- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

European Real Estate Stocks to Watch as Lower Inflation Shifts Rate Cut Expectations

Cooling French inflation, confirmed at 2.0% year on year in June on an EU harmonised basis, is reshaping expectations around European Central Bank policy and interest rate paths. For European real estate stocks, small shifts in borrowing costs and consumer confidence can matter as much as rental income and occupancy. This article looks at how that inflation backdrop could affect sentiment toward larger listed property companies, and what that might mean for investors weighing exposure to the sector. Ahead, you will find three stocks from our European Real Estate Stocks screener that appear positively exposed to this news.

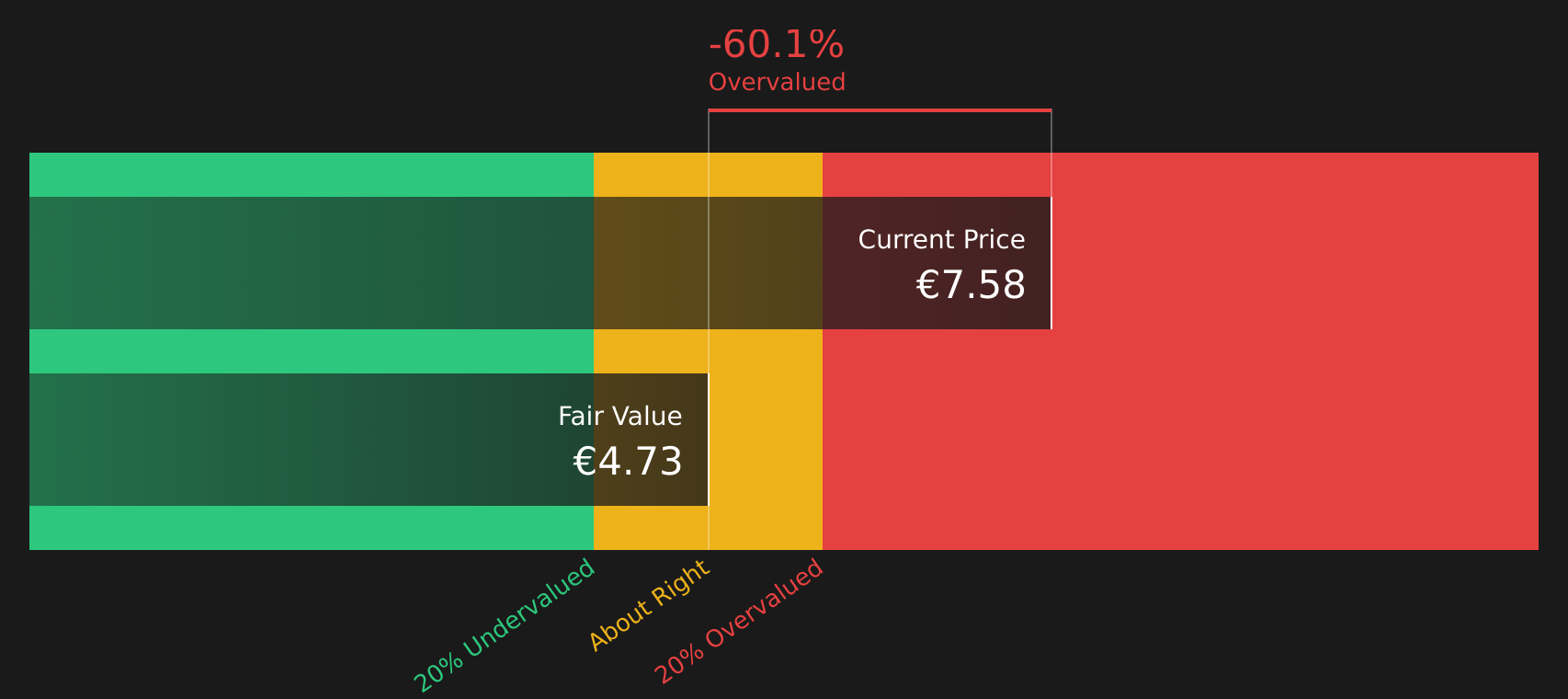

Nexity (ENXTPA:NXI)

Overview: Nexity is a French real estate group that plans, develops, and manages a wide range of properties, from new housing and office buildings to logistics platforms, shops, hotels, student residences, and coworking spaces for individuals, businesses, and local authorities.

Operations: Nexity generates most of its revenue from Promotion activities at about €2.4b, with Services contributing roughly €422.7m and Other Activities around €5.1m, primarily in France where about €2.7b of revenue is recorded versus €72.5m abroad.

Market Cap: €421.9m

Cooling French inflation and the prospect of less pressure on ECB rates could matter for Nexity, which relies on residential development and higher risk external borrowing at a time when the real estate cycle is described by management as somber and margins are held back by older crisis era projects. The stock screens as lowly valued on sales compared with peers, while analysts still see a path to a return to profit over the next few years and Nexity is pursuing a joint venture with Groupe BPCE that could widen its access to first time buyers and investors. For investors, the tension between funding risk, subdued demand, and potential upside from a large housing pipeline is where the story gets interesting.

Nexity’s low sales multiple and somber cycle set up a classic mismatch between sentiment and potential, but the real story sits inside the DCF valuation analysis for Nexity, where funding risk and housing demand intersect unexpectedly.

MERLIN Properties SOCIMI (BME:MRL)

Overview: MERLIN Properties SOCIMI is a large listed Spanish real estate and infrastructure company focused on owning, developing, and managing income producing commercial assets across the Iberian Peninsula, including offices, shopping centers, logistics facilities, and data centers.

Operations: MERLIN Properties SOCIMI generates most of its revenue from office buildings at about €292.1m, followed by shopping centers at roughly €129.4m, logistics at €83.5m, data centers at €45.4m, and other activities at under €1m, plus a €29.6m segment adjustment.

Market Cap: €9.3b

MERLIN Properties SOCIMI sits at the crossroads of several themes in European real estate: demand for high quality offices, the growth of logistics tied to e commerce, and the build out of data centers as digital infrastructure. Cooling French inflation and reduced pressure on euro area rates matter for a company that relies on external debt and funds capital intensive projects, while its P/E sits below many peers. At the same time, office concentration, one off gains and an uneven dividend record introduce uncertainty. For investors, the interest lies in how MERLIN balances rental income, new data center ambitions, and a leveraged capital structure at a time when funding costs and property values are under close scrutiny.

MERLIN’s mix of offices, logistics, and data centers is only half the story. The tension between its P/E, debt load, and growth projects shows up clearly inside the 4 key rewards and 2 important warning signs

Aedas Homes (BME:AEDAS)

Overview: Aedas Homes is a Spanish residential developer that builds multi and single family homes, including turnkey build to rent projects, while also offering real estate, interior design, and related services to both individual buyers and institutional investors.

Operations: Aedas Homes generates the bulk of its €868.8m revenue from Development activities at about €847.2m, with Asset Management contributing roughly €21.7m, all in Spain.

Market Cap: €946.1m

Aedas Homes sits at the center of Spain’s new housing market, with a sizeable order book, a landbank geared to several years of development, and growing fee based services in build to rent and asset management. Cooling inflation in France, which shapes expectations for euro area rates, is important for a business funded entirely by external borrowing and selling higher ticket homes, because cheaper finance can support both project funding and buyer affordability. Yet profit margins have compressed, net income dropped to €60.9m, and returns on equity are modest, so investors need to weigh forecast earnings growth against funding risk, regional concentration, and recent earnings volatility to see what the current P/E and analyst targets may be missing.

Aedas Homes’ compressed margins and €847.2m development engine make the earnings story feel incomplete, and the missing piece sits inside the analyst forecasts for Aedas Homes where one key assumption could change the narrative.

The three stocks covered here are just a starting point, and the full European Real Estate Stocks screener surfaced 11 more European real estate companies with equally compelling, but very different, stories tied to funding costs, rental income profiles, and housing affordability. Use Simply Wall St to identify and analyze the specific catalysts and narratives that matter most to you, so you can focus on the opportunities that best fit your own conviction.

Take Control of Your Investment Journey

If Nexity or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Real Estate?

Some stocks are building quiet momentum while most investors are still focused elsewhere. Before potential entry points are fully reflected in prices, scan these fresh ideas and consider them early.

- Target steady income and reduce surprises by zeroing in on companies from the 471 dividend fortresses that have been filtered for durability, not just headline yields.

- Spot companies quietly building strong positions with the 107 top founder-led companies so you see where long term operators still have real skin in the game.

- Stay informed about major infrastructure trends by tracking potential beneficiaries inside the 34 power grid technology and infrastructure stocks while the theme is still under the radar for now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com