- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

DoorDash (DASH) Deepens Auto Parts Push With AutoParts.com Partnership Is Its Logistics Edge Durable?

- In late June 2026, AutoParts.com Inc. announced its auto parts catalog went live on the DoorDash Marketplace, using geo-located inventory and a national retailer network, alongside a limited-time 20% discount for new DoorDash customers meeting minimum order requirements.

- This move pushes DoorDash further into non-food retail, testing whether its logistics and on-demand infrastructure can profitably handle complex, time-sensitive categories like auto parts.

- We’ll now examine how adding AutoParts.com’s geo-located auto parts inventory to DoorDash’s marketplace influences its broader investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

DoorDash Investment Narrative Recap

To own DoorDash, you need to believe its logistics, subscriptions, and advertising can support profitable growth as it moves well beyond restaurant delivery. The AutoParts.com launch extends that thesis into a more complex, time-sensitive retail category, but the near term story still hinges more on upcoming earnings clarity and how well DoorDash manages costs and profitability than on any single partnership.

The most relevant nearby announcement is DoorDash’s plan to report second quarter 2026 results on August 5. With the stock trading on a rich earnings multiple and recent returns lagging the broader market, that update looks important for testing whether non food efforts like auto parts, apparel, and grocery are translating into healthier margins and more durable revenue, rather than just higher volume and complexity.

Yet beneath that growth ambition, investors should be aware that rising labor and regulatory pressures could still...

Read the full narrative on DoorDash (it's free!)

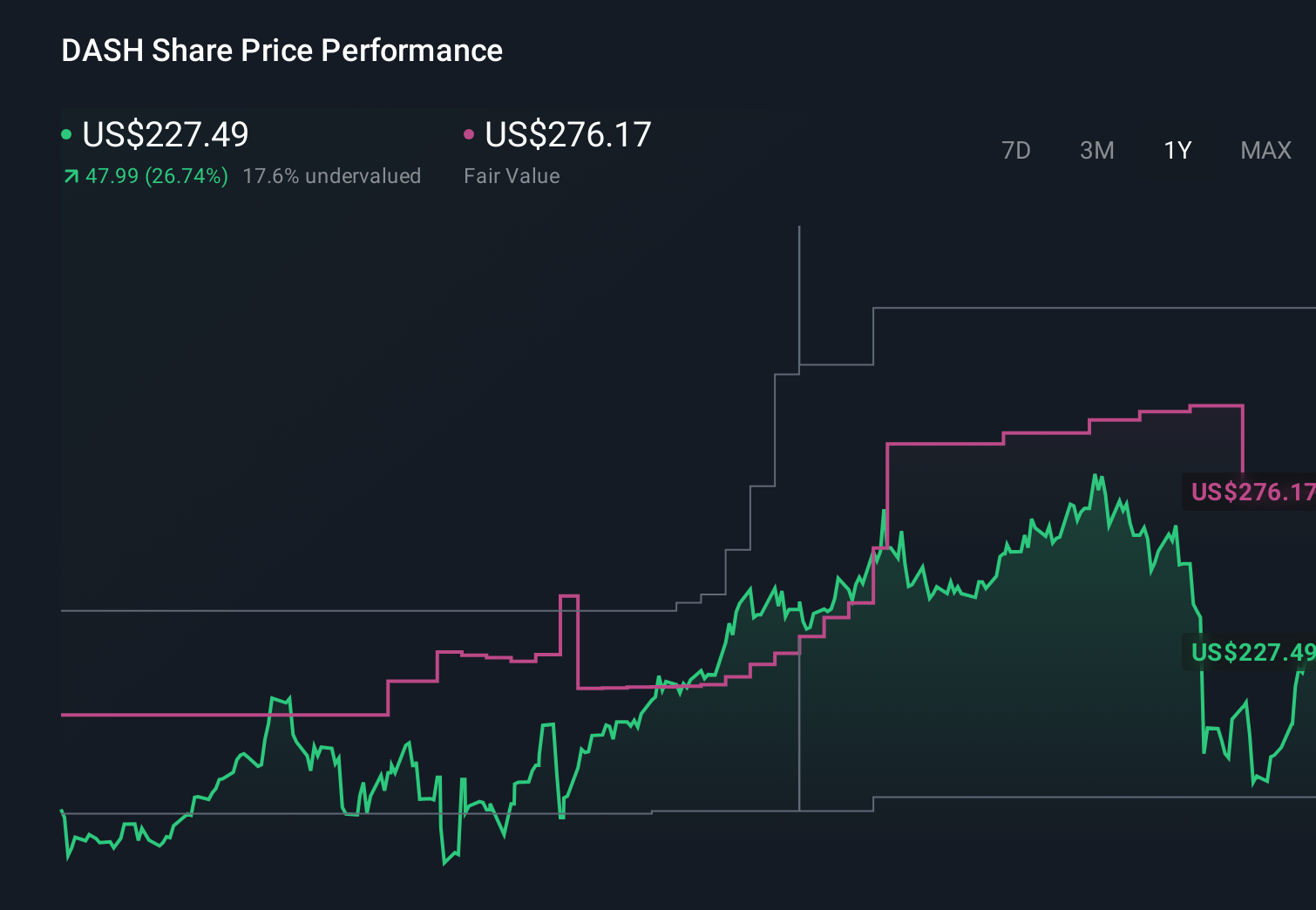

DoorDash's narrative projects $26.2 billion revenue and $3.3 billion earnings by 2029.

Uncover how DoorDash's forecasts yield a $245.99 fair value, a 26% upside to its current price.

Exploring Other Perspectives

Some of the lowest analyst estimates paint a much harsher picture, even before this AutoParts.com news, assuming around US$24.5 billion in 2029 revenue and US$2.4 billion in earnings, and warning that fee fatigue and heavier regulation could blunt the benefits of new retail categories.

Explore 10 other fair value estimates on DoorDash - why the stock might be worth 11% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your DoorDash research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free DoorDash research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DoorDash's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- Find 45 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com