- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Archrock (AROC) Names A New CFO, Is The Stock 34% Undervalued?

Archrock (AROC) has been in focus after appointing Mohit Singh as Chief Financial Officer and Senior Vice President, a leadership change that arrives just days before the stock exits the Russell 2000 Dynamic Index.

See our latest analysis for Archrock.

Archrock’s share price has recently pulled back, with a 1 day share price return of down 5.08% and a 7 day return of down 12.30%. However, the 30 day and year to date share price returns of 7.57% and 38.15% keep the broader trend positive and align with a 1 year total shareholder return of 53.53% and a larger 3 year total shareholder return. This suggests sentiment is pausing rather than reversing around the CFO appointment and upcoming index removal.

If this leadership change has you reassessing your watchlist, it could be a moment to broaden your search using our screener for 35 power grid technology and infrastructure stocks

With Archrock still showing strong multi year total returns and trading at a 34.13% discount to an estimated intrinsic value, as well as about 15.07% below the average analyst price target, the key question is whether this signals a genuine opportunity or if the market is simply recalibrating and already factoring in any future growth.

Most Popular Narrative: 13.1% Undervalued

With Archrock last closing at $36.79 against a narrative fair value of $42.33, the current pullback sits in the shadow of a model that leans higher and builds in a detailed view of future cash flows.

The company's ongoing transformation to a modern, high-horsepower fleet and longer customer commitments (average contract duration now exceeding six years) is translating to higher margins, enhanced operational stability, and increased earnings visibility. Integration of digital fleet optimization and remote monitoring is improving equipment uptime and operational efficiency, likely driving margin expansion and EPS growth over time through cost containment and service consistency.

Want to see what kind of revenue path and margin profile need to line up with that fleet shift? The fair value hinges on a specific growth glide path, a target profitability range, and a future earnings multiple that sets a clear bar for Archrock.

Result: Fair Value of $42.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the Archrock narrative could be challenged if U.S. natural gas demand weakens or if regulations and alternative technologies reduce compression equipment deployment and contract renewals.

Find out about the key risks to this Archrock narrative.

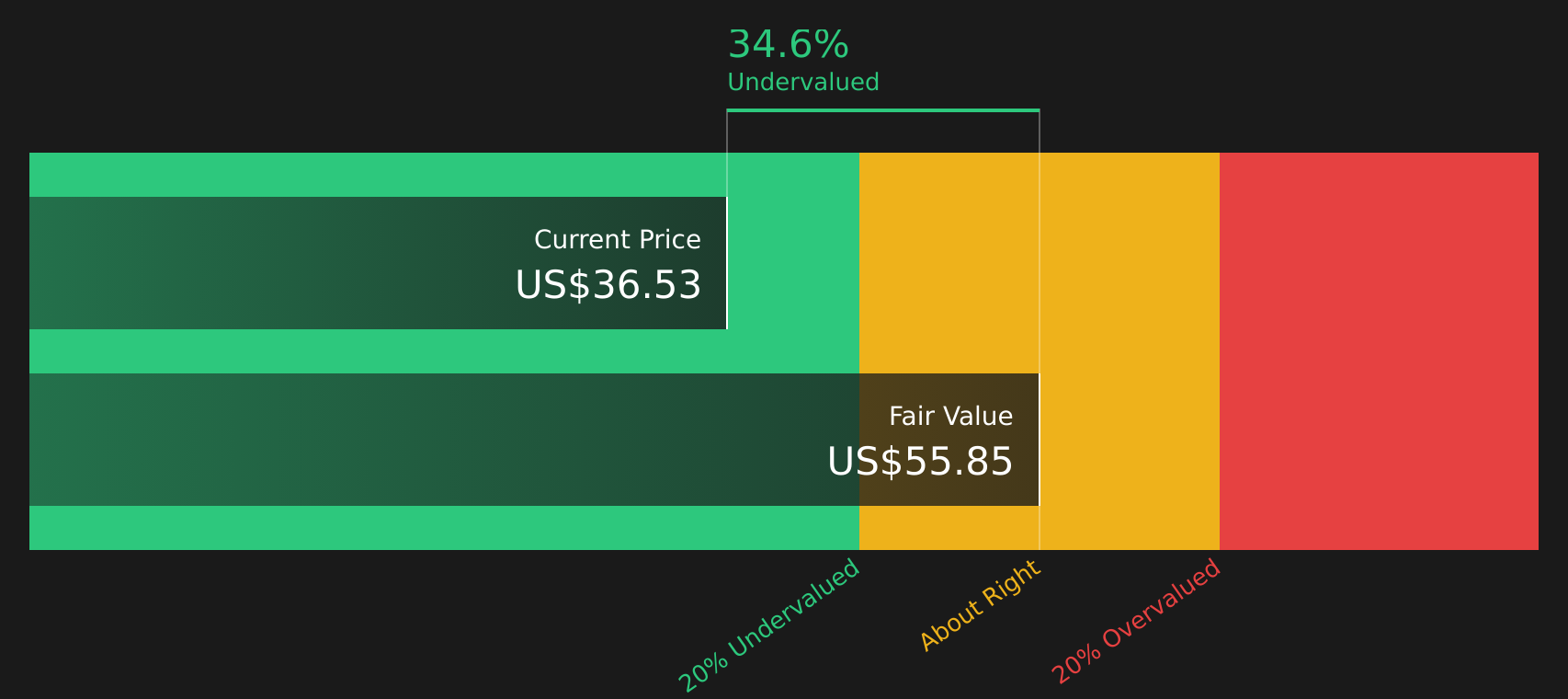

Another View on Archrock’s Valuation

The DCF work suggests Archrock is trading at a 34.1% discount to an estimated future cash flow value of $55.85, a steeper gap than the 13.1% discount to the $42.33 narrative fair value. That difference raises a simple question: which set of assumptions do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

If the mixed tone around Archrock has you undecided, take a close look at the numbers, weigh the potential upside against the concerns, and let the balance of 3 key rewards and 3 important warning signs guide your own conclusion.

Looking for more ideas beyond Archrock?

Before moving on from Archrock, take a moment to broaden your opportunity set with a few focused stock lists that can surface ideas you might otherwise miss.

- Target potential mispricings by scanning companies that combine quality fundamentals with attractive valuations using the 44 high quality undervalued stocks.

- Strengthen your portfolio’s core by reviewing businesses with robust finances through the solid balance sheet and fundamentals stocks screener (47 results).

- Get ahead of the crowd by searching for lesser known prospects with strong fundamentals in the screener containing 18 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com