- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is AllianceBernstein Holding (AB) Undervalued As Margin Plans And Private Markets Growth Build?

AllianceBernstein Holding (AB) is drawing fresh attention as management pursues office relocation and other margin accretion efforts aimed at stronger net margins by 2025, while expanding its private markets platform.

See our latest analysis for AllianceBernstein Holding.

Against this backdrop, AllianceBernstein Holding’s recent share price moves have been relatively muted, with a 7 day share price return of 2.34% but a year to date share price return that is down 3.83%, while 3 year total shareholder return of 43.67% points to stronger momentum over a longer horizon.

If this mix of short term repositioning and longer term wealth creation interests you, it could be worth widening your search with 18 top founder-led companies

So is AllianceBernstein Holding’s recent share price lift a signal that its margin and private markets plans are gaining traction in investors’ models, or just a short term sentiment swing that leaves the current valuation doing most of the work?

Most Popular Narrative: 5.1% Undervalued

On the most followed narrative, AllianceBernstein Holding’s fair value of $39.14 sits a little above the last close at $37.16, which frames the current upside as modest rather than dramatic.

AllianceBernstein is expanding into high-growth markets such as Asia, U.S. high net worth, and global insurance, supported by its differentiated distribution platform, which is expected to drive revenue growth. The company is enhancing its margin profile by relocating its office and implementing margin accretion initiatives, which are projected to improve net margins as they move into 2025.

Want to see what sits behind that fair value gap for AllianceBernstein Holding? The narrative leans heavily on rapid top line expansion, a changing mix of high fee strategies, and a tighter margin structure. The key is how those moving parts are modeled together over several years, not a single quarter snapshot.

Result: Fair Value of $39.14 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, even for AllianceBernstein Holding, lower interest rates squeezing private credit spreads or sustained fee pressure in fixed income could quickly challenge this undervaluation story.

Find out about the key risks to this AllianceBernstein Holding narrative.

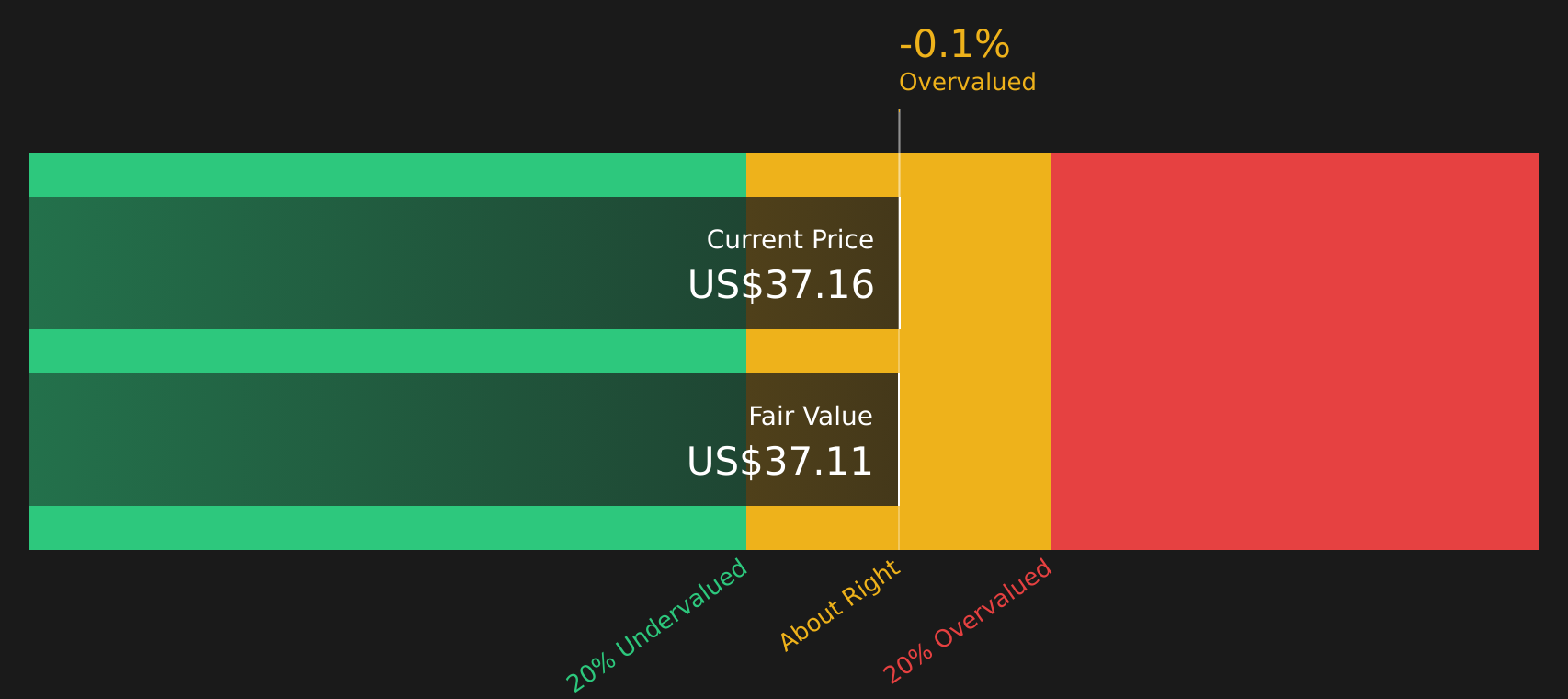

Another View: Fair Value Looks Tighter On Cash Flows

While the most followed AllianceBernstein Holding narrative points to a 5.1% upside to fair value, our DCF model presents a much tighter picture. The current $37.16 price sits slightly above an estimated future cash flow value of $37.11, which tilts this view toward overvalued rather than undervalued.

This small gap highlights how sensitive AllianceBernstein Holding’s story is to long term cash flow assumptions and discount rates. When the signals are this close together, the question becomes which lens you place more weight on.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out AllianceBernstein Holding for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on valuation and sentiment around AllianceBernstein Holding, it may be helpful to review the full data set promptly and shape your own view using the 2 key rewards and 4 important warning signs.

Looking for more investment ideas beyond AllianceBernstein Holding?

If AllianceBernstein Holding has your attention, do not stop here. Broaden your watchlist with fresh ideas that match different goals, risk levels, and income needs.

- Target potential mispricing by scanning companies that combine quality fundamentals with room for re rating using the 44 high quality undervalued stocks.

- Strengthen your income stream by focusing on companies that aim to keep paying investors with the support of the 9 dividend fortresses.

- Protect your downside by concentrating on resilient businesses with sturdier finances through the 76 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com