- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is PVH’s New 2031 Multicurrency Credit Facility Reshaping the Investment Case for PVH (PVH)?

- In late June 2026, PVH Corp. entered into a new Credit Agreement that introduced a €400,000,000 term loan A and a US$1,500,000,000 multicurrency revolving credit facility maturing in 2031, replacing its prior 2022 financing.

- This long-dated, flexible borrowing structure, with the ability to add up to an extra US$1,500,000,000 in term or revolving commitments, reshapes PVH’s financial toolkit for funding operations and managing regional currency needs.

- We’ll now assess how this expanded, multicurrency credit capacity interacts with analyst concerns about weaker European demand in PVH’s investment narrative.

Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

PVH Investment Narrative Recap

To own PVH, you need to believe its Calvin Klein and Tommy Hilfiger brands can stay relevant while the company protects margins amid global cost and tariff pressures. The new €400 million term loan and US$1,500,000,000 multicurrency revolver do not directly shift the key near term catalyst, which remains execution in Europe, or the biggest risk, which is margin pressure from tariffs and promotions across already challenged regions.

The June 3, 2026 guidance update is the clearest recent reference point against which to view this new credit capacity. Management now expects full year 2026 revenue to be roughly flat and Q2 revenue down 3% to 4%, and analysts have flagged softer European demand. The expanded facility gives PVH more room to support operations and currency needs while it works through these near term demand and margin pressures.

Yet investors should also weigh how prolonged tariff and discounting pressure could affect PVH’s ability to sustain margins and earnings growth over time...

Read the full narrative on PVH (it's free!)

PVH's narrative projects $9.6 billion revenue and $734.4 million earnings by 2029.

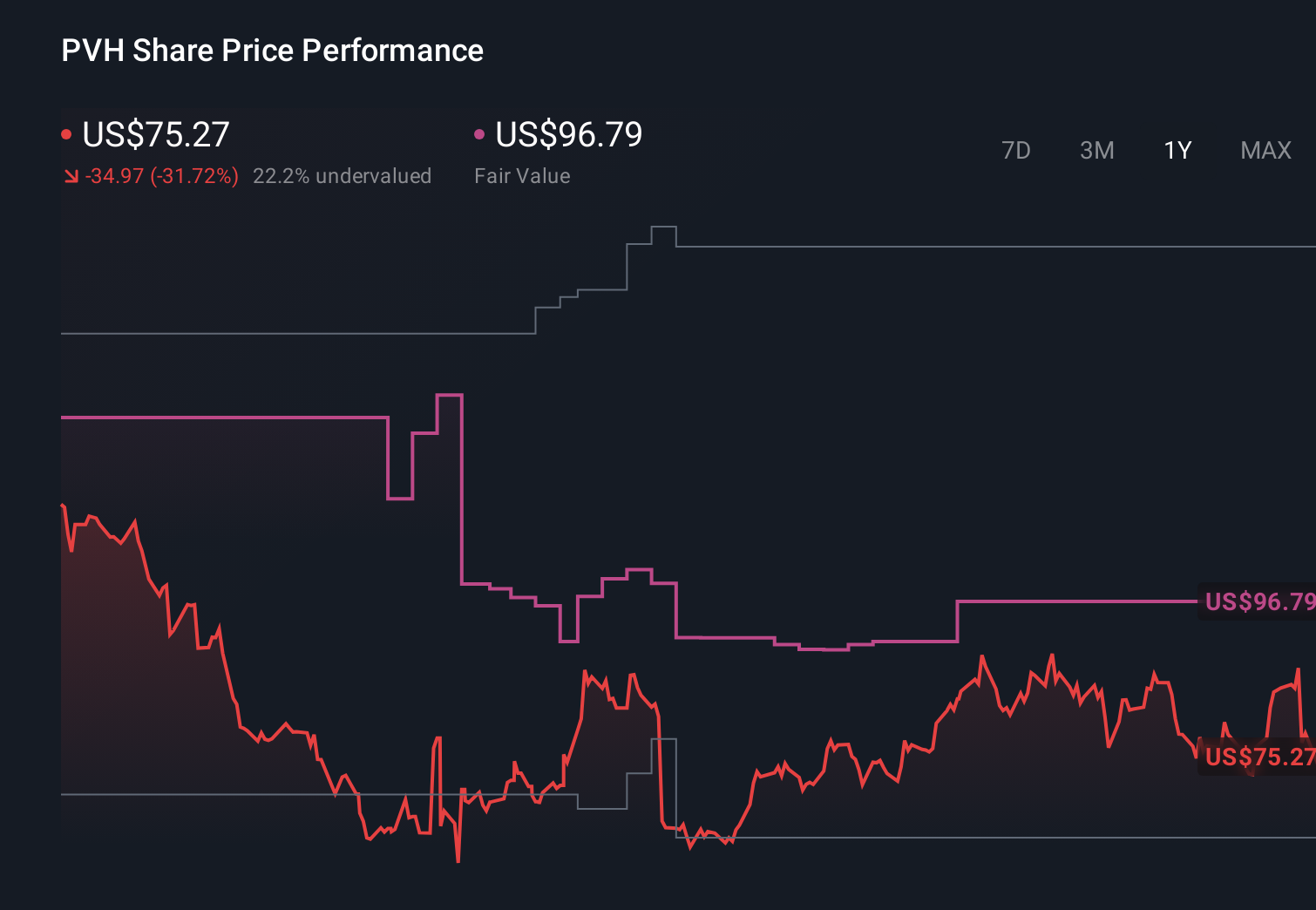

Uncover how PVH's forecasts yield a $93.08 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were looking for earnings to climb toward about US$771 million over time, which contrasts sharply with current margin concerns and shows how widely views can differ, especially if tariff headwinds play out differently than expected.

Explore 3 other fair value estimates on PVH - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your PVH research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free PVH research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PVH's overall financial health at a glance.

Seeking Other Investments?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Find 41 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com