- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

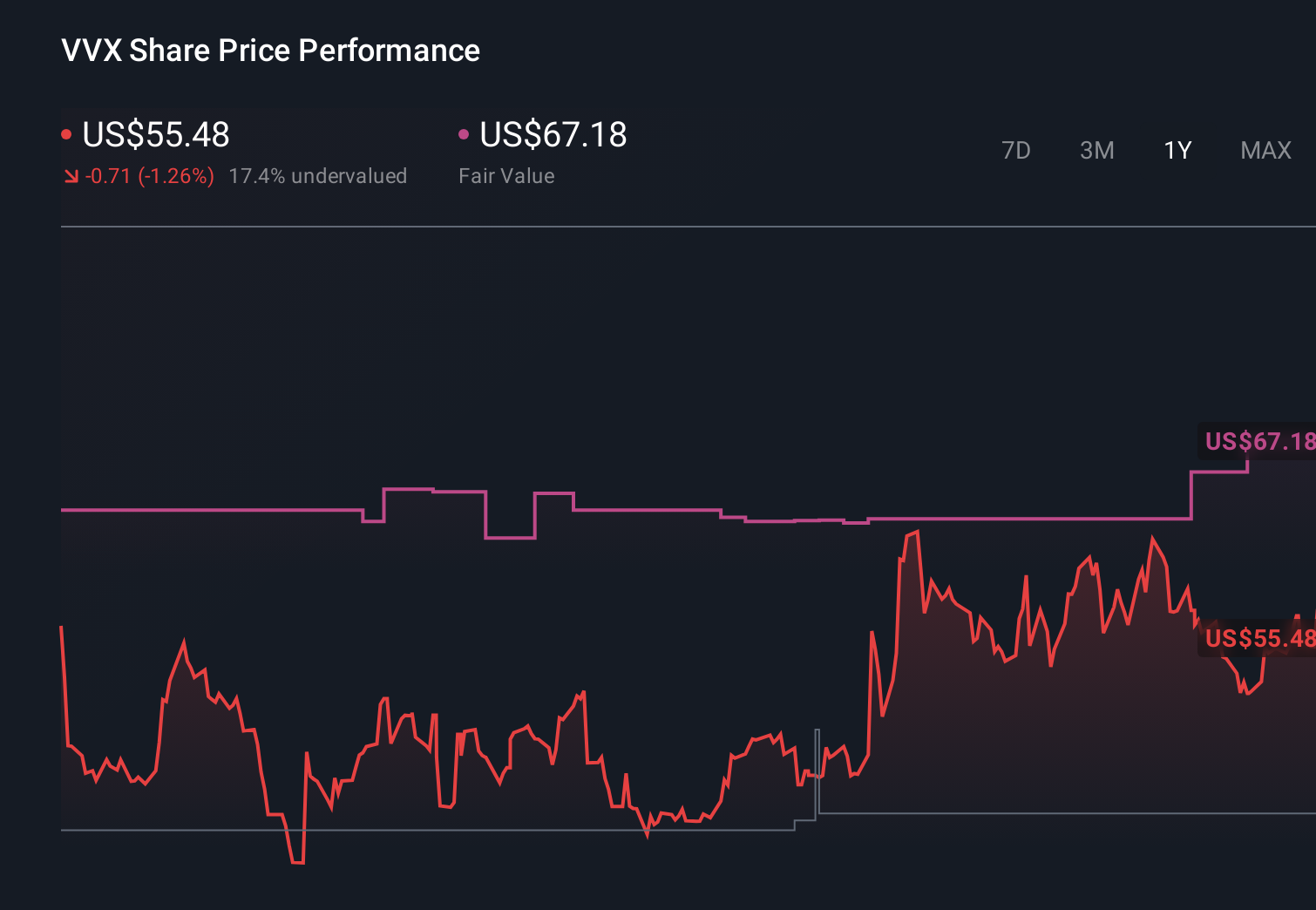

V2X (VVX) Is Up 8.3% After Winning US$500M C-12 Support Deal Has The Bull Case Changed?

- In late June, V2X was awarded a ceiling US$500 million firm-fixed-price, indefinite-delivery/indefinite-quantity contract to provide contractor logistic support for the U.S. Air Force’s C-12 aircraft fleet, including Foreign Military Sales work through June 2031.

- This long-duration logistics award adds a sizable program to V2X’s contract portfolio, reinforcing its role in mission-critical aviation support for U.S. and allied forces.

- We’ll now examine how this long-term C-12 support award may influence V2X’s investment narrative built around large, episodic defense contracts.

Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

V2X Investment Narrative Recap

To own V2X, you need to believe its model of winning large, episodic defense contracts can translate into steadier cash flows as programs ramp and integrate. The new US$500 million C 12 logistics IDIQ improves near term award momentum but, given its ceiling and duration, does not on its own resolve the key near term risk around securing enough new, sizeable awards to offset backlog runoff and book to bill pressures.

The most relevant recent announcement is the restart of work on the US$4.3 billion T 6 COMBS contract after the protest was resolved in February 2026. Together with the C 12 award, this reinforces V2X’s positioning on long term, fixed price and outcome based programs that support its modernization catalyst, while also heightening execution and margin risk as more of the portfolio shifts to contracts where cost discipline is critical.

Yet investors should be aware that if fixed price programs underperform or are delayed, the impact on margins and backlog could be far more severe than...

Read the full narrative on V2X (it's free!)

V2X's narrative projects $5.5 billion revenue and $196.9 million earnings by 2029. This requires 5.1% yearly revenue growth and about a $108.2 million earnings increase from $88.7 million today.

Uncover how V2X's forecasts yield a $79.42 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling earnings near US$249 million by 2029 and faster margin expansion, in contrast to more cautious views on contract concentration risk and execution, so you should expect that both bullish and conservative narratives may shift meaningfully as awards like C 12 are layered onto those earlier assumptions.

Explore 3 other fair value estimates on V2X - why the stock might be worth just $79.42!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your V2X research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free V2X research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate V2X's overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com