- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Whirlpool (WHR) Plant Closure Puts Fair Value Narrative Back In Focus

Whirlpool (WHR) is back in focus after announcing plans to close its Supsa plant in Apodaca, Mexico, shift production to other sites, and absorb about US$165 million in related restructuring charges.

See our latest analysis for Whirlpool.

The restructuring news comes after a sharp move in Whirlpool’s share price, with a 1 day share price return of 7.55% and a 7 day share price return of 6.88%, set against a much weaker 90 day share price return that fell 27.32% and a 1 year total shareholder return that declined 61.11%. This suggests recent momentum is improving from a low base.

If you are weighing Whirlpool’s reset against other opportunities in industrial technology, this could be a useful moment to scan 31 robotics and automation stocks.

Whirlpool now trades well below both analyst targets and one intrinsic value estimate, even after the recent rebound. Is the discount a signal that the market is too cautious, or a warning that it is not cautious enough?

Most Popular Narrative: 27.4% Undervalued

The most followed Whirlpool narrative sees fair value at $56.10 per share, compared with a last close of $40.72, leaning heavily on restructuring and product mix improvement to close that gap.

Recent and ongoing restructuring, cost takeout programs, and supply chain efficiencies are expected to deliver structural operating margin improvement, even as current headwinds fade.

Want to see what supports that margin story and valuation gap for Whirlpool? The core of this narrative blends modest revenue growth, higher profitability and a richer earnings multiple into one tight forecast. Curious which assumptions really move the fair value line here? The full narrative lays out the blueprint investors are using to back that $56.10 figure.

Result: Fair Value of $56.10 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Whirlpool’s reliance on mature markets and heightened competition from lower cost manufacturers could pressure margins and delay the kind of earnings improvement this narrative assumes.

Find out about the key risks to this Whirlpool narrative.

Another View on Whirlpool’s Valuation

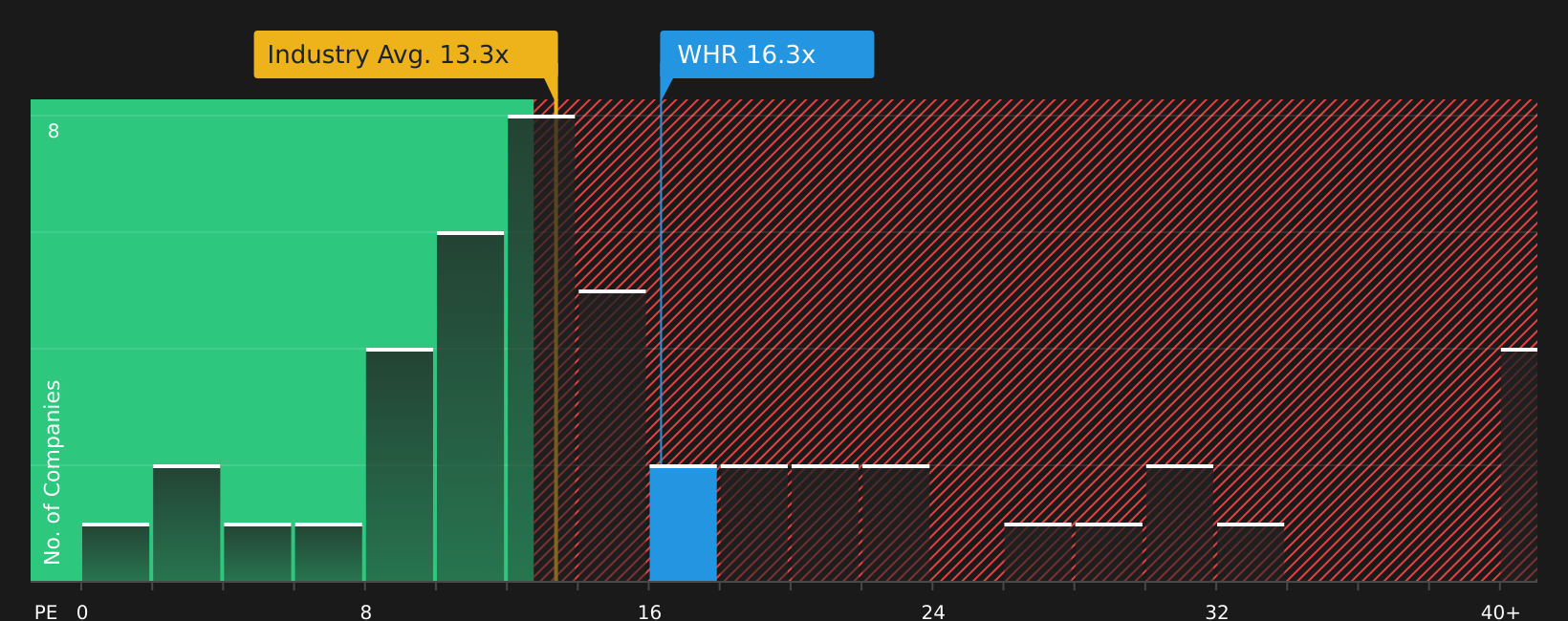

The earlier narrative leans on fair value of $56.10 per Whirlpool share, but the current P/E of 16.3x tells a different story. That multiple sits above both peer averages of 14.8x and the US Consumer Durables industry at 13.3x, even though the fair ratio points to 28.3x as a level the market could move toward. For investors, that mix of apparent discount and richer current multiple raises a simple question: is Whirlpool cheap relative to its cash flows or already pricing in a lot of the recovery case?

To unpack what this P/E gap really means for your risk and opportunity, it helps to see how earnings, pricing and expectations fit together in a structured valuation breakdown, not just a single headline multiple. See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment split between Whirlpool’s challenges and its potential rewards, this is a good time to review the latest data for yourself, decide where you stand, and then pressure test that view by checking the 3 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Whirlpool?

If Whirlpool has you rethinking your portfolio, do not stop here. Some of the most useful opportunities often show up when you widen the search and compare.

- Target stronger long term potential by scanning companies that currently look attractively priced using the 45 high quality undervalued stocks.

- Build a steadier income stream by reviewing stocks highlighted in the 9 dividend fortresses.

- Sleep easier at night by focusing on companies that pass strict resilience checks with the 77 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com