- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Stocks Priced Below Estimated Value For Savvy Investors In July 2026

Over the last 7 days, the United States market has remained flat, though it has seen a 20% rise over the past year with earnings forecasted to grow by 18% annually. In this environment, identifying stocks priced below their estimated value can be a strategic approach for investors looking to capitalize on potential growth opportunities.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Western Digital (WDC) | $532.10 | $1032.87 | 48.5% |

| Rayonier (RYN) | $21.83 | $42.94 | 49.2% |

| Procore Technologies (PCOR) | $44.72 | $86.77 | 48.5% |

| Natera (NTRA) | $281.27 | $553.62 | 49.2% |

| Genuine Parts (GPC) | $128.67 | $248.48 | 48.2% |

| FatPipe (FATN) | $5.11 | $9.93 | 48.5% |

| Esquire Financial Holdings (ESQ) | $120.50 | $238.84 | 49.5% |

| Betterware de MéxicoP.I. de (BWMX) | $18.17 | $35.99 | 49.5% |

| Beacon Financial (BBT) | $30.23 | $60.24 | 49.8% |

| Amaroq (AMRQ.F) | $1.12 | $2.23 | 49.8% |

Here we highlight a subset of our preferred stocks from the screener.

Crexendo (CXDO)

Overview: Crexendo, Inc. offers cloud communication platform software and unified communications as a service both in the United States and internationally, with a market cap of $254.46 million.

Operations: The company's revenue is derived from two main segments: Software Solutions, contributing $30.52 million, and Cloud Telecommunications Services (including Web Services), generating $42.30 million.

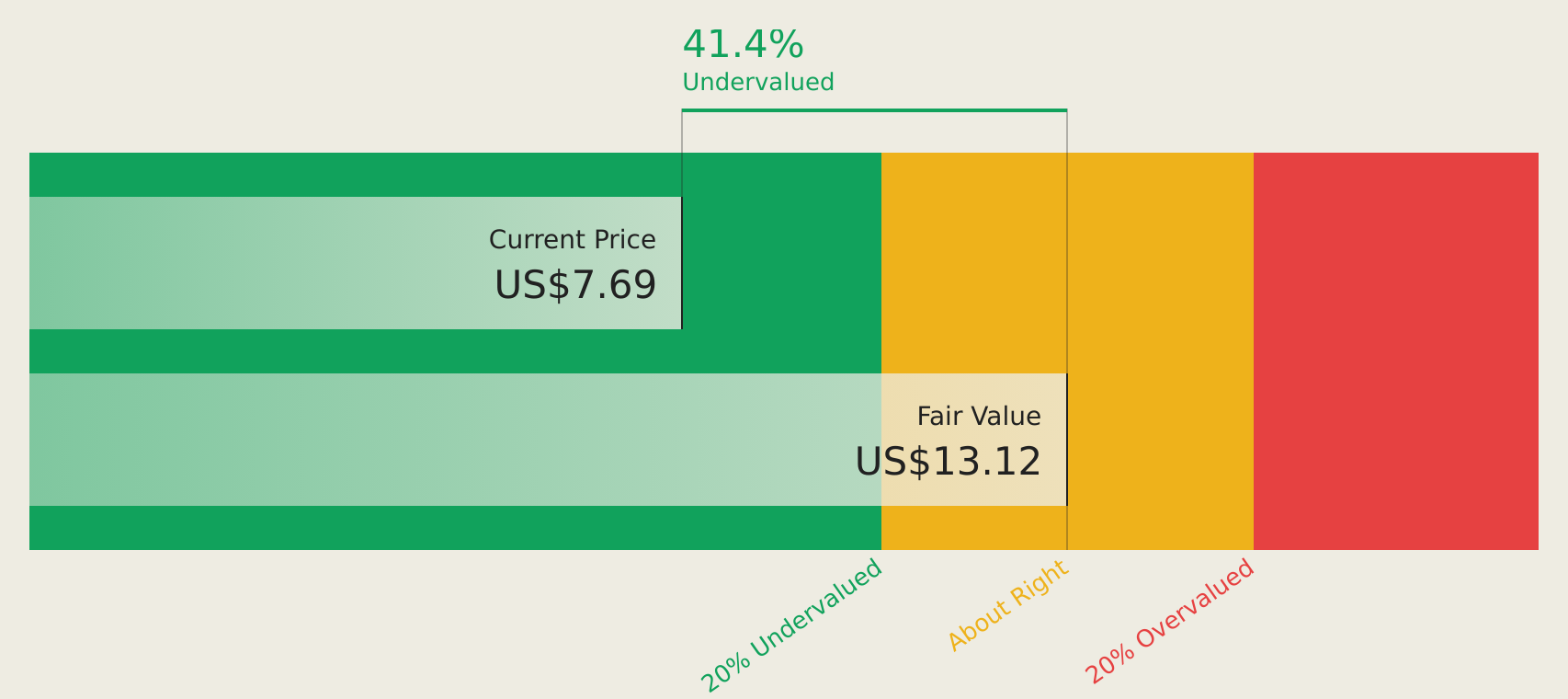

Estimated Discount To Fair Value: 40.1%

Crexendo is trading at US$7.87, significantly below its estimated future cash flow value of US$13.13, indicating potential undervaluation based on cash flows. Despite recent insider selling, the company's earnings are forecast to grow by 39.5% annually, outpacing the broader U.S. market's growth rate of 18.4%. Recent additions to the Russell 2000 Growth-Defensive Index and strategic debt financing for acquisitions may bolster future growth prospects and operational efficiency.

- According our earnings growth report, there's an indication that Crexendo might be ready to expand.

- Click here and access our complete balance sheet health report to understand the dynamics of Crexendo.

Kingstone Companies (KINS)

Overview: Kingstone Companies, Inc., operating through its subsidiary Kingstone Insurance Company, offers property and casualty insurance products in the United States with a market cap of $291.58 million.

Operations: The company's revenue segment is derived entirely from property and casualty insurance, amounting to $224.14 million.

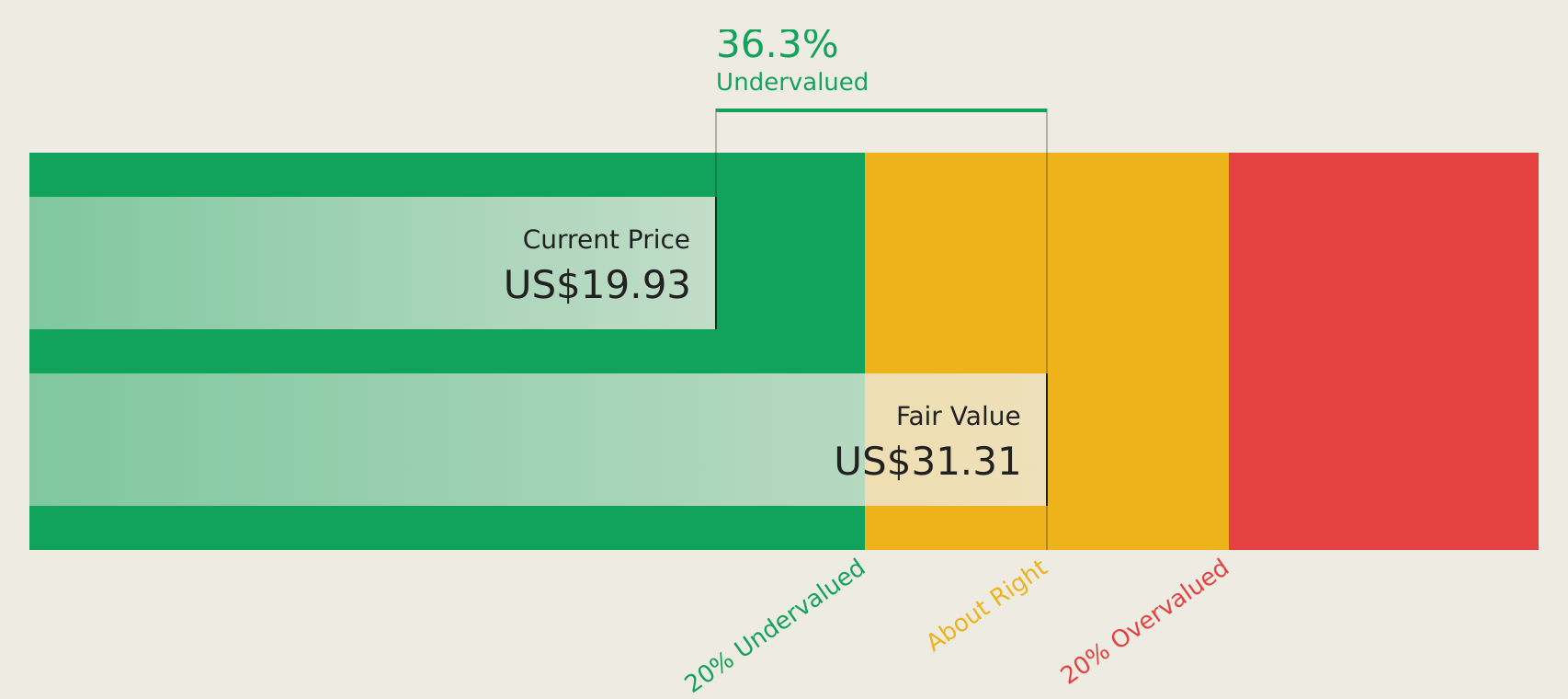

Estimated Discount To Fair Value: 35.3%

Kingstone Companies, trading at US$20.27, is undervalued compared to its estimated future cash flow value of US$31.31. Its earnings are projected to grow by 20.8% annually, surpassing the broader U.S. market's growth rate of 18.4%. Despite a recent net loss and index reclassifications, Kingstone's new loss-prevention initiative with vipHomeLink reflects a strategic focus on risk management that could enhance operational resilience and financial performance over time.

- Our growth report here indicates Kingstone Companies may be poised for an improving outlook.

- Take a closer look at Kingstone Companies' balance sheet health here in our report.

Andersen Group (ANDG)

Overview: Andersen Group Inc. offers independent tax, valuation, and financial advisory services to a diverse clientele in the United States, with a market cap of $4.28 billion.

Operations: The company's revenue primarily comes from providing a range of tax, valuation, financial advisory, and related consulting services amounting to $871.37 million.

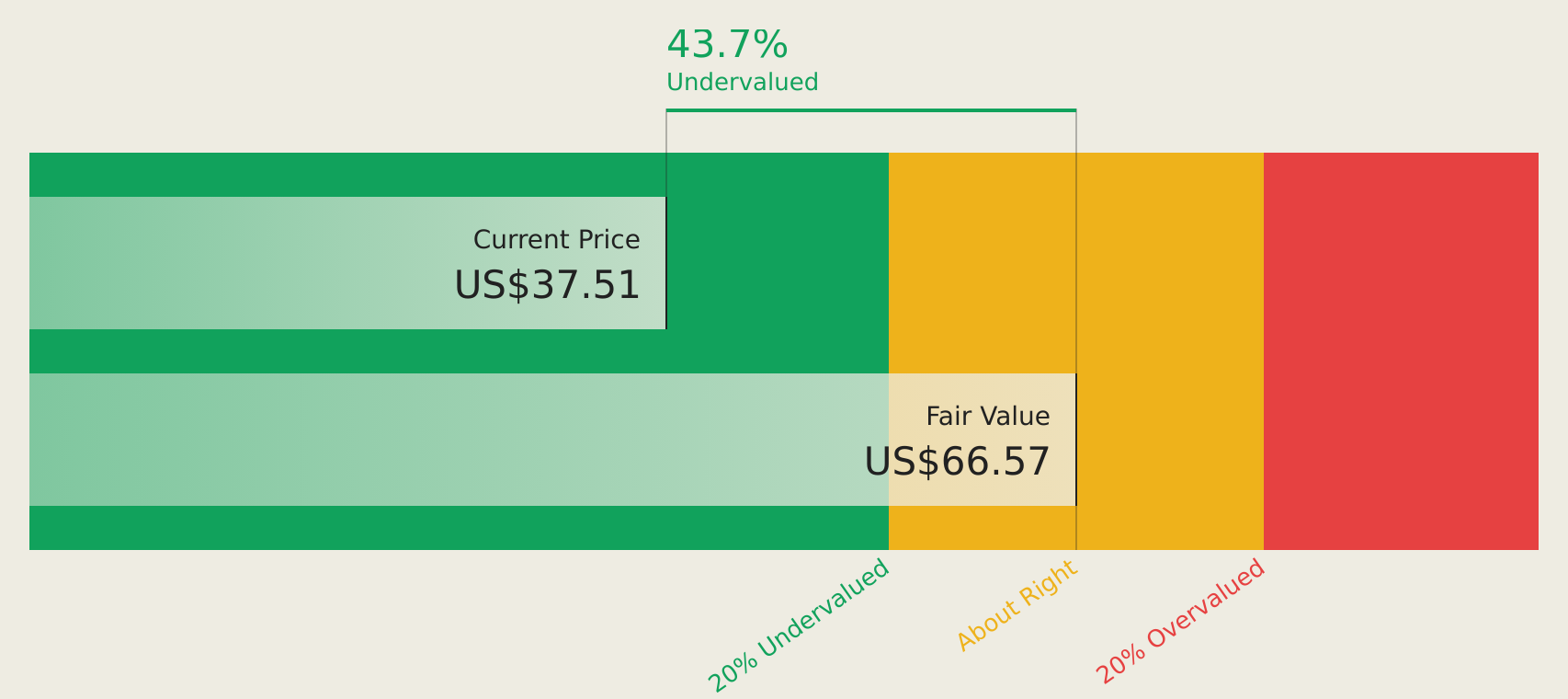

Estimated Discount To Fair Value: 38.3%

Andersen Group, trading at US$40.51, is undervalued compared to its estimated future cash flow value of US$65.70. Despite high debt levels and a recent net income dip to US$0.494 million in Q1 2026 from the previous year's US$50.58 million, Andersen's earnings are forecasted to grow significantly by over 100% annually. The company's inclusion in the S&P Global BMI Index and strategic board appointment underscore its focus on governance and growth amid slower-than-market revenue expansion projections.

- Insights from our recent growth report point to a promising forecast for Andersen Group's business outlook.

- Get an in-depth perspective on Andersen Group's balance sheet by reading our health report here.

Turning Ideas Into Actions

- Navigate through the entire inventory of 151 Undervalued US Stocks Based On Cash Flows here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com