- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Procter And Gamble (PG) Trades 26% Above Fair Value After Earnings Beat

Procter & Gamble (PG) is back in focus after its latest quarter showed broad-based growth, with Beauty leading top and bottom line beats. The company also marked its 70th straight annual dividend increase.

See our latest analysis for Procter & Gamble.

Procter & Gamble’s recent results and product launches, such as Braun NEVO and the new Cascade Clean and Dry Booster, have coincided with a 1-day share price return of 2.30% and a 7-day share price return of 4.17%, while the 1-year total shareholder return is slightly down 0.47%. This suggests near term momentum has picked up even as longer term returns remain more modest.

If this kind of steady consumer demand appeals to you, it could be a good moment to broaden your watchlist and check out 19 top founder-led companies

After Procter & Gamble’s recent bounce and steady dividend track record, the debate now centers on the stock’s valuation: is most of the easy upside already reflected in the price, or is there still meaningful room ahead?

Most Popular Narrative: 26.2% Overvalued

According to the most followed Procter & Gamble narrative, the latest fair value estimate of $121.06 sits well below the recent $152.75 close, which naturally raises questions for anyone tracking this steady compounder.

Procter & Gamble, despite being within a very competitive industry, still has some competitive advantages shown in its higher operating margin above the ~20% mark and the Morning Star Wide Moat. The fact that the ROIC is double the Cost of Capital suggests its capital allocation is being well managed. Its solid Moodys Debt Rating, along with the Low Uncertainty Morningstar rating, presents the company as a stable and reliable investment if the opportunity arises.

Want to see how a wide moat, premium margins and a disciplined cost of capital feed into that $121.06 figure? The key is how this narrative blends moderate growth, high returns on invested capital and a specific profit multiple assumption that does not line up neatly with the current $152.75 price.

Result: Fair Value of $121.06 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the Procter & Gamble narrative could be challenged if consumer demand weakens or if input cost pressures constrain its high operating margin profile.

Find out about the key risks to this Procter & Gamble narrative.

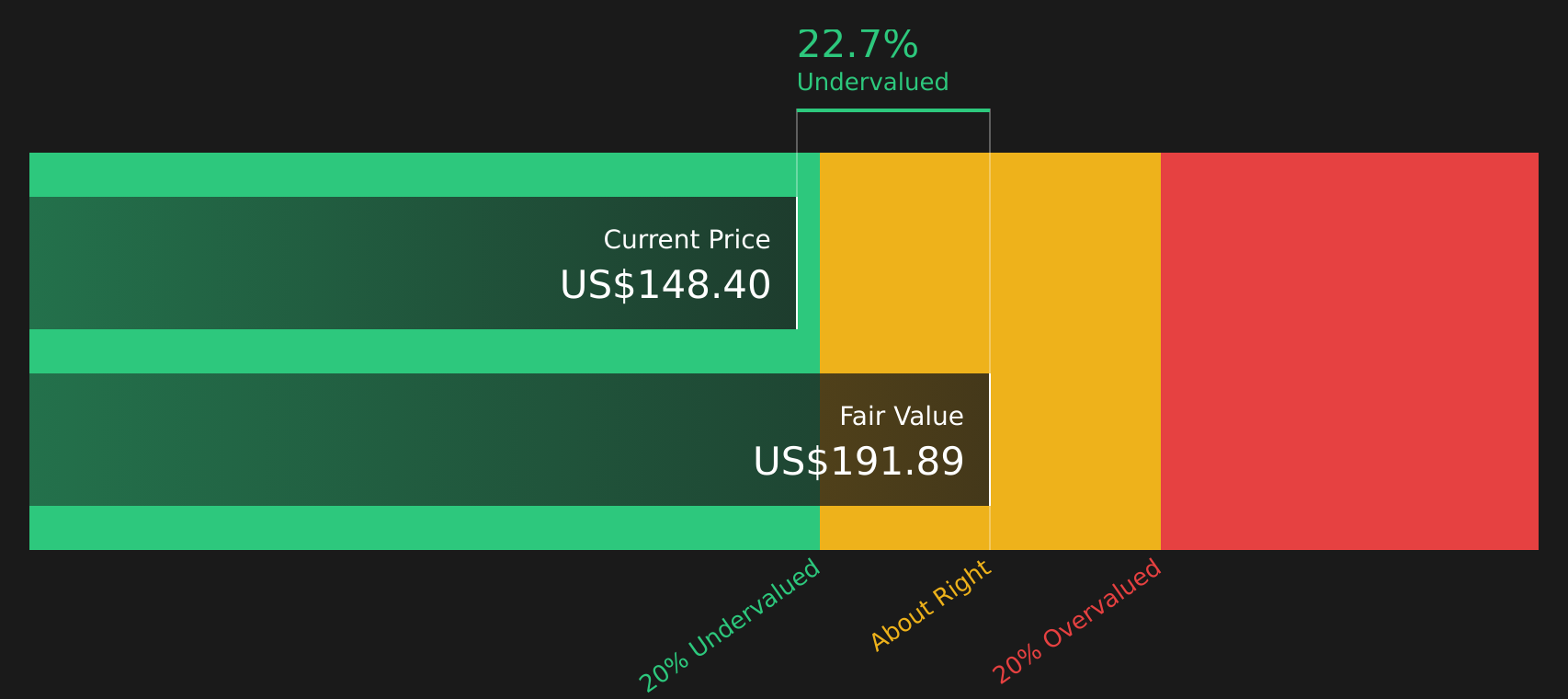

Another View On Procter & Gamble’s Valuation

The crowd narrative pegs Procter & Gamble at $121.06, about 26.2% below the recent $152.75 price. Our DCF model indicates an estimated future cash flow value of $191.89, which suggests the stock is trading below that value. Which perspective do you think is closer to reality?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

If this mixed picture on Procter & Gamble has you undecided, move quickly from reading to reviewing the numbers yourself and weigh up the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Procter & Gamble?

If Procter & Gamble’s story has sharpened your focus, do not stop here. Fresh ideas across different styles can help round out your next investing moves.

- Start building potential income strength by checking stocks that currently feature 9 dividend fortresses for investors who prioritize regular cash returns.

- Hunt for quality at a sensible price by scanning companies highlighted in the screener containing 18 high quality undiscovered gems before they attract wider attention.

- Reduce portfolio stress by reviewing companies that appear in the 74 resilient stocks with low risk scores and may better fit a steadier risk profile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com