- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Exploring July 2026's Undervalued Small Caps With Insider Buying

Over the last 7 days, the United States market has remained flat, yet it has risen by 20% over the past year with earnings projected to grow by 18% annually in the coming years. In such a dynamic environment, identifying stocks that are potentially undervalued and have insider buying can offer intriguing opportunities for investors looking to capitalize on future growth prospects.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Betterware de MéxicoP.I. de | 10.2x | 0.8x | 49.14% | ★★★★★★ |

| Appian | 2022.4x | 2.3x | 34.37% | ★★★★★☆ |

| Industrial Logistics Properties Trust | NA | 1.3x | 39.65% | ★★★★★☆ |

| Bank of Marin Bancorp | NA | 12.9x | 27.61% | ★★★★☆☆ |

| Peoples Bancorp | 12.6x | 3.3x | 40.16% | ★★★★☆☆ |

| German American Bancorp | 13.2x | 4.8x | 39.46% | ★★★☆☆☆ |

| Bank of the James Financial Group | 10.5x | 2.3x | 18.55% | ★★★☆☆☆ |

| Patria Investments | 24.9x | 4.5x | 7.34% | ★★★☆☆☆ |

| Shore Bancshares | 12.2x | 3.4x | 2.23% | ★★★☆☆☆ |

| Union Bankshares | 10.2x | 2.1x | 15.98% | ★★★☆☆☆ |

Let's uncover some gems from our specialized screener.

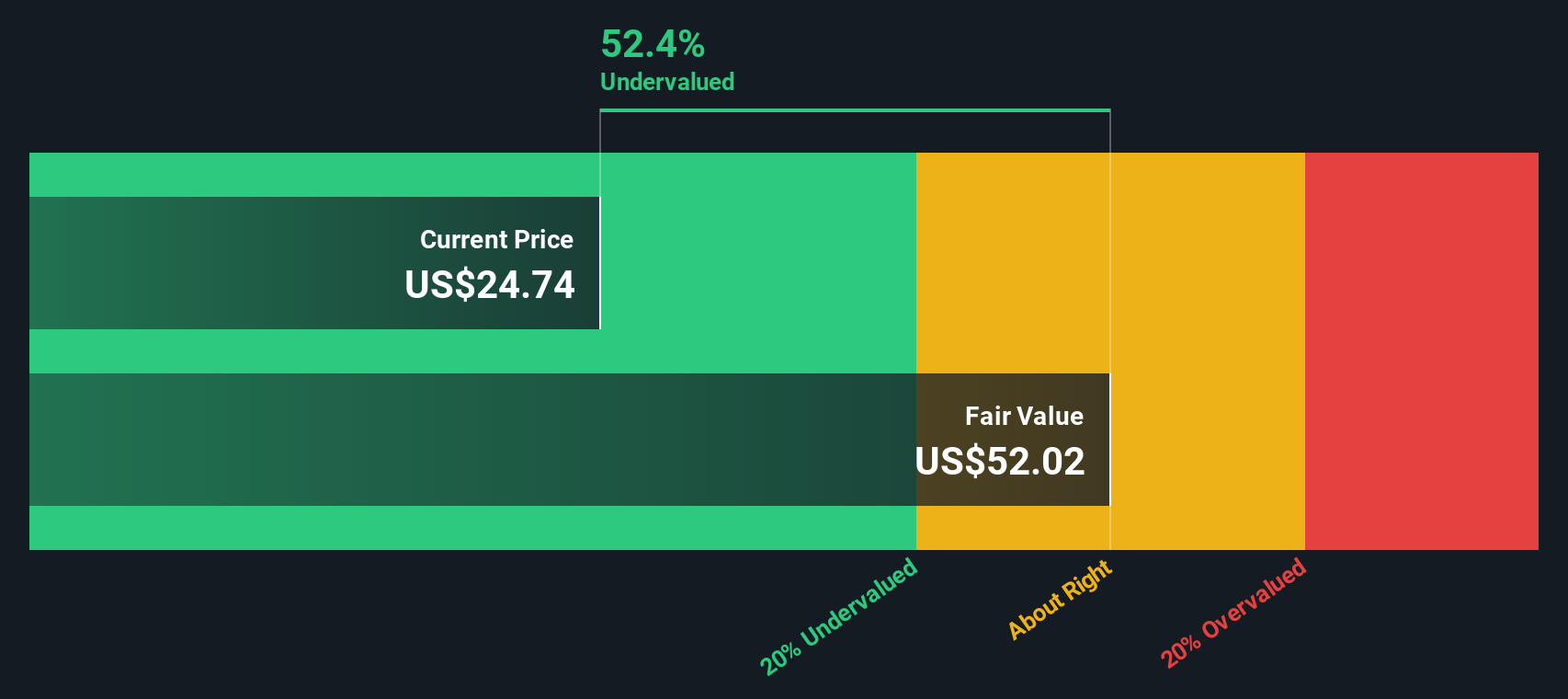

Burke & Herbert Financial Services (BHRB)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Burke & Herbert Financial Services operates in the community banking sector, with a focus on providing financial services, and has a market capitalization of $0.41 billion.

Operations: BHRB's revenue primarily comes from community banking, with a gross profit margin consistently at 100%. The net income margin has shown variability, peaking at 34.39% in late 2025. Operating expenses have been significant, with general and administrative expenses being the largest component.

PE: 12.0x

Burke & Herbert Financial Services, a smaller player in the financial sector, recently saw its removal from the Russell 2000 Dynamic Index as of June 27, 2026. Despite this setback, insider confidence is evident with recent purchases by company executives. The firm reported steady earnings for Q1 2026 with net income at US$27.35 million and basic EPS holding at US$1.8. With leadership changes underway and earnings growth forecasted at 25% annually, there’s potential for future value realization in this underappreciated stock.

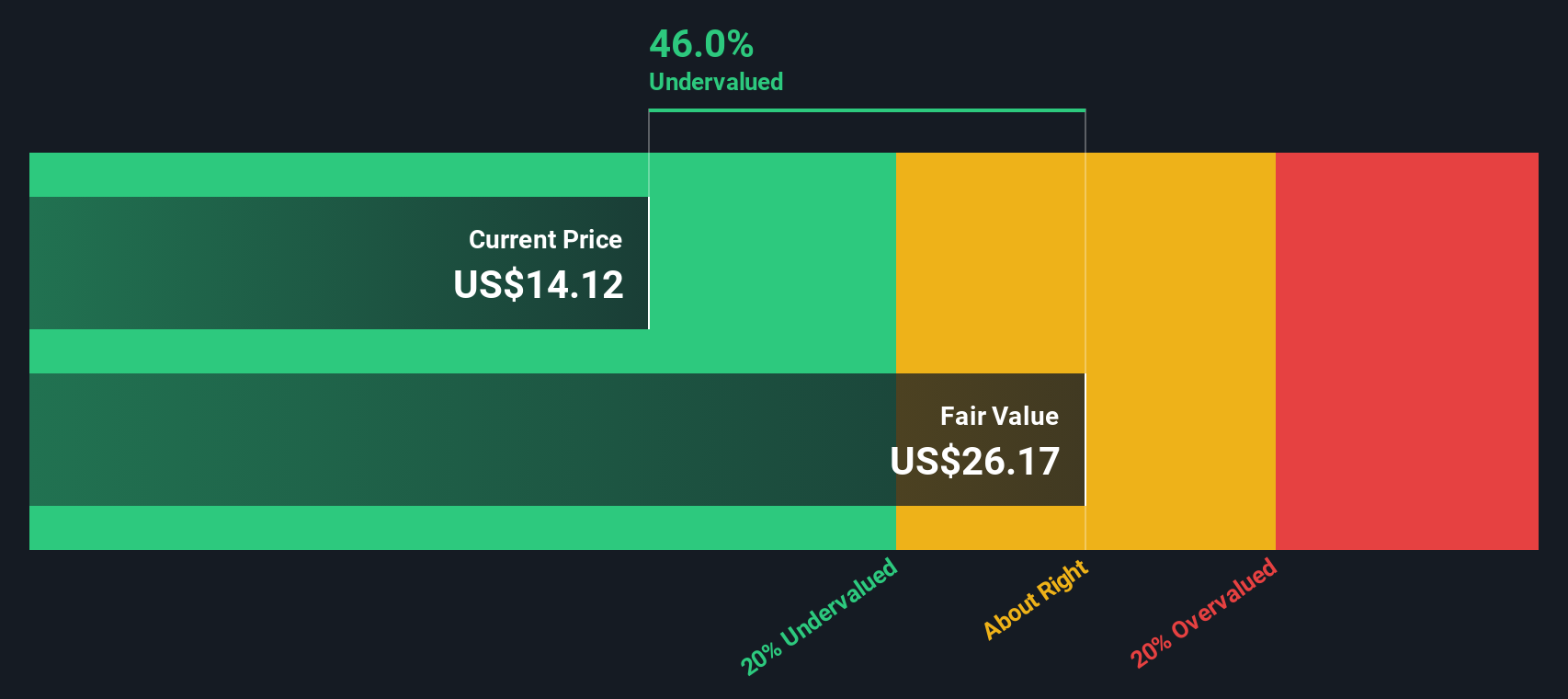

Investar Holding (ISTR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Investar Holding is a financial services company primarily engaged in banking operations, with a market capitalization of approximately $0.25 billion.

Operations: Investar Holding's primary revenue stream is from its banking operations, with a recent quarterly revenue of $107.12 million. The company's net income margin has shown variability, reaching 25.25% in the latest period. Operating expenses are significant, with general and administrative expenses consistently comprising a large portion of these costs.

PE: 14.9x

Investar Holding, a smaller U.S. company, recently experienced significant insider confidence with purchases from January to March 2026. Despite being dropped from the Russell 2000 Dynamic Index on June 27, they reported impressive first-quarter earnings growth: net income reached US$12.02 million compared to US$6.29 million a year ago. A recent dividend increase and consistent share repurchases suggest potential value appreciation amidst industry challenges and auditor changes in June 2026.

- Dive into the specifics of Investar Holding here with our thorough valuation report.

Assess Investar Holding's past performance with our detailed historical performance reports.

UMH Properties (UMH)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: UMH Properties focuses on the ownership and operation of manufactured home communities, with a market cap of approximately $1.41 billion.

Operations: The company's revenue primarily comes from its ownership and operation of manufactured home communities, generating $265.95 million. Over the observed periods, the gross profit margin has shown a gradual increase, reaching 54.67% by March 2026. Operating expenses have consistently been a significant part of the cost structure, with depreciation and amortization being notable components.

PE: 149.4x

UMH Properties, a company known for its real estate investments, recently saw insider confidence with share purchases from January to March 2026. The stock's addition to multiple Russell indices on June 27, 2026, underscores its potential in the market. Despite challenges like activist pressure and executive transitions, UMH maintains a strong position with a $260 million credit facility and projected earnings growth of up to 24% annually. Recent dividend affirmations further highlight financial stability amidst evolving leadership dynamics.

- Click here and access our complete valuation analysis report to understand the dynamics of UMH Properties.

Gain insights into UMH Properties' past trends and performance with our Past report.

Turning Ideas Into Actions

- Click this link to deep-dive into the 60 companies within our Undervalued US Small Caps With Insider Buying screener.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com