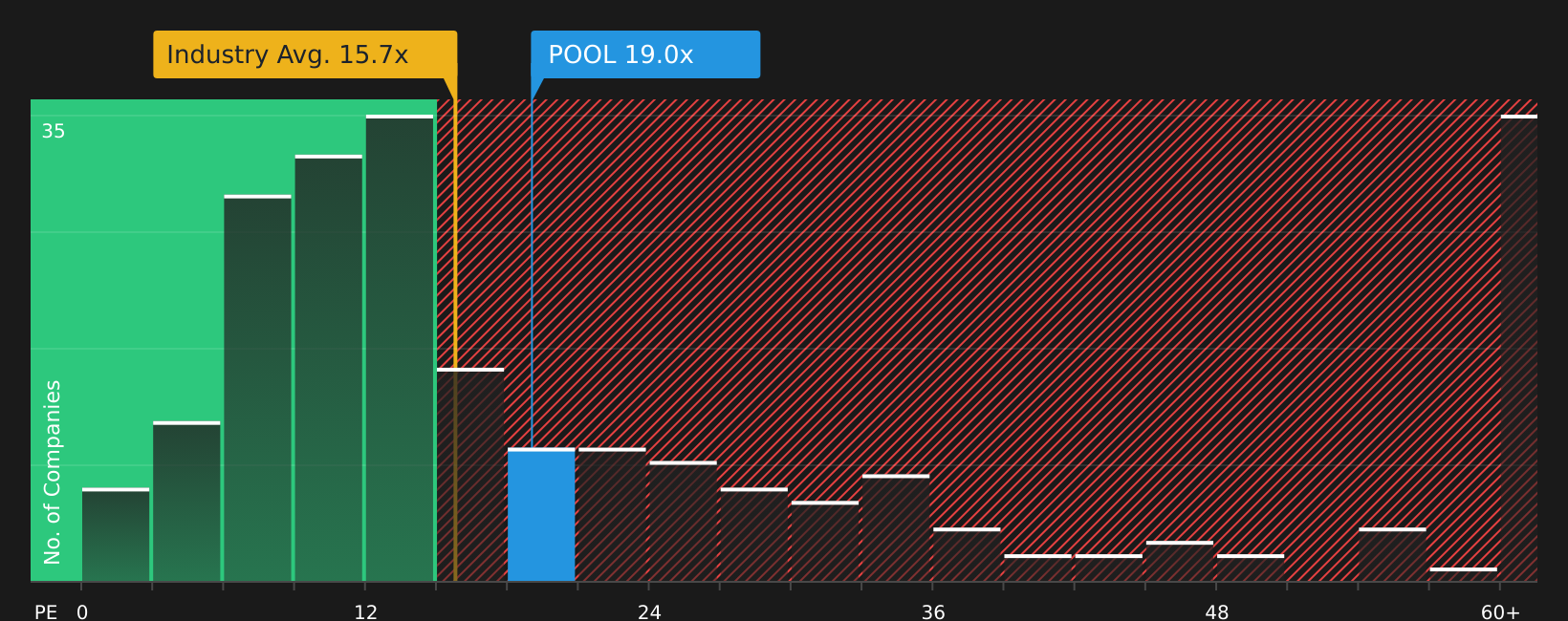

The P/E ratio is a useful cross check for Pool because earnings are still a core yardstick for how the market is pricing the stock. Pool currently trades on a P/E of about 19.0x, compared with roughly 15.7x for the wider Retail Distributors industry and a peer average of around 12.6x.

The tailored fair P/E ratio for Pool, which blends factors such as its sector, size and risk profile, is lower at about 13.8x. Set against today’s P/E, that indicates investors are paying a clear premium to the earnings level that this framework would usually support, even before considering any further change in sentiment.

Based on earnings alone, Pool stock appears overvalued relative to both its industry and this fair value benchmark.

See what the numbers say about this price — find out in our valuation breakdown.

The Pool Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Pool pick up where this valuation puzzle leaves off by spelling out which assumptions about Pool's future growth, margins and earnings would need to hold for the stock to be worth materially more or less than its current price. Each narrative links a fair value estimate to a specific story about Pool's potential catalysts and risks, so you can track over time which version of events appears to be taking shape.

One of the top community narratives on Pool: 30% undervalued

"Resilient maintenance demand, which represented about 64% of 2025 pool product sales, together with an installed base that grew by an estimated 60,000 new U.S. pools in 2025, supports a larger recurring revenue pool that can feed both top line and more stable earnings over time..."

Read one of the top narratives on Pool

Do you think there's more to the story for Pool? Head over to our Community to see what others are saying!

The Bottom Line

Pool sits between an intrinsic value view that screens as undervalued on Discounted Cash Flow (DCF) and an earnings multiple view that looks overvalued versus peers and a tailored fair P/E. That split largely reflects the DCF focusing on cash generation and capital needs, while the market is anchoring more on current growth expectations and sentiment toward the sector. With broader checks landing in mixed territory, the key question from here is whether Pool can sustain cash flows strongly enough to close the gap to the intrinsic value estimate, or whether the current earnings multiple proves too rich if that does not play out.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com