- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Cui Dongshu: The sales growth rate of automobile manufacturers was relatively stable in June, and the trend of new energy vehicles was not strong

The Zhitong Finance App learned that on July 11, Cui Dongshu published an article saying that due to the strong consumption policy last year, the 2026 policy contraction was obvious, and the entry-level consumer support policy declined sharply, causing passenger car retail sales to continue to grow negatively from January to June this year. In particular, there was a collapse in fuel passenger cars. However, due to increased exports, the manufacturer's sales growth rate was relatively stable in June. The trend of new energy vehicles was weak in June, the automobile export market continued to strengthen, manufacturers' inventories shrank slightly, and there was no phenomenon of industry inventory pressure.

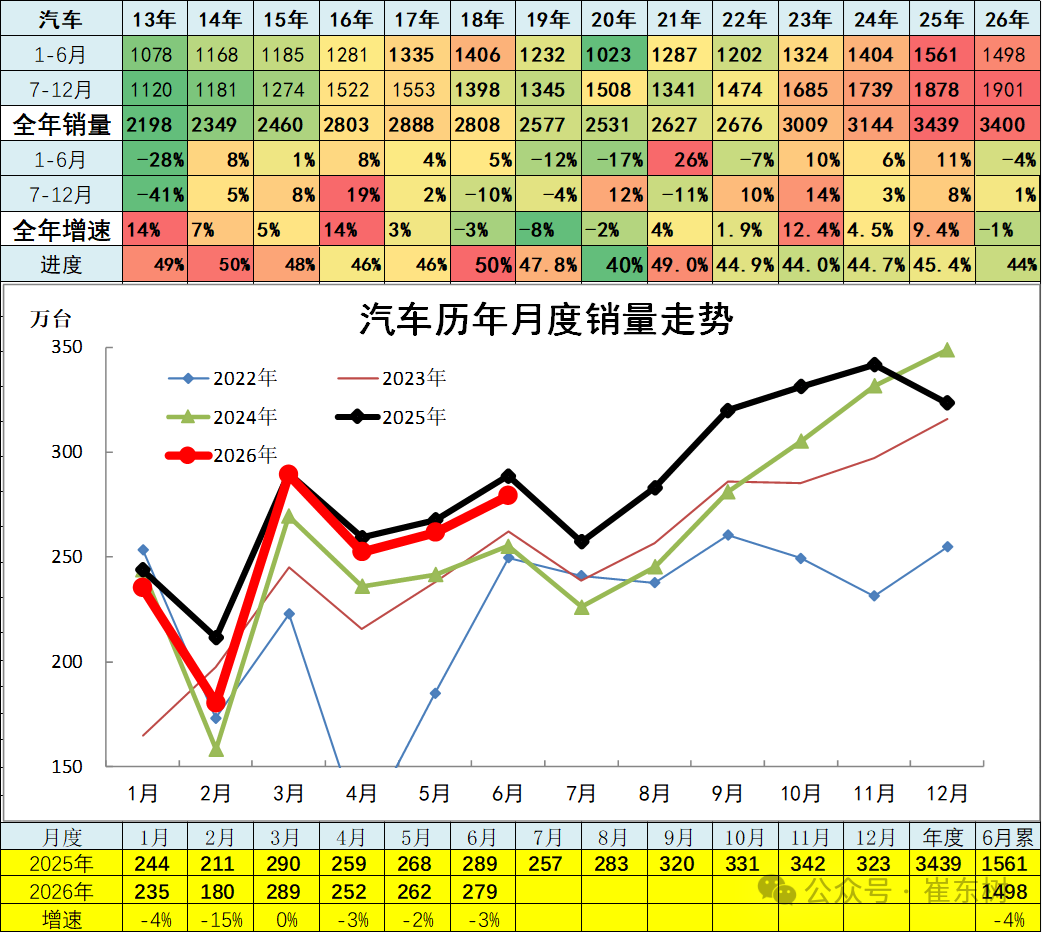

1. The automobile market is generally stable in 2026

Total car sales in June 2026 were 2.79 million units, down 3% year on year. From January to June 2026, the total sales volume of automobiles was 14.98 million units, a cumulative decrease of 4%. In 2026, the truck and bus market was strong, and the passenger car market performance was slightly weak. Coupled with strong exports and weak domestic markets, the overall sales trend of manufacturers was relatively stable in the end.

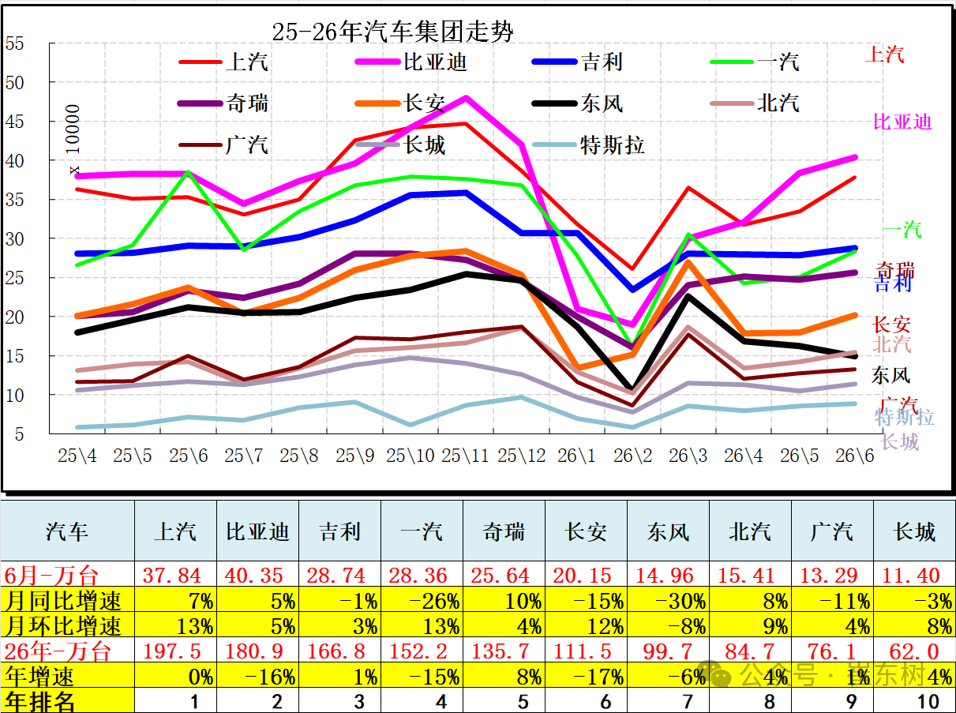

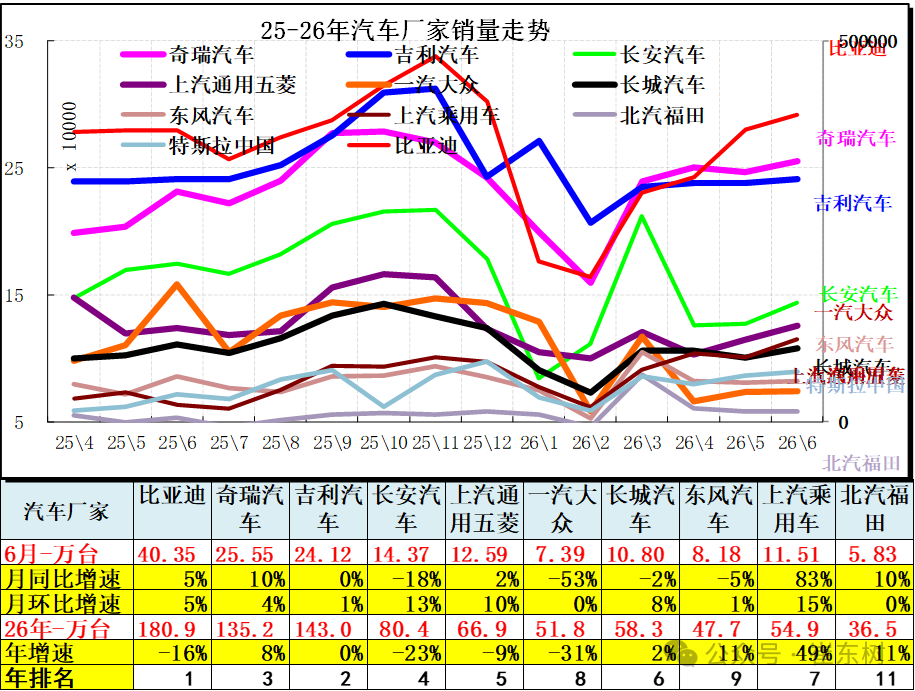

In 2026, the performance of the Automobile Group was drastically divided, and companies such as SAIC Motor (600104.SH) quickly recovered and achieved a comeback to number one. BYD (01211) is still maintaining a strong trend overall.

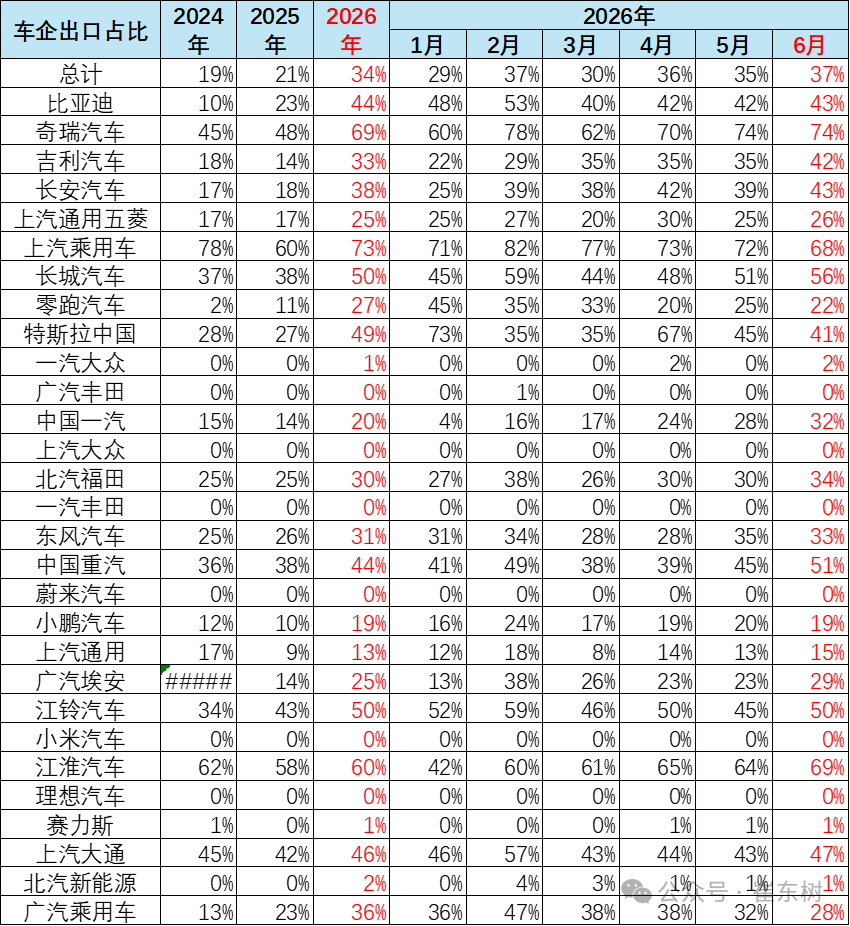

2. Export as a share of total sales

China's automobile exports have exploded in recent years, reaching 37% of total exports in June 2026, a significant increase from 21% in 2025, making exports an important component in supporting the growth of China's automobile scale.

3. The performance of major car groups is drastically divided

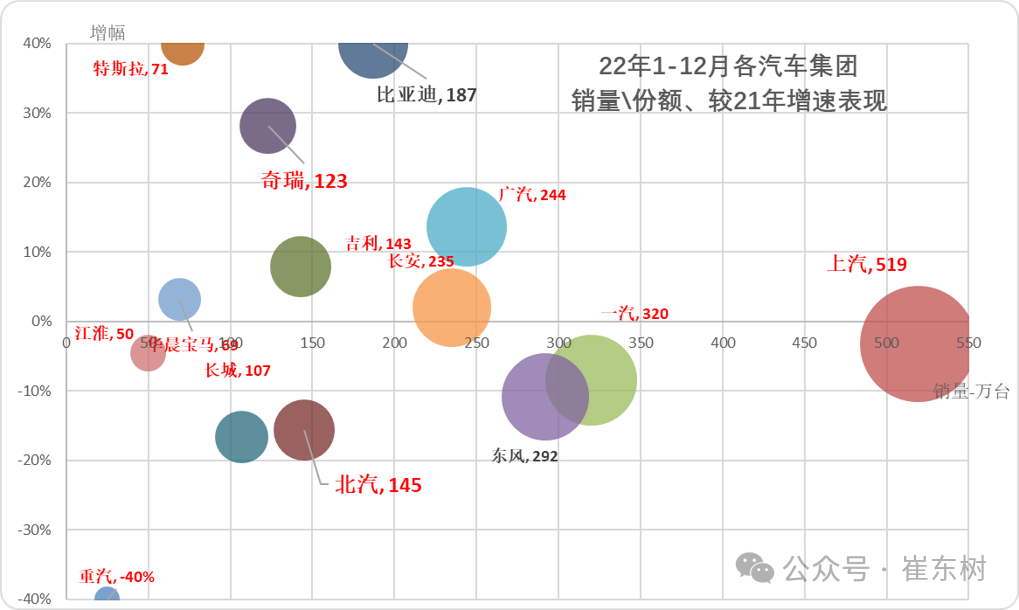

Compared with the 2021 chart above, some car companies performed strongly in 2022, and the growth rate of the industry was seriously divided. The epidemic in early 2022 put a lot of pressure on traditional car companies. In particular, the impact of new energy was compounded by the impact of the epidemic. The performance of large state-owned groups was divided, and GAC and Chery performed well. Among them, Chery's commercial vehicle and passenger car sectors performed well. The performance of various companies in the North, such as FAW, Great Wall, and BAIC, is under pressure.

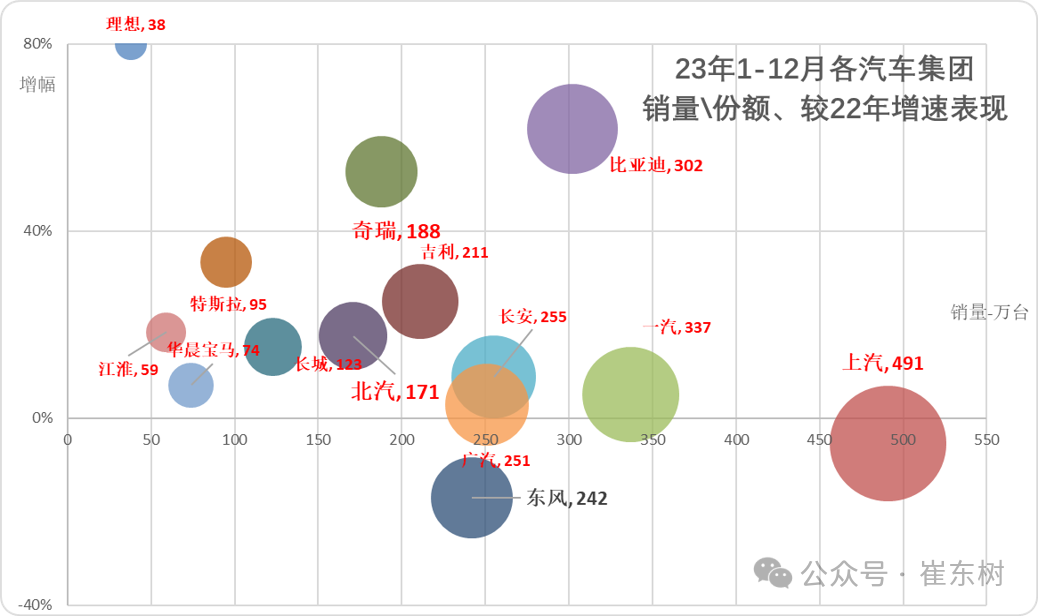

In early 2023, new energy sources drove the trend of the car market to diverge. The top three central enterprises are generally divided, and some state-owned enterprises are left behind. New energy companies such as BYD have performed very well; Chery and Tesla have performed relatively well this year. The performance of second-tier car companies is divided. Due to the continuous loss pressure of new and old kinetic energy conversion and new energy vehicles, the differentiation of own-brand SMEs is seriously sluggish.

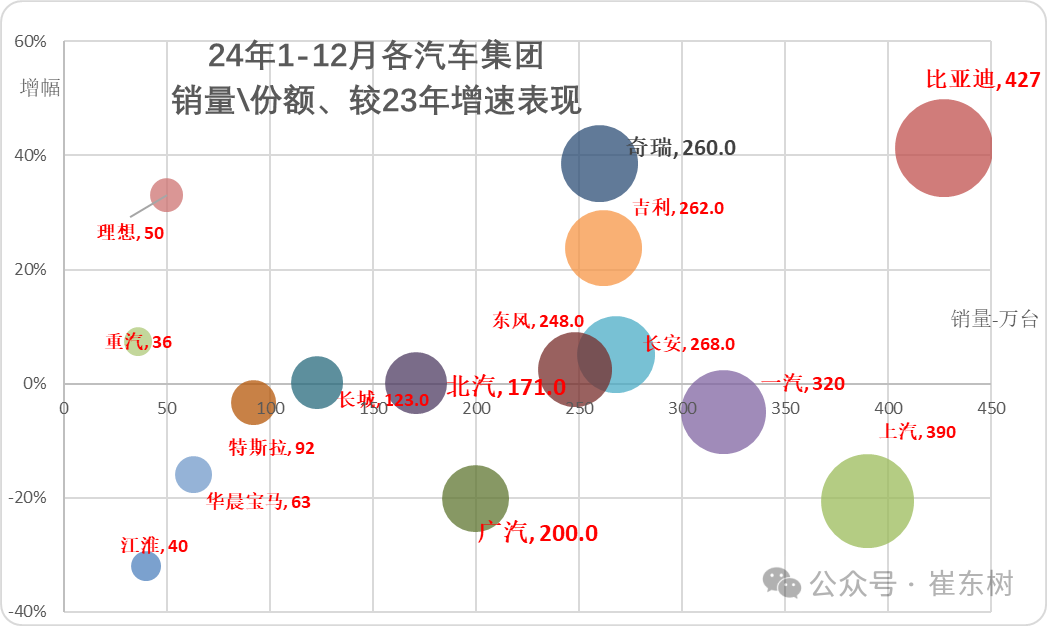

The Auto Group's lineup pattern changed completely in 2024, and the price reduction of new BYD products increased. Due to the high demand for passenger car sales and overseas contributions, Chery, Geely, and Dongfeng performed well, and SAIC Motor is still in a sharp decline. The growth rates of new energy vehicles at BYD and Tesla are diverging.

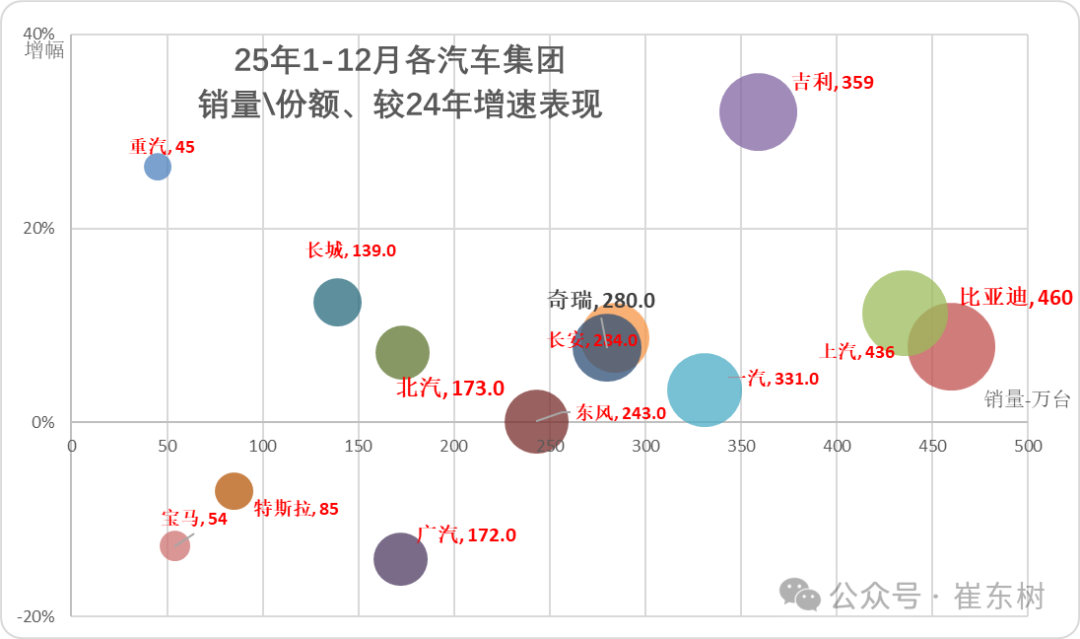

The pattern of manufacturers in the automobile market has changed dramatically, and the industry is showing sharp divisions in growth. Private enterprises starting in 2025 replaced state-owned enterprises as the main players in the industry, and the growth rates of Geely, BYD, Chery, and Great Wall remained at a high level.

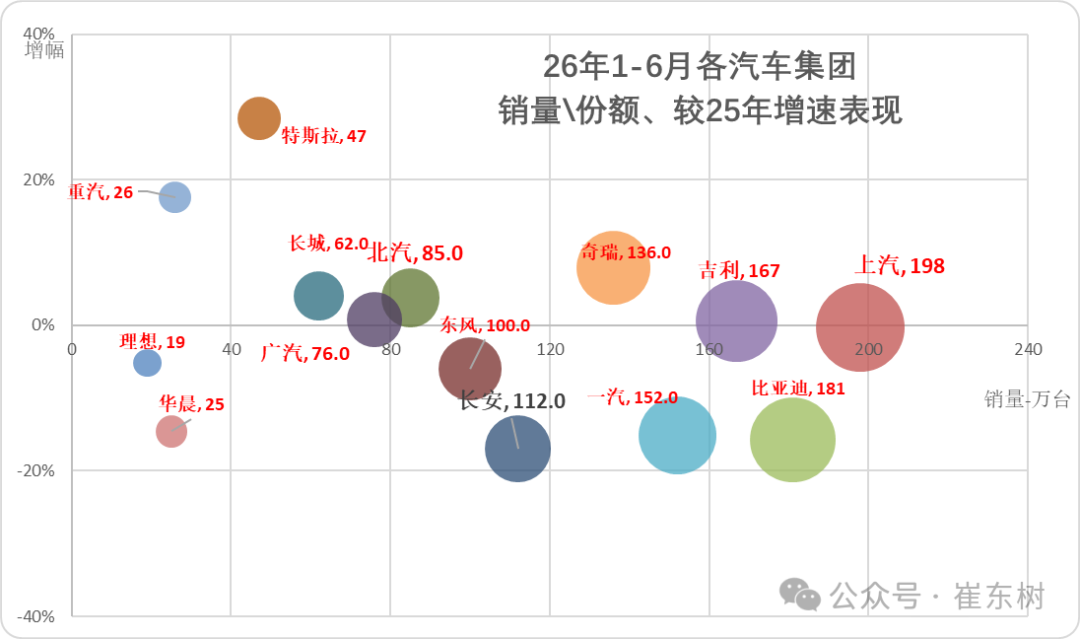

Leading sales in 2026 is the focus of efforts of companies in various countries. Despite the severe downturn in the market, SAIC Motor, Geely, Chery, and BAIC performed well in January-June of this year, and their growth rate improved. Great Wall, Tesla, etc. performed well overall.

In 2026, the pattern of automobile manufacturers was relatively stable, and their autonomous status increased dramatically. The overall sales volume of manufacturers was good in June, but sluggish retail sales in the market dragged down the performance of passenger car manufacturers. Some manufacturers, such as BYD, showed a strong month-on-month trend compared to May; SAIC passenger cars and the like strengthened year on year; while some manufacturers such as BYD sold very well in June, Changan (000625.SZ) and others are still making strong year-on-year adjustments.

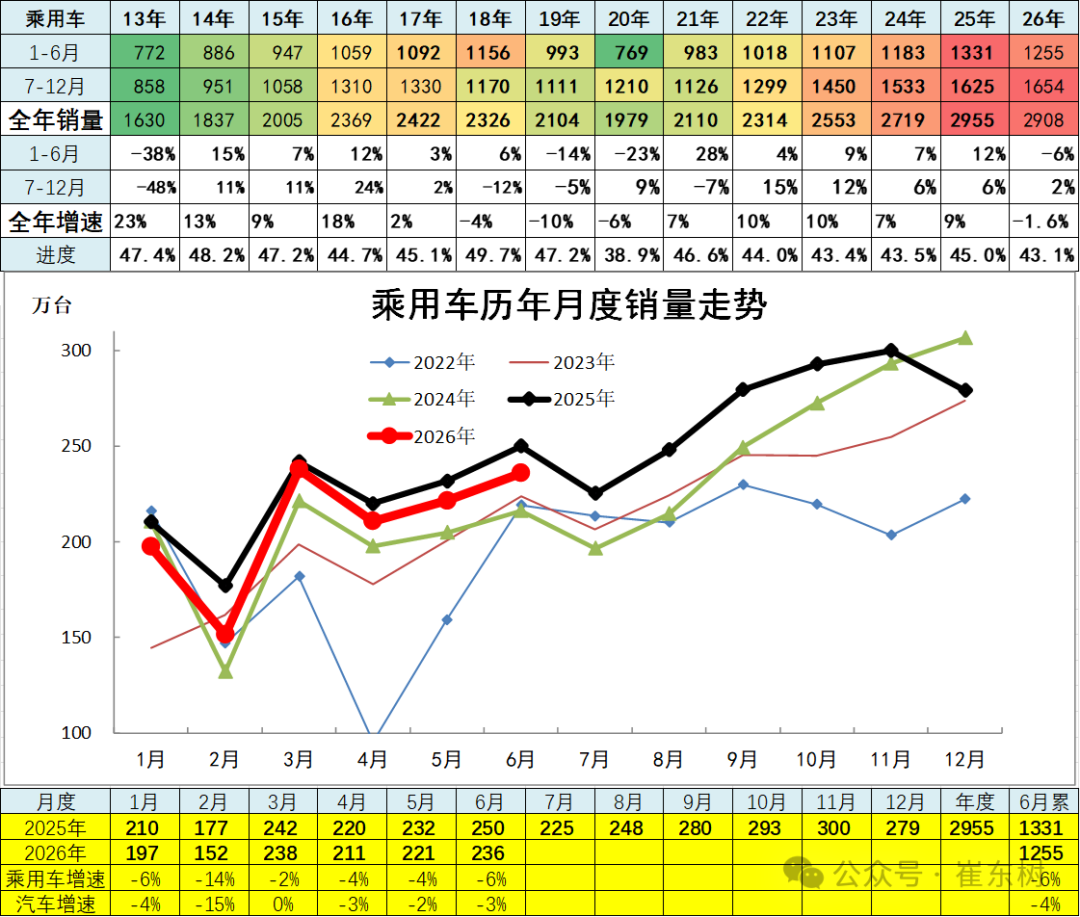

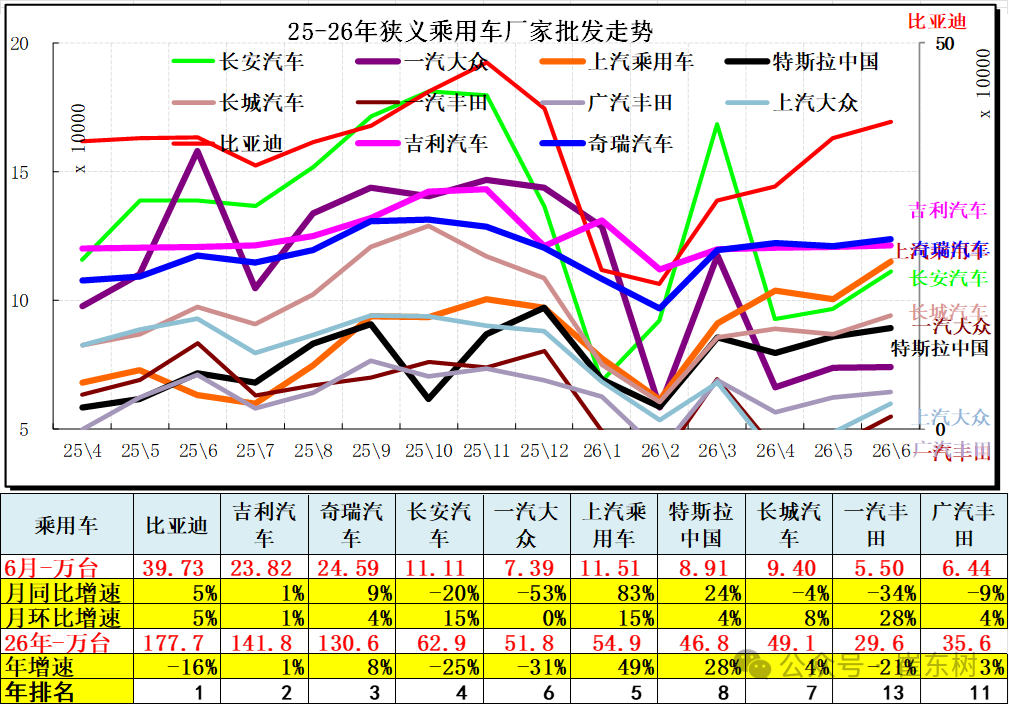

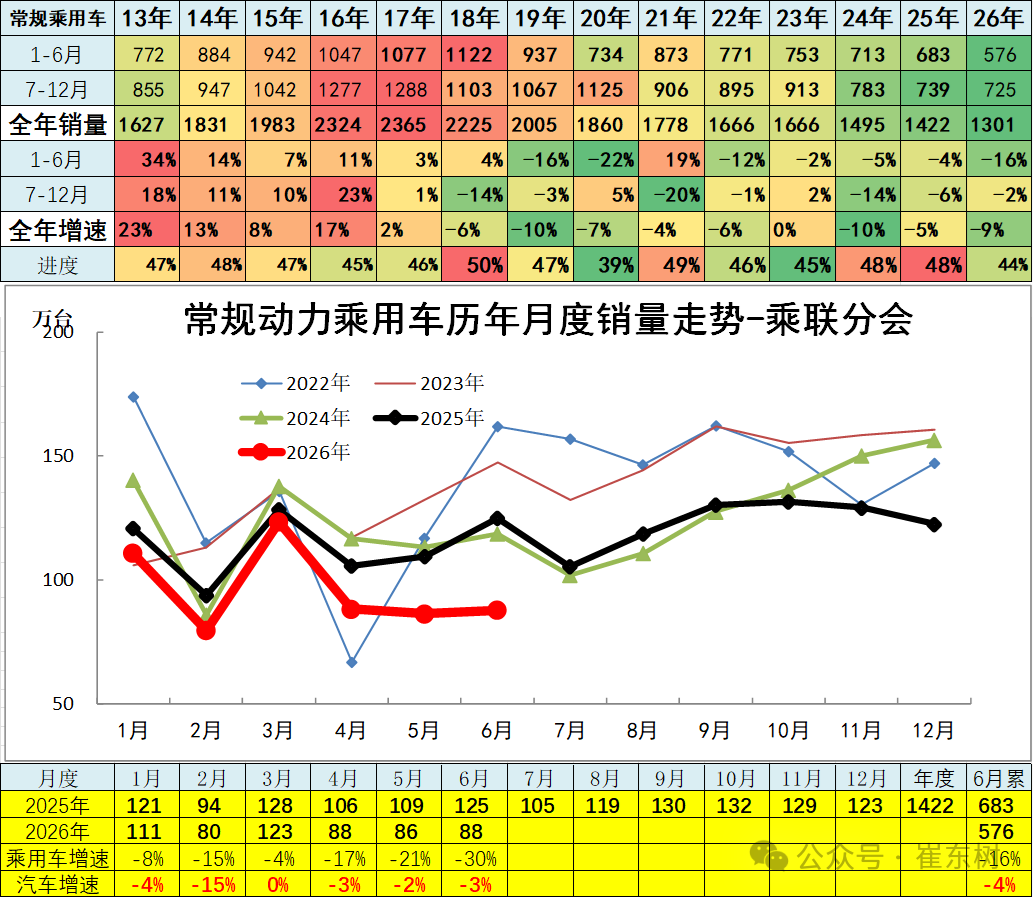

4. Production and sales trends of passenger car companies in the narrow sense

In June 2026, the total sales volume of passenger cars in the narrow sense was 2.36 million units, down 6% year on year; from January to June 2026, the total sales volume of passenger cars in the narrow sense was 12.55 million units, down 6% year on year. In recent years, technological innovation in new energy vehicles and the competitiveness of new products have continued to grow, and the launch of new fuel vehicles has been weak. New energy vehicles at the beginning of 2026 are in an adjustment period. Dealers' confidence is insufficient, and high oil prices are holding down the growth rate.

In 2026, passenger car autonomous vehicle companies will take the overall lead. The main car companies were generally weak in June, and their autonomy was strong. Joint venture car companies showed a weak trend in June due to high oil prices. BYD led the way, Chery ranked 2nd, and Geely held the top 3 in June, and the scale of the top 3 is getting closer. Joint ventures such as FAW-Volkswagen and SAIC-Volkswagen are underperforming fans.

The main passenger car manufacturers rapidly divided. Export-oriented companies and NEV manufacturers showed strong performance. Joint venture performance differentiation was particularly obvious, and Toyota was stronger.

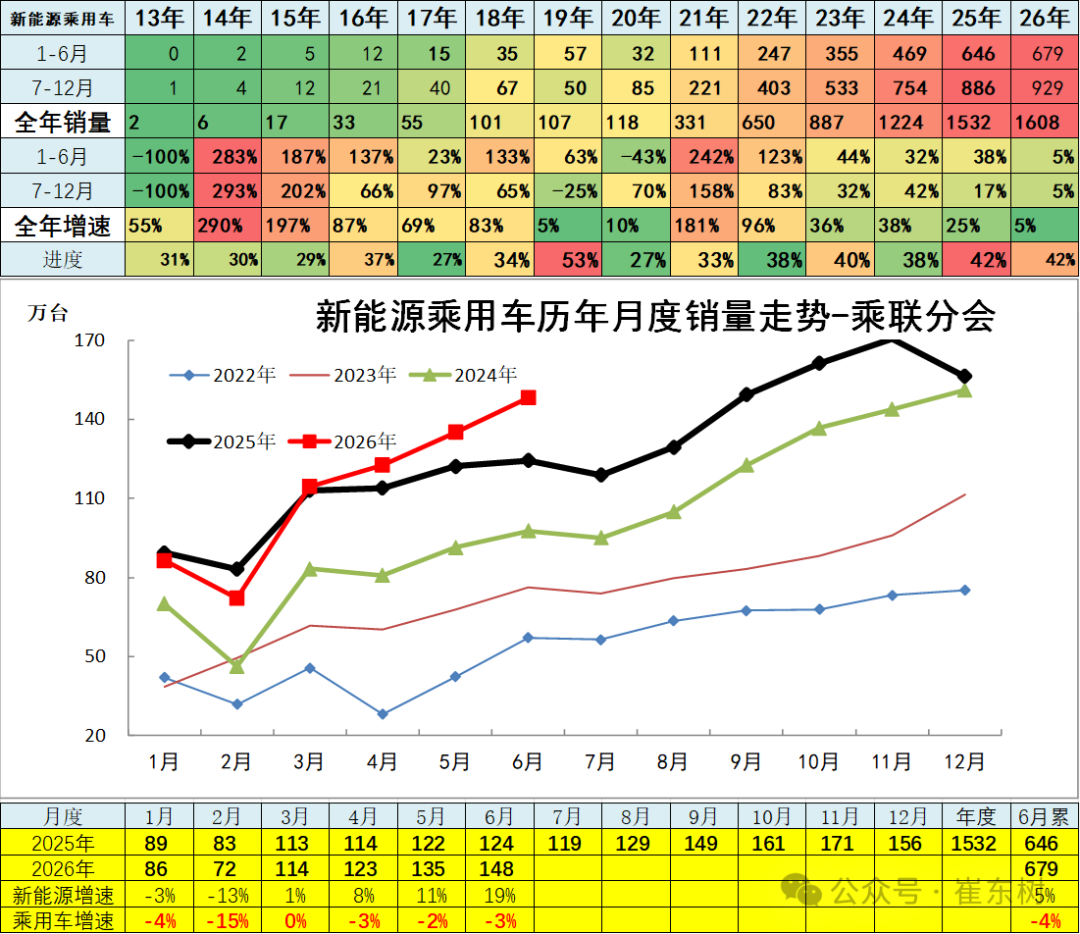

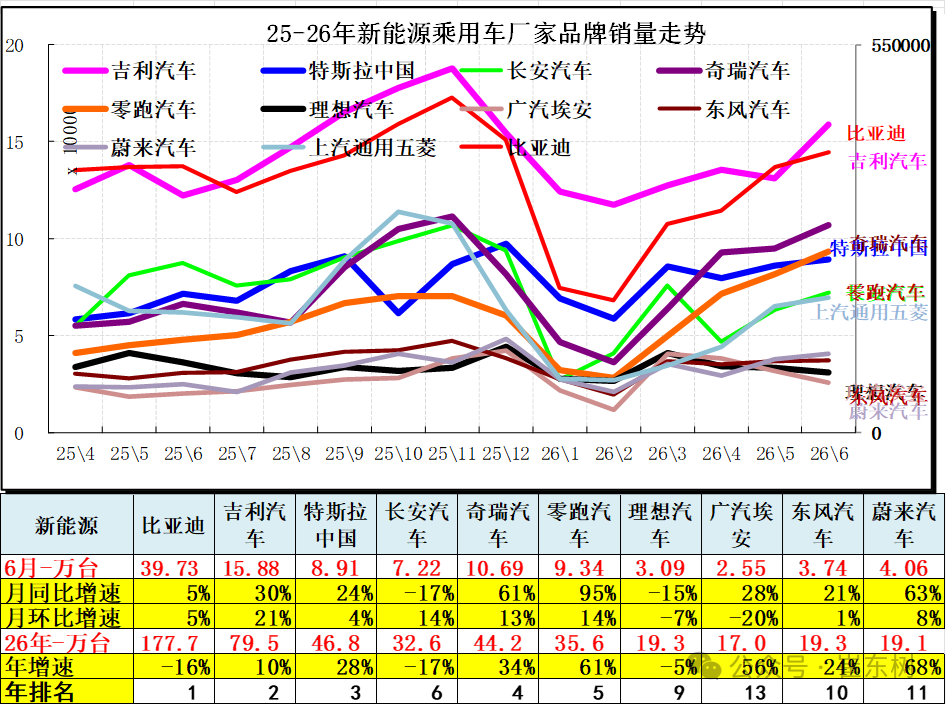

5. Production and sales trends of new energy passenger vehicle companies

In June 2026, NEV manufacturers sold a total of 1.48 million units, up 19% year on year; from January to June 2026, NEV manufacturers sold a total of 6.79 million units, up 5% year on year. At the beginning of 2026, scrapping and renewal subsidies were under high pressure, oil prices skyrocketed, consumption was sluggish, and demand for new energy vehicles was weak. The domestic trend of new energy in 2026 faced strong pressure from low demand.

In 2026, BYD remained number one, but mixed growth pressure was strong. New energy sources such as Chery and Zero Run are growing strongly.

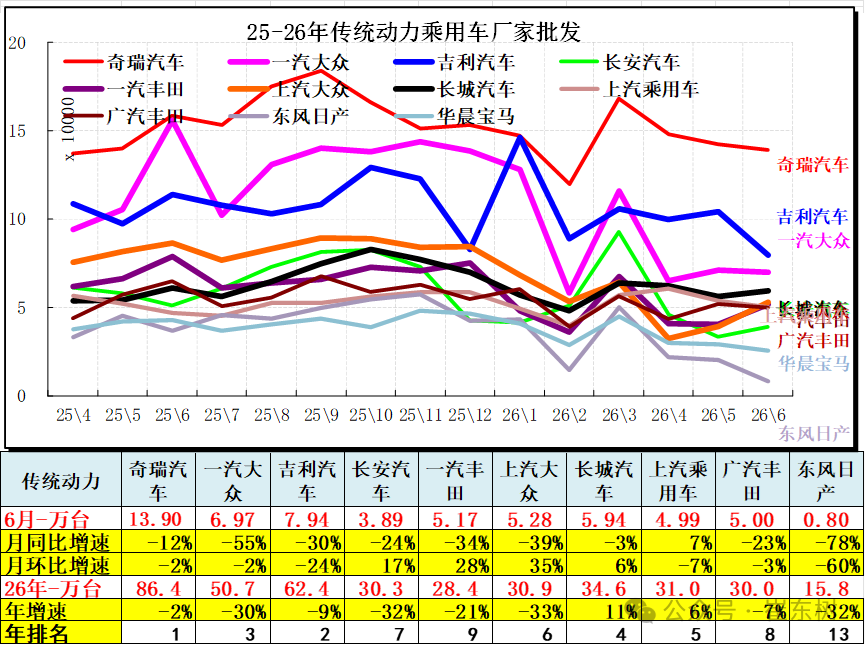

6. Production and sales trends of traditional power passenger car companies

In 2025, sales of passenger cars in the narrow sense of fuel were 14.22 million units, a year-on-year decrease of 5%. From January to June 2026, 5.76 million units fell 16%. As oil prices rise, the market trend is still weak in 2026.

Due to export support, the overall performance of fuel vehicles was divided in 2026, and autonomous performance was strong, and the main joint venture car companies rapidly weakened in the short term.

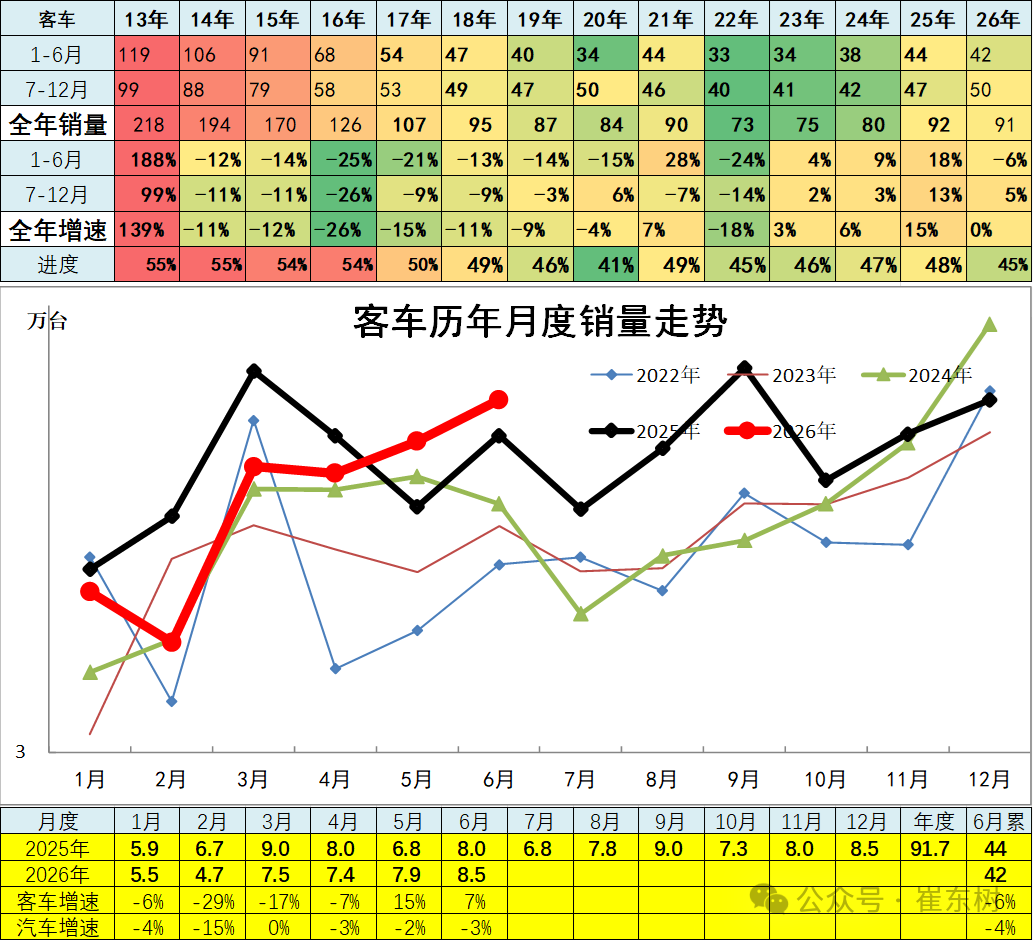

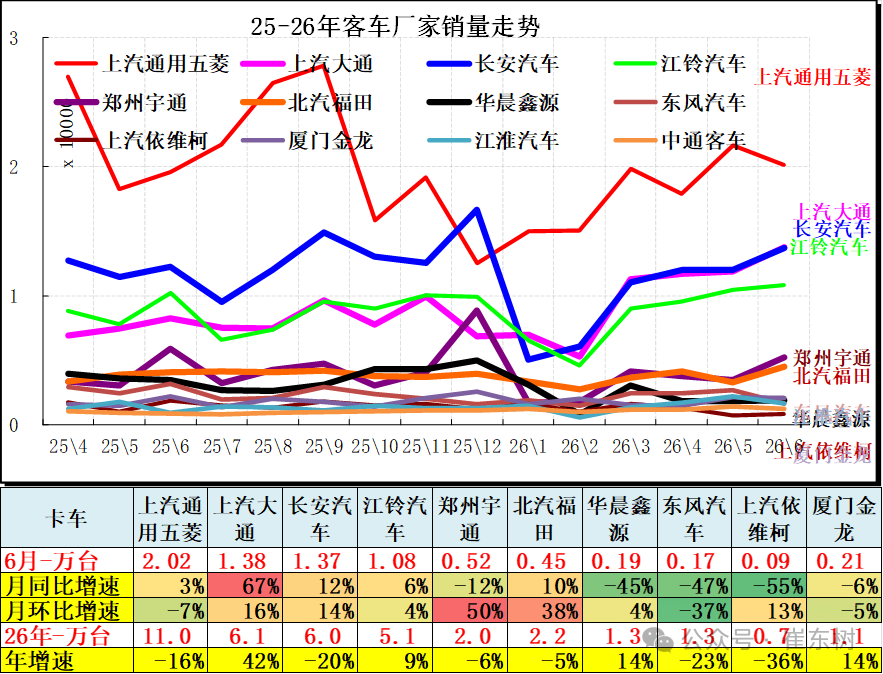

7. Production and marketing classification trends of bus companies

Total bus sales for the full year of 2025 were 920,000 units, with a cumulative growth rate of 15%; total bus sales from January to June 2026 were 420,000 units, down 6% year on year, and the driving effect of exports and new energy logistics vehicles was average.

After sprinting at the end of 2025, the bus trend gradually strengthened in 2026. SAIC-GM-Wuling performed very well. Leading manufacturers such as SAIC Maxus have generally had strong sales in recent months. Market demand for logistics light buses and WeChat has fluctuated greatly, and exports have contributed greatly. Commercial vehicle trends for Jiangling Motors and SAIC Chase were good in 2026. Logistics vehicle companies such as Zhengzhou Yutong, Beiqi Foton, and SAIC Chase rebounded significantly in June.

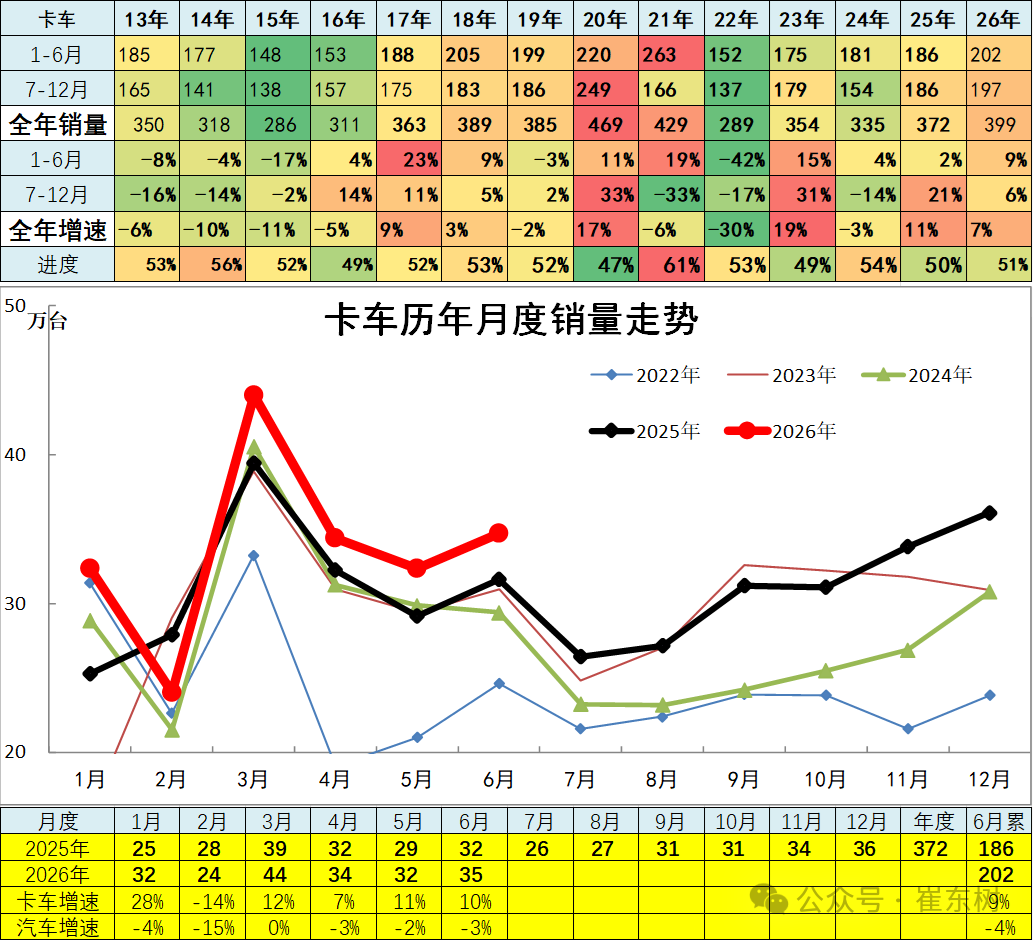

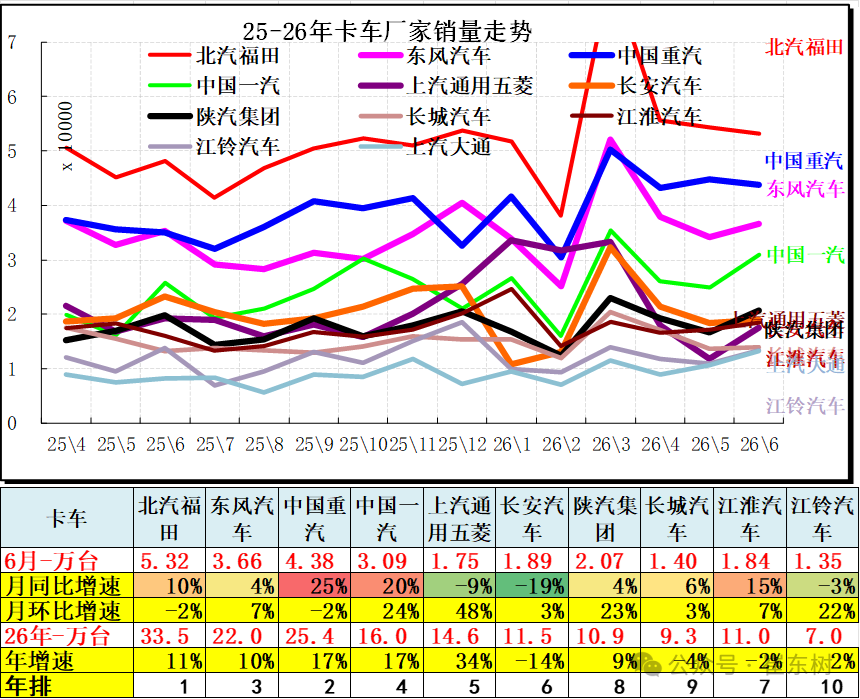

8. Production and marketing classification trends of truck companies

In 2025, truck sales were 3.72 million units, with a cumulative growth rate of 11%; from January to June 2026, truck sales were 2.02 million units, up 9% year on year, forming a trend of differentiation between consumption and production, a sharp decline in consumption and strong production growth.

Major truck manufacturers were clearly divided in 2026, with leading truck manufacturers showing strong performance. Vehicle companies such as BAIC Foton, China FAW, Sinotruk, and JAC have surged compared to June last year.

The effects of commercial vehicle subsidies are outstanding. Heavy trucks have skyrocketed in 2026, pure electric heavy trucks have performed very well, FAW, Shaanxi Automobile, and Sinotruk are growing strongly, and the industry pattern is relatively stable.