- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Does Illinois Medicaid Renewal Solidify Centene’s Core Government Programs Franchise Narrative (CNC)?

- Centene’s Illinois subsidiary, Meridian Health Plan of Illinois, was previously awarded a four‑year contract extension to continue serving in the HealthChoice Illinois Medicaid managed care program from January 1, 2027, reinforcing its role among six managed care organizations supporting approximately 2.4 million Medicaid‑eligible residents statewide.

- This renewal underscores Illinois’ confidence in Meridian’s coordinated-care model and focus on social determinants of health, which are central to Centene’s government‑programs business.

- We’ll now examine how this major Illinois Medicaid contract renewal could influence Centene’s broader investment narrative and outlook.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Centene Investment Narrative Recap

To own Centene, you need to be comfortable with a company built around large, long term government health contracts and disciplined cost control. The Illinois Medicaid renewal strengthens that foundation but does not remove near term pressure points such as medical cost volatility and uncertainty around Medicaid rate adequacy, which remain key risks for margin recovery in the coming years.

The most relevant recent announcement alongside the Illinois award is Centene’s Q1 2026 update, where management raised full year 2026 GAAP diluted EPS guidance to more than US$2.37 on projected revenue of US$187.5 billion to US$191.5 billion. That focus on execution and margin repair frames how investors might think about the financial importance of retaining sizable Medicaid contracts like HealthChoice Illinois.

Yet behind the contract win, investors should be aware that...

Read the full narrative on Centene (it's free!)

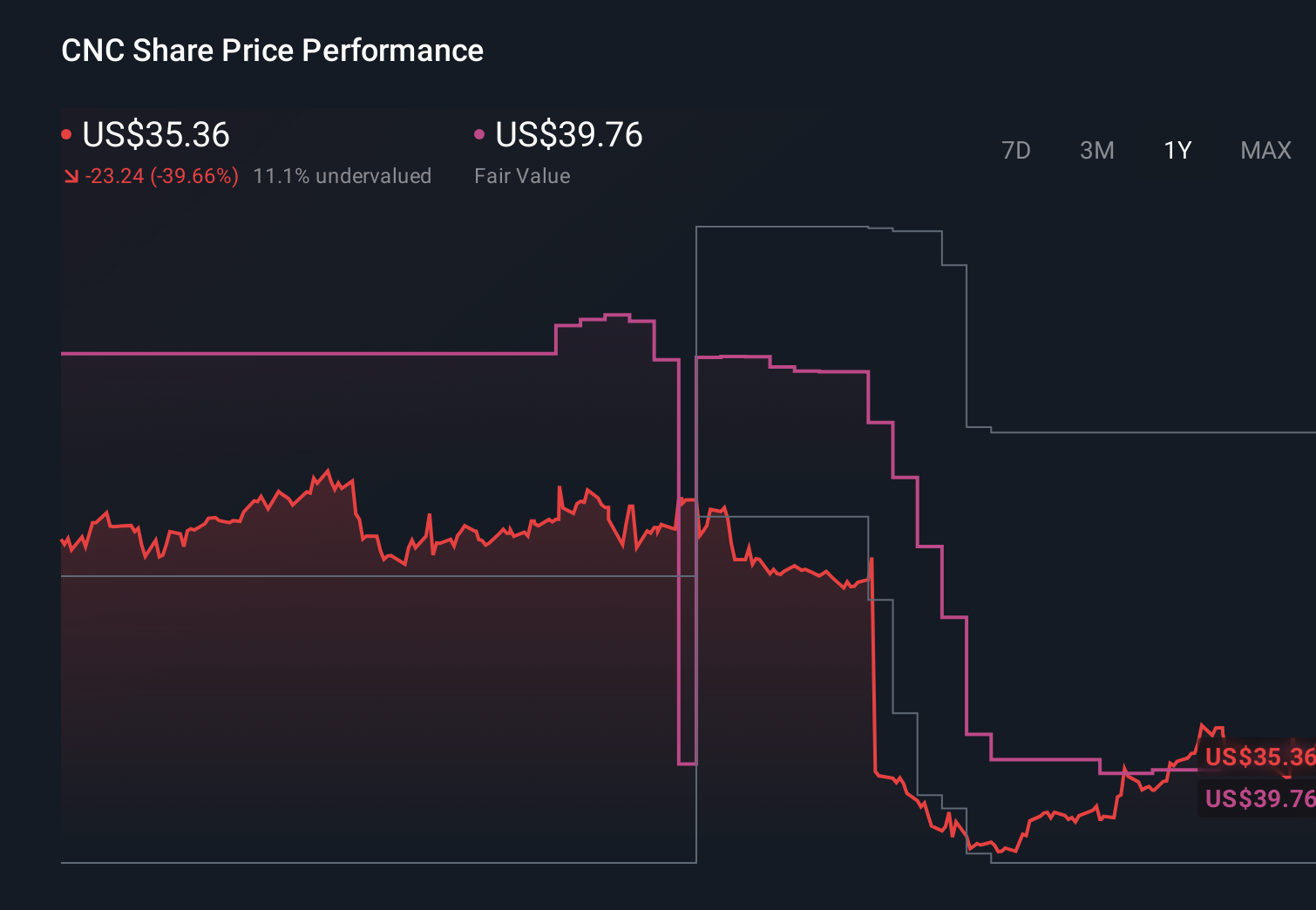

Centene's narrative projects $200.3 billion revenue and $2.7 billion earnings by 2029. This requires 4.0% yearly revenue growth and about a $9.1 billion earnings increase from -$6.4 billion today.

Uncover how Centene's forecasts yield a $61.83 fair value, a 8% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming Centene could reach about US$209.5 billion of revenue and US$3.7 billion of earnings by 2029, so this Illinois renewal may either reinforce that faster margin recovery story or highlight how dependent it is on continued contract wins and policy stability.

Explore 10 other fair value estimates on Centene - why the stock might be worth over 3x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Centene research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Centene research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Centene's overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com