- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

How Investors May Respond To Boot Barn (BOOT) Expansion Plans And Rising Options-Market Volatility

- In recent months, Boot Barn Holdings outlined plans to open 70 new stores in fiscal 2027 while pushing exclusive brands beyond 40% of sales, aiming to balance physical expansion with differentiated merchandise and ongoing digital execution.

- At the same time, unusually active options trading with high implied volatility around Boot Barn’s August 2026 calls highlights shifting investor expectations as earnings estimates are re-examined.

- We’ll now examine how Boot Barn’s planned store expansion and growing mix of exclusive brands may influence its existing investment narrative.

AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Boot Barn Holdings Investment Narrative Recap

To own Boot Barn, you have to believe its store led growth, Western and workwear focus, and rising exclusive brand mix can support durable profitability without overextending the footprint. The plan to open 70 new stores in fiscal 2027 and push exclusive brands beyond 40% of sales aligns with that thesis. Recent options activity with high implied volatility does not materially change the near term catalyst, which is execution on store productivity, or the biggest risk, which is overexpansion.

Among recent updates, the fiscal 2027 outlook stands out as most relevant. Management now expects sales of about US$2.58 billion to US$2.62 billion with consolidated same store sales growth of 2% to 4%, while continuing to lean into e commerce and exclusive brands. For investors, the key question is whether these growth targets can be met without pressuring net margins through higher occupancy costs and potential store cannibalization in newer markets.

Yet the risk that aggressive store growth could raise costs faster than profits is something investors should be aware of as...

Read the full narrative on Boot Barn Holdings (it's free!)

Boot Barn Holdings' narrative projects $3.3 billion revenue and $350.9 million earnings by 2029. This requires 13.9% yearly revenue growth and about a $125 million earnings increase from $225.9 million today.

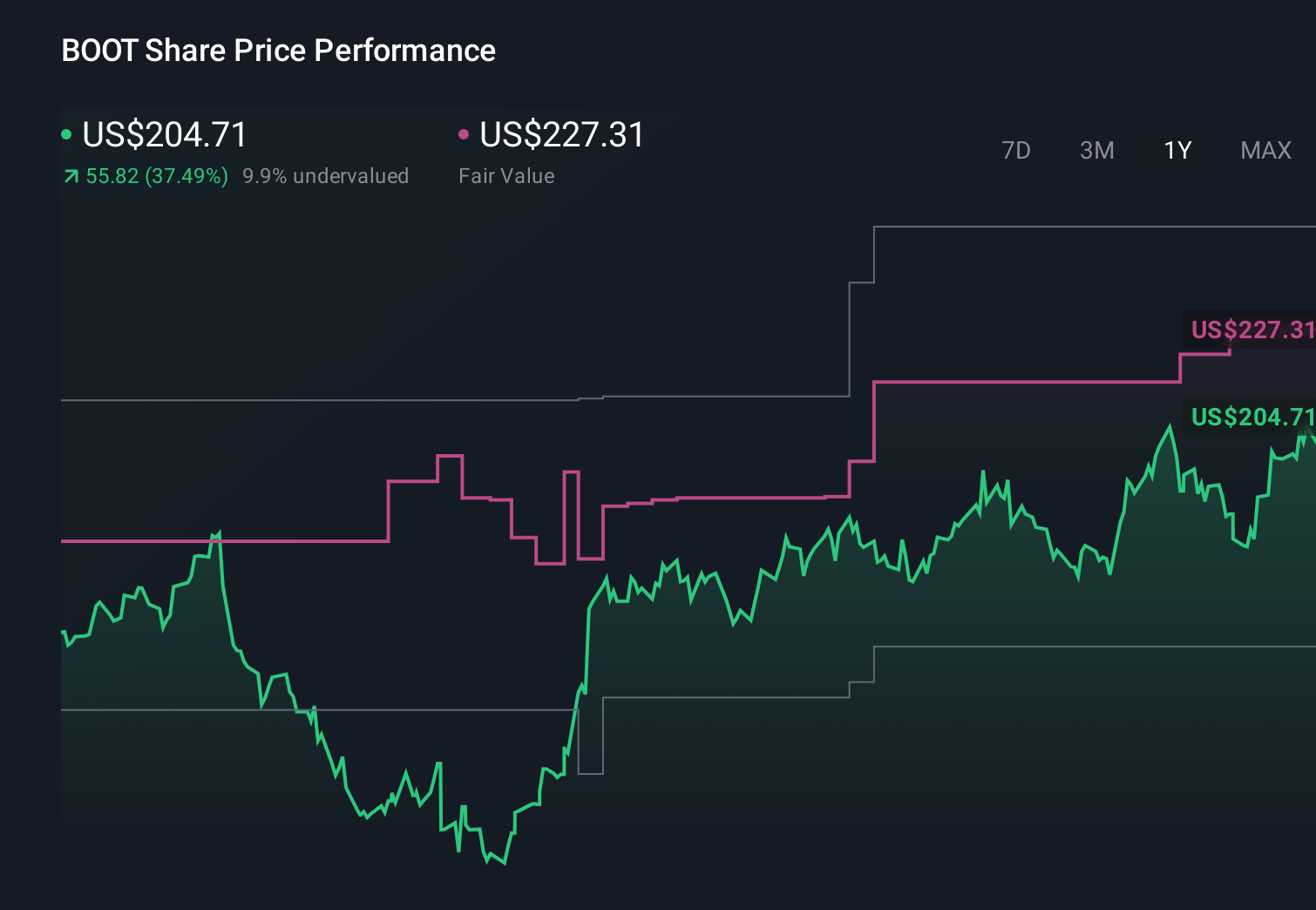

Uncover how Boot Barn Holdings' forecasts yield a $225.14 fair value, a 40% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts already assumed only about US$3.3 billion of revenue and US$336 million of earnings by 2029, so you should recognize that they paint a much more cautious picture on store expansion and margin resilience than the consensus and consider how this latest store growth update might shift those expectations.

Explore 4 other fair value estimates on Boot Barn Holdings - why the stock might be worth 46% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Boot Barn Holdings research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Boot Barn Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boot Barn Holdings' overall financial health at a glance.

Ready For A Different Approach?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com