- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

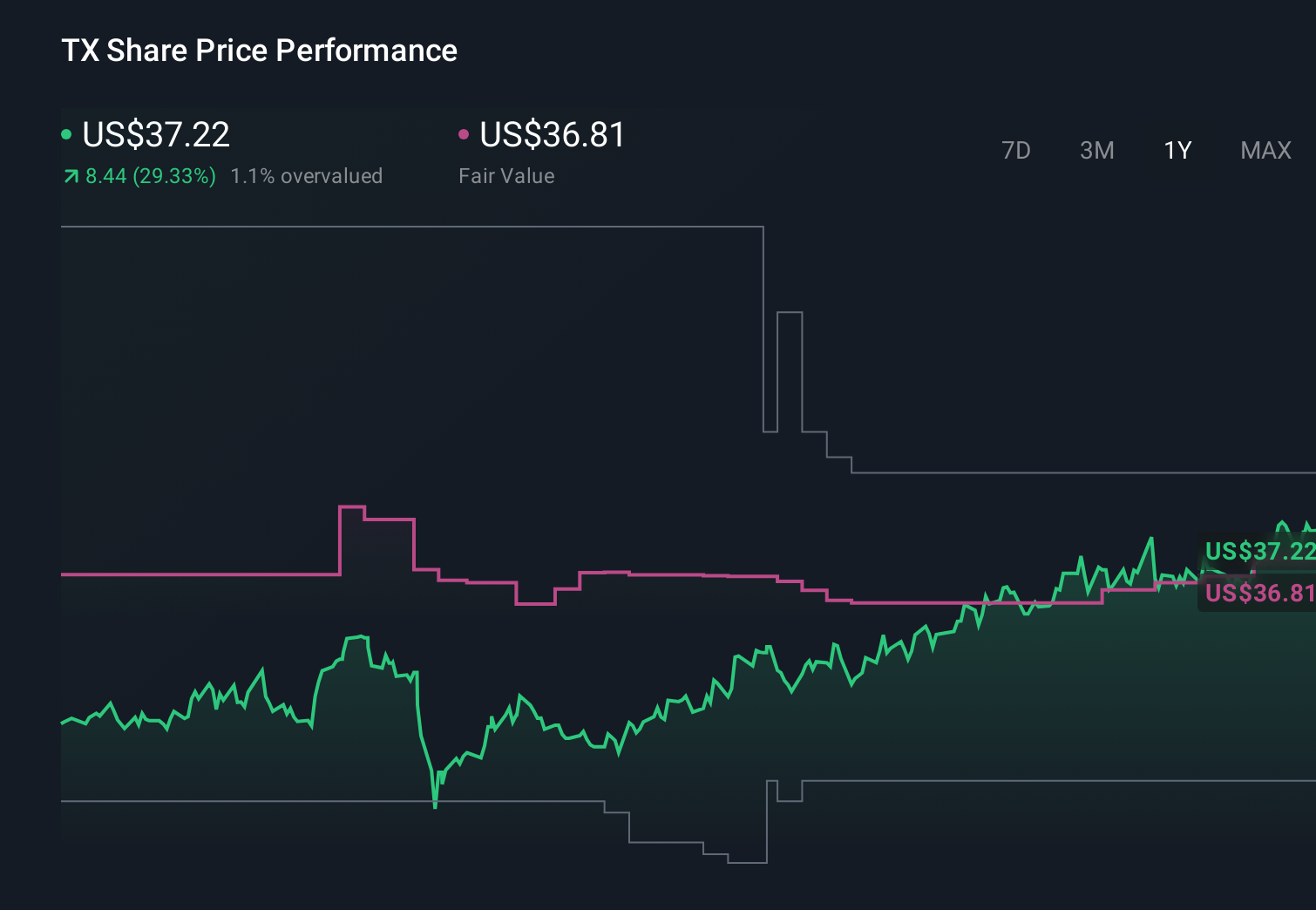

Ternium (TX) Is Up 6.1% After Wells Fargo Upgrade on Mexico Outlook and Capacity Plans - What's Changed

- Earlier this week, Wells Fargo upgraded Ternium S.A. to Equal Weight from Underweight after the company’s first-quarter 2026 earnings beat analyst expectations, citing contributions from new capacity expected in 2027 and improving Mexican market conditions.

- The upgrade underscores how Ternium’s expansion plans and recent operational performance are beginning to influence external views of its long-term positioning in Latin American steel.

- Next, we’ll explore how Wells Fargo’s upgrade, tied to new capacity plans and Mexico’s improving backdrop, reshapes Ternium’s investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Ternium Investment Narrative Recap

To own Ternium, you need to believe its Latin American footprint and Mexico focused expansion can support resilient cash generation despite cyclical steel markets and heavy capex needs. Wells Fargo’s upgrade after the Q1 2026 earnings beat reinforces confidence in the near term catalyst of new capacity coming online, but it does not remove key risks around global overcapacity, import pressure and the strain from Ternium’s multi year US$4 billion investment cycle.

The most relevant recent development alongside Wells Fargo’s upgrade is Ternium’s Q1 2026 result, where net income rose to US$213 million from US$67 million a year earlier on broadly flat sales. That step up in profitability gives more support to the expansion and cost efficiency catalysts, but it also sits against a backdrop of reduced dividends intended to protect the balance sheet as spending at Pesqueria ramps and free cash flow remains under pressure.

Yet behind the earnings momentum, investors should be aware of how prolonged global overcapacity or delays at Pesqueria could suddenly change that picture...

Read the full narrative on Ternium (it's free!)

Ternium's narrative projects $18.7 billion revenue and $1.5 billion earnings by 2029. This requires 6.2% yearly revenue growth and about a $0.9 billion earnings increase from $571.3 million today.

Uncover how Ternium's forecasts yield a $53.12 fair value, a 20% upside to its current price.

Exploring Other Perspectives

While Wells Fargo is warming up to Ternium after its Q1 beat, the most cautious analysts still saw a tougher road, with revenue only reaching about US$17.3 billion and earnings about US$1.1 billion by 2029. Compared with the consensus narrative that leans on Mexico expansion and cost cuts, this more pessimistic view highlights heavier decarbonization costs and overcapacity risk, reminding you that reasonable people can read the same news very differently.

Explore 3 other fair value estimates on Ternium - why the stock might be worth as much as 31% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Ternium research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Ternium research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ternium's overall financial health at a glance.

Searching For A Fresh Perspective?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com