- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

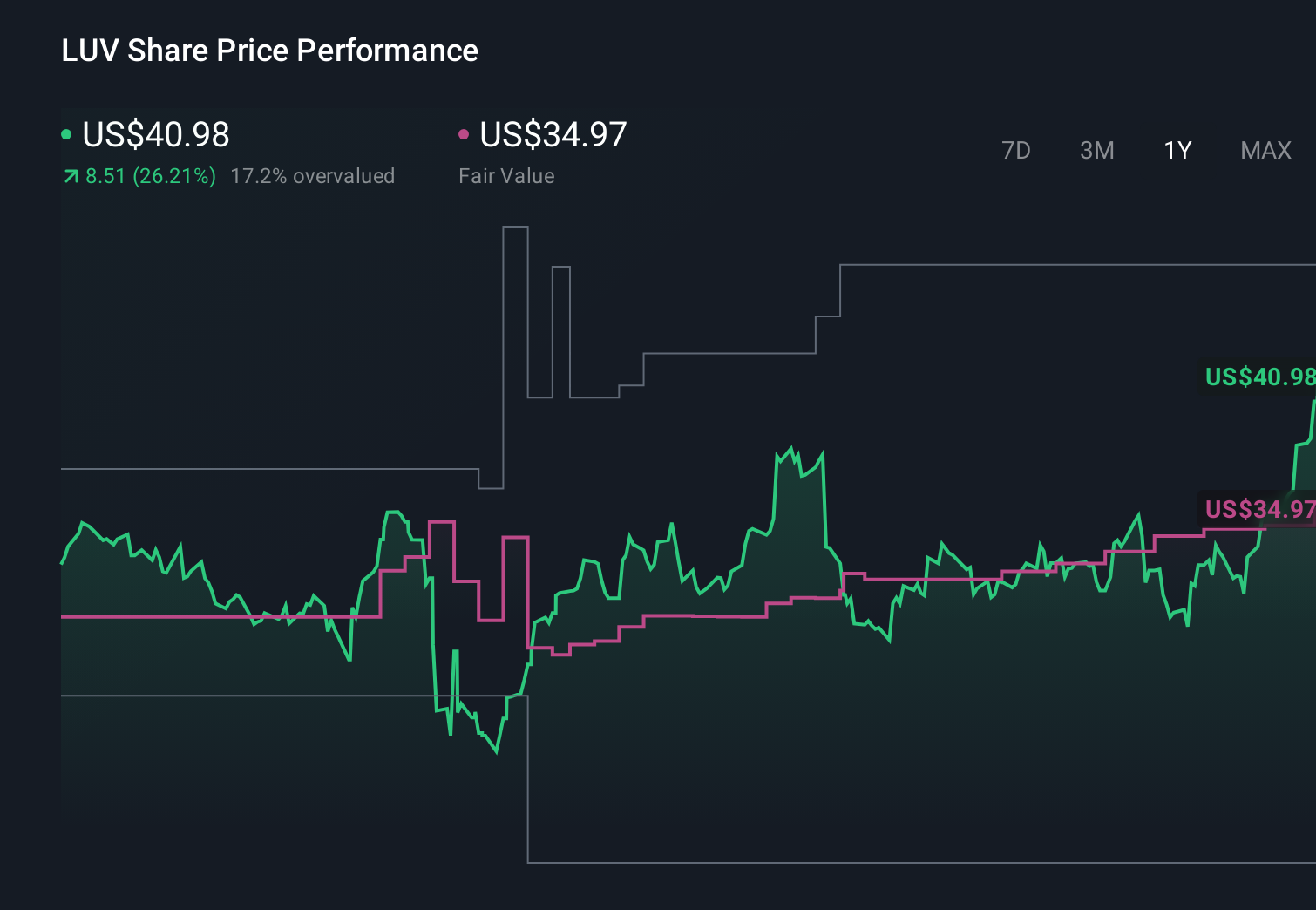

Is New Klarna Partnership And Air Premia Tie-Up Altering The Investment Case For Southwest (LUV)?

- In early July 2026, Klarna Group plc and Southwest Airlines Co. announced a long-term partnership to offer flexible, transparent payment options for flights booked via Southwest’s website and app, while an interline agreement with Korea’s Air Premia opened single-ticket access from South Korea to more than 120 Southwest destinations through Los Angeles, San Francisco, and Honolulu.

- Together, these partnerships give Southwest deeper reach into East Asian demand and more flexible payment choices for millions of U.S. travelers, potentially enhancing its appeal versus other carriers.

- Next, we’ll examine how Southwest’s new Klarna-powered payment flexibility could influence the company’s broader investment narrative and risk-reward profile.

Find 44 companies with promising cash flow potential yet trading below their fair value.

Southwest Airlines Investment Narrative Recap

To own Southwest, you need to believe its transformation efforts can lift earnings despite macro uncertainty, cost inflation, and aircraft supply constraints. The Klarna and Air Premia deals support the near term catalyst of broadening demand channels and improving revenue quality, but they do little to offset key risks such as potential fuel cost volatility and possible customer pushback around new fees and product changes.

Among recent developments, the Singapore Airlines partnership best frames these new announcements, because it also extends Southwest’s reach through single ticket itineraries to roughly 120 domestic destinations. Together with Air Premia and Klarna, it reinforces the catalyst around expanding higher value distribution and international feed, while investors still need to watch how these gains interact with rising operating costs and any softness in U.S. leisure demand.

Yet alongside these growth angles, investors should be aware that rising fuel and labor costs could still pressure margins if...

Read the full narrative on Southwest Airlines (it's free!)

Southwest Airlines' narrative projects $34.5 billion revenue and $2.3 billion earnings by 2029. This requires 6.1% yearly revenue growth and about a $1.5 billion earnings increase from $817.0 million today.

Uncover how Southwest Airlines' forecasts yield a $47.51 fair value, in line with its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming only about 2.1 percent annual revenue growth to roughly US$30.8 billion, with earnings of about US$2.0 billion by 2029, so compared with the more constructive consensus catalysts around partnerships and product changes, this is a much more cautious story that you should weigh against the new Klarna and Air Premia news.

Explore 5 other fair value estimates on Southwest Airlines - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Southwest Airlines research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Southwest Airlines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southwest Airlines' overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com