- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Grab Stock And Other Penny Shares With Stronger Balance Sheets

Penny stocks sit at the intersection of opportunity and risk, which is why a focus on financial strength can matter even more when inflation paths, interest rate expectations, and energy costs are pulling markets in different directions. The Financially Fit Penny Stocks screener filters for lower priced companies with relatively healthier balance sheets, so you are not just chasing a low share price in a volatile macro backdrop. In this article, you will see three stocks from this screener that stand out on financial quality grounds. This can give you a starting list for deeper research into this higher risk corner of the market.

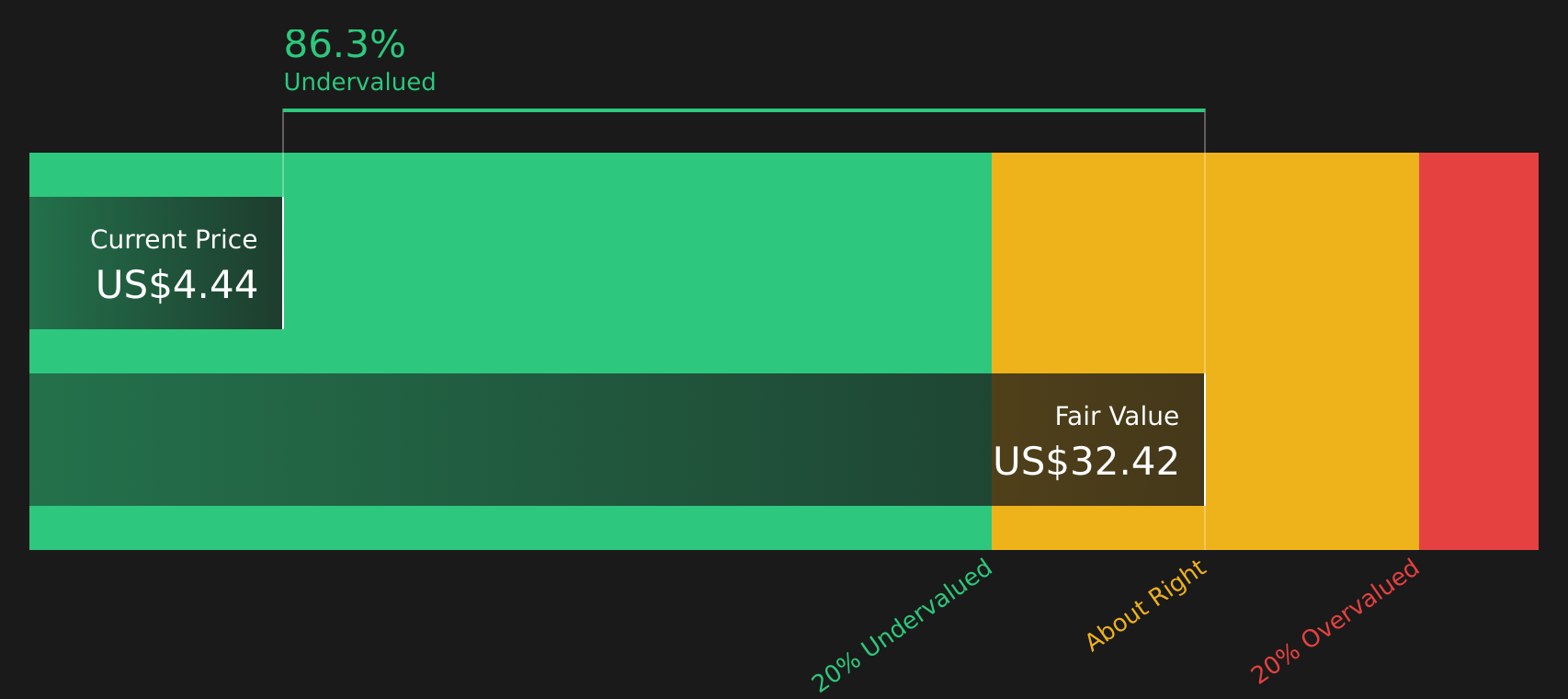

Grab Holdings (GRAB)

Overview: Grab Holdings runs a super app across Southeast Asia that brings together ride-hailing, food and package delivery, digital payments, banking and insurance services, plus tools for merchants and advertisers in a single ecosystem.

Operations: Grab generates most of its US$3.6b revenue from Deliveries (US$1.9b) and Mobility (US$1.3b), with smaller contributions from Financial Services (US$379m) and Others (US$4m).

Market Cap: US$15.9b

Investors looking at Grab Holdings are getting exposure to a leading Southeast Asian super app that is already profitable, with net profit margins at 10.7% and earnings growth that has recently been very large compared to its 5 year average. At the same time, the stock is flagged as trading well below one estimate of fair value. Analysts on average also expect earnings and revenue to keep rising faster than the wider US market. The flip side is that a high P/E ratio, heavy use of non cash earnings and a funding structure built mainly on external borrowing raise questions about earnings quality and resilience. That mix of strong progress and real risk is what makes Grab worth a closer look.

Grab Holdings’ profitability, high P/E and heavy non cash earnings make its story feel incomplete, and the real twist sits inside the analysis report for Grab Holdings

Clover Health Investments (CLOV)

Overview: Clover Health Investments offers Medicare Advantage plans in the United States and uses its Clover Assistant software to help physicians spot and manage chronic diseases, aiming to improve care quality while controlling medical costs.

Operations: Clover Health Investments generates about US$2.2b in revenue from its Insurance segment, entirely from the United States.

Market Cap: US$2.5b

Clover Health Investments gives you exposure to a Medicare-focused insurer that pairs fast-growing membership with a technology centered care model, which analysts link to better medical cost control and higher potential margins. The stock screens as inexpensive on P/S and discounted against one cash flow estimate; however, expectations are already high, with analysts building in strong revenue and earnings growth and a richer P/E multiple years out. At the same time, the business is still loss making, faces rising medical and pharmacy costs, and relies heavily on Medicare Advantage funding and regulatory support. That mix of upside tied to value based care and real questions about profitability, policy risk, and insider selling is why Clover Health deserves closer scrutiny in a higher risk penny stock basket.

Clover Health’s growth story, powered by Medicare and its software led care model, looks like it is still missing a crucial chapter: the analyst forecasts for Clover Health Investments hint at how expectations, policy risk and margins may really fit together

Hyliion Holdings (HYLN)

Overview: Hyliion Holdings develops the KARNO Power Module, a fuel flexible generator that can produce on site electricity for data centers, defense and other customers using fuels ranging from natural gas and diesel to hydrogen and ammonia, aiming to cut emissions while keeping power reliable.

Operations: Hyliion currently generates US$5.8m in revenue from Auto Parts & Accessories in the United States.

Market Cap: US$758m

Hyliion Holdings sits at an early but interesting stage, with the KARNO Power Module targeting a sweet spot where data center operators, the U.S. military and regulators all want cleaner, more reliable on site power. The company has policy tailwinds like a 30% investment tax credit and a pipeline of letters of intent, plus recent defense related partnerships that frame a potential long term revenue stream. However, it is still loss making with less than a year of cash runway and no proven commercial sales base. For a penny stock focused on capital intensive hardware and additive manufacturing, that mix of funding risk and wide ranging analyst assumptions is a reason Hyliion may warrant closer, model driven scrutiny before any investment decision.

Hyliion’s early stage power story, with tax credits and defense interest already on the table, feels like it is missing one crucial piece: the analysis report for Hyliion Holdings that could reframe how you see its funding risk and upside

The three stocks in this article are just the starting point, and the full screener has surfaced 323 more Financially Fit Penny Stocks with equally compelling financial stories and potential catalysts inside the Financially Fit Penny Stocks screener. Use Simply Wall St to identify and analyze the specific balance sheet strength, cash flow profiles and business narratives that matter to you so you can focus on the highest conviction opportunities in this part of the market.

Take Control of Your Investment Journey

If Grab Holdings or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives For Your Curiosity?

Fresh stock ideas can move from quiet to full breakout fast, and the best entries rarely wait. Spot momentum early, before the crowd, and act now.

- Catch potential breakout trendsetters by scanning a curated pool of under radar compounders with the 19 high quality undiscovered gems while they are still flying below most investors’ screens.

- Ride structural demand for critical materials by tracking producers highlighted in the 8 top copper producer stocks while supply stories and project timelines still matter most to pricing.

- Target durable income streams by reviewing companies in the 9 dividend fortresses before yields drop and valuations fully reflect their balance sheet strength and payout records.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com