- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

PSP Swiss Property (SWX:PSPN) Could Be 3% Undervalued As Special Meeting Nears

PSP Swiss Property (SWX:PSPN) has called a special investor meeting for 27 June 2026 to discuss a corporate transaction and revised EBITDA guidance, a combination that often signals meaningful implications for future cash flows.

See our latest analysis for PSP Swiss Property.

At a share price of CHF143.8, PSP Swiss Property has seen its 90 day share price return fall 9.04%, while the 1 year total shareholder return of 5.74% sits against a much stronger 3 year total shareholder return of 54.35%. This hints that long term momentum has been firmer than the more recent trend around the upcoming transaction and EBITDA update.

If this special meeting has you rethinking where you allocate capital, it could be a good moment to widen your search with 108 top founder-led companies

Bulls may view PSP Swiss Property’s long term returns and upcoming transaction as a chance to support a resilient landlord, while bears focus on softer EBITDA guidance and recent share weakness. So what do the valuation numbers actually point to next?

Most Popular Narrative: 3% Undervalued

The most followed narrative on PSP Swiss Property puts fair value at CHF148.25, slightly above the last close at CHF143.8, so the special meeting lands against a backdrop of only modest implied upside.

The company's high concentration in office assets in Zurich and Geneva leaves it exposed to a potential medium-term oversupply risk, particularly as large tenants (e.g., UBS) are expected to bring more office space to the market in 2026-2027. This could lead to temporary vacancy spikes, putting pressure on future rental income and net earnings.

PSP's portfolio is concentrated in prime locations (Zurich, Geneva CBD) where demand remains robust, supported by secular trends like urbanization and restricted land supply which underpin high occupancy, rental growth, and recurring valuation uplifts, benefitting asset values and shareholder returns.

Want to see what sits behind that tension between prime-city demand and future vacancy risk? The narrative leans on revenue growth, margin compression, and a richer profit multiple. Curious which assumptions really carry the CHF148.25 fair value story?

Result: Fair Value of CHF148.25 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, for PSP Swiss Property this narrative could still be upset if office oversupply in Zurich and Geneva materializes faster than expected or if sustainability capex meaningfully squeezes margins.

Find out about the key risks to this PSP Swiss Property narrative.

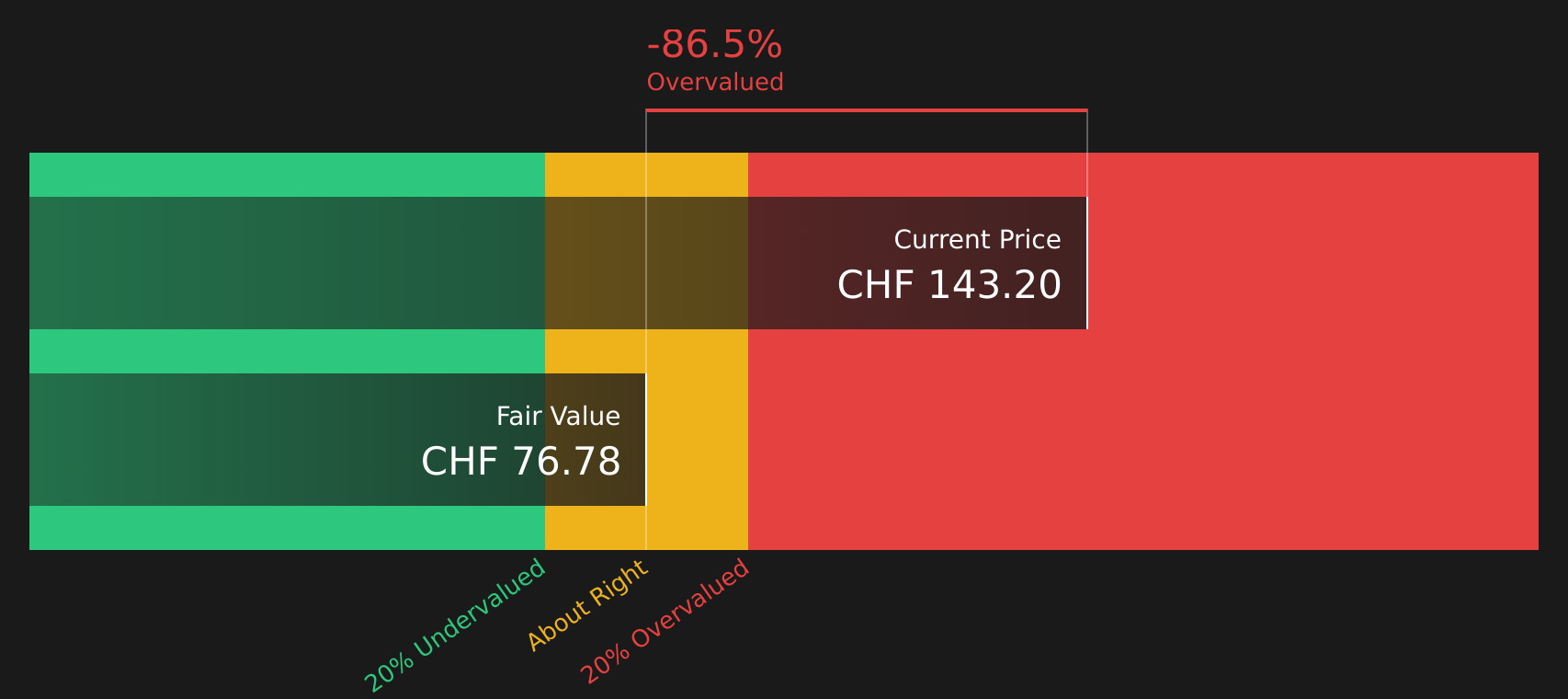

Another View: PSP Swiss Property Through a Cash Flow Lens

The earlier discussion used earnings multiples to argue PSP Swiss Property looks about 3% undervalued at CHF148.25 fair value versus the CHF143.8 share price. Our DCF model presents a very different picture, with an estimate of future cash flow value at CHF77.67, which makes the current price look expensive instead.

For investors, that gap is not just academic. If earnings based models and cash flow based models disagree this sharply, it raises a simple question: which set of assumptions are you more comfortable tying your capital to over the long run?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out PSP Swiss Property for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 213 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around PSP Swiss Property leave you unsure, treat that as a cue to move quickly, review the data carefully, and build your own stance using 2 key rewards and 3 important warning signs

Looking for more investment ideas beyond PSP Swiss Property?

Do not stop with one stock. Broaden your watchlist now with focused ideas that could suit different goals, risk levels, and income needs.

- Target potential mispricing by scanning 213 high quality undervalued stocks that combine quality fundamentals with room for market expectations to catch up.

- Strengthen your income stream by reviewing 471 dividend fortresses built around higher yields that still keep an eye on stability.

- Sleep easier at night by focusing on 292 resilient stocks with low risk scores designed for investors who want resilience front and center.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com