- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

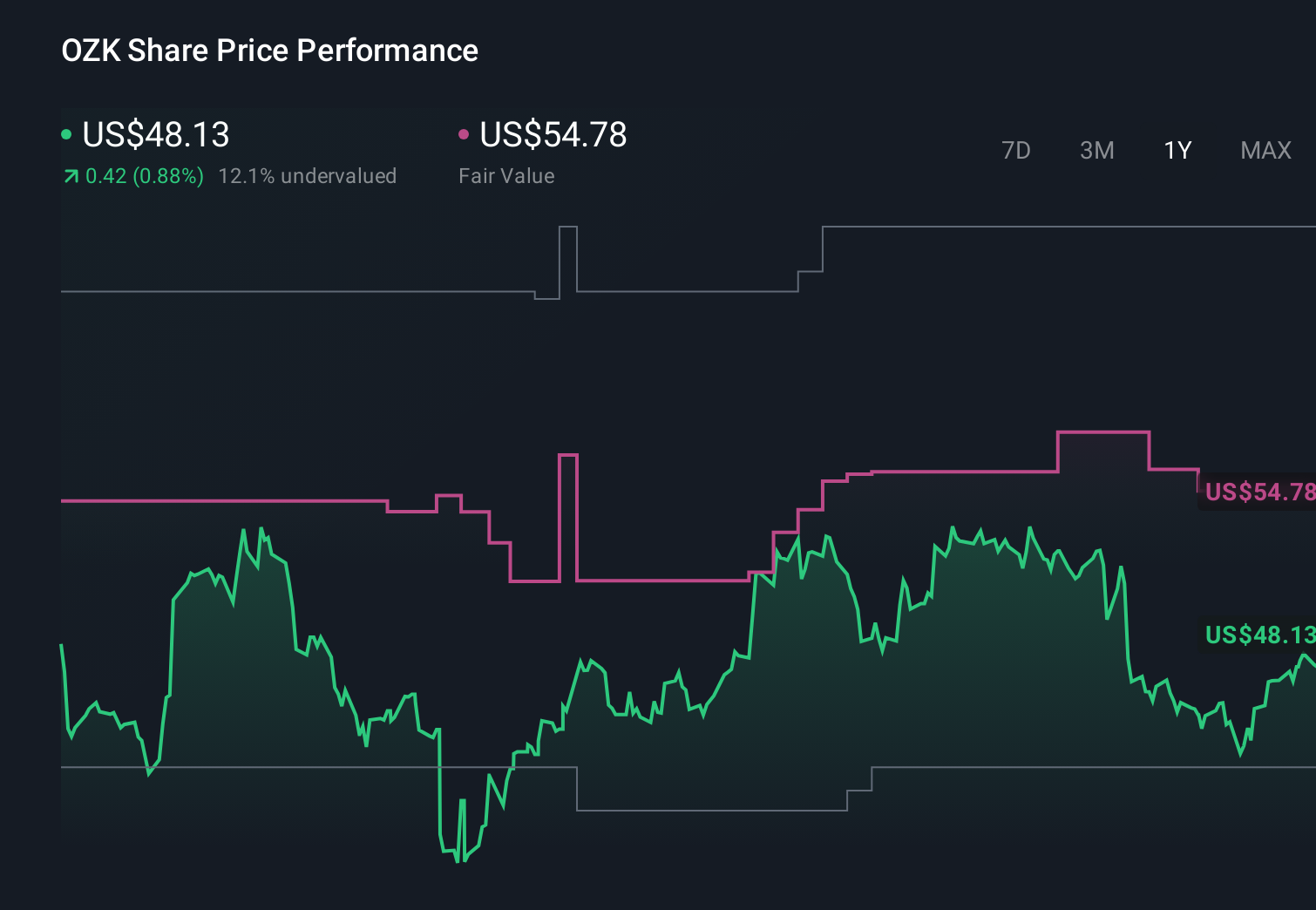

The Bull Case For Bank OZK (OZK) Could Change Following New Buyback And Dividend Hike News

- Bank OZK recently announced that its Board of Directors approved a new quarterly common dividend of US$0.48 per share, marking its sixty-fourth consecutive quarterly increase, alongside a preferred dividend of US$0.28906 per share and the expiration of its prior share repurchase plan.

- At the same time, the Board authorized a fresh share buyback program of up to US$200 million through July 1, 2027, underscoring an ongoing focus on returning capital to shareholders via both dividends and repurchases.

- We’ll now examine how the newly authorized US$200 million share repurchase program may influence Bank OZK’s existing investment narrative.

Find 44 companies with promising cash flow potential yet trading below their fair value.

Bank OZK Investment Narrative Recap

To own Bank OZK, you need to be comfortable with a bank that leans heavily on commercial real estate lending, while trying to balance growth, credit quality, and operating efficiency. The new US$0.48 dividend and US$200 million buyback authorization signal continued capital returns, but they do not materially change the near term story, where the key catalyst is upcoming earnings and the biggest risk remains asset quality if commercial real estate conditions weaken.

The newly authorized US$200 million repurchase program is the most relevant update here, sitting alongside a long-running pattern of quarterly dividend increases. For investors focused on catalysts, this program could modestly influence per share metrics if executed alongside earnings stability, but it does not reduce exposure to concentrated commercial real estate lending or potential pressure on margins from branch expansion and competition.

However, alongside these capital returns, there is an important risk investors should be aware of around concentrated exposure to commercial real estate and...

Read the full narrative on Bank OZK (it's free!)

Bank OZK's narrative projects $2.1 billion revenue and $727.8 million earnings by 2029. This requires 9.8% yearly revenue growth and about a $37.1 million earnings increase from $690.7 million today.

Uncover how Bank OZK's forecasts yield a $52.33 fair value, a 3% upside to its current price.

Exploring Other Perspectives

While recent buybacks and dividend hikes may appeal, the most pessimistic analysts still assume only US$2.1 billion of revenue and US$717.8 million of earnings by 2029, highlighting how differently you might view credit risk tied to commercial real estate.

Explore 5 other fair value estimates on Bank OZK - why the stock might be worth 18% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Bank OZK research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Bank OZK research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank OZK's overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com