- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Fast Growing Australian Stocks With High Insider Ownership Worth A Closer Look

With inflation trends easing in some regions, interest rate paths looking more measured, and growth signals mixed across major economies, many investors are looking for companies that can rely on their own earnings power rather than broad market momentum. Fast growing stocks with high insider ownership can fit that brief, because management teams have a meaningful stake in the outcome and analysts are optimistic about their prospects. This article profiles 3 stocks from the Fast Growing Stocks With High Insider Ownership screener and highlights why this theme may appeal if you want growth potential supported by aligned insiders.

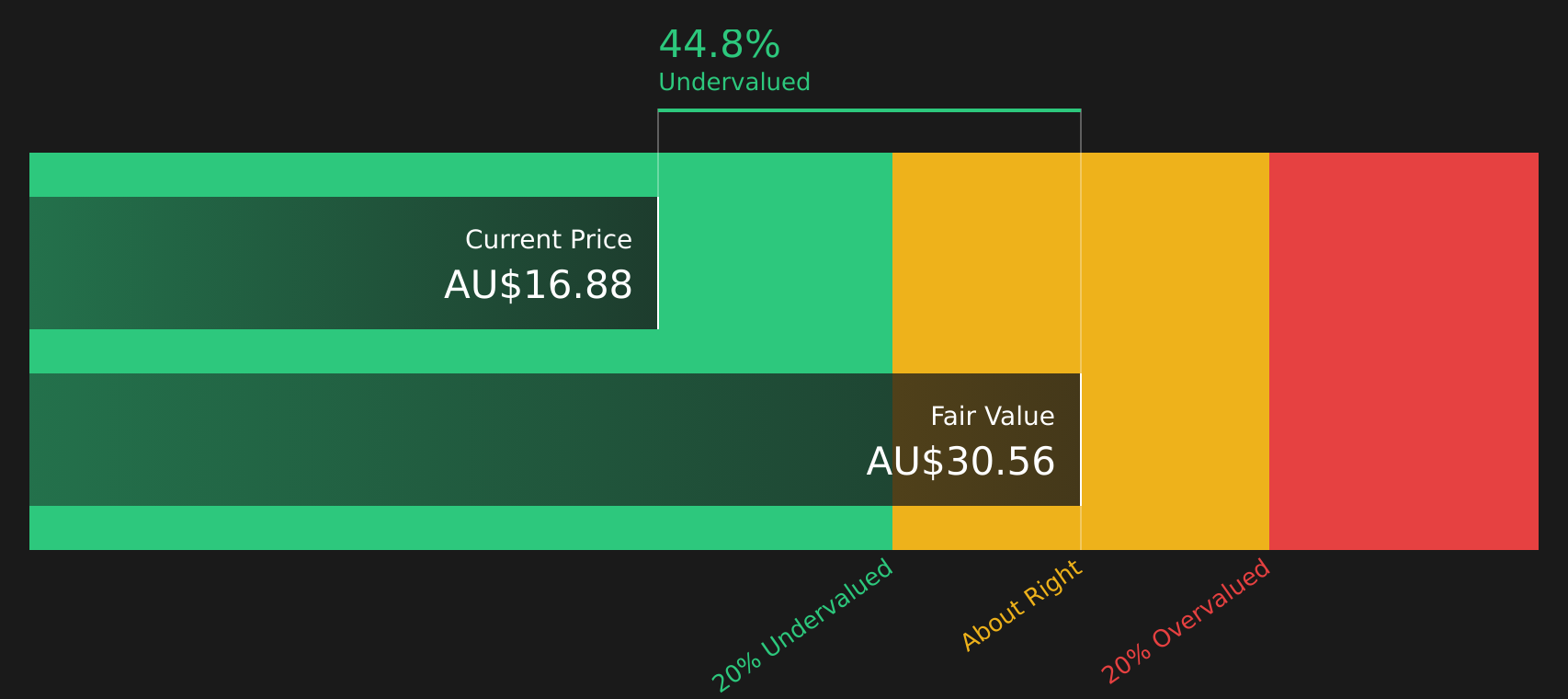

Telix Pharmaceuticals (ASX:TLX)

Overview: Telix Pharmaceuticals is a commercial stage biopharmaceutical company that develops and sells radiopharmaceutical products that help doctors locate and treat cancers, with a focus on prostate, kidney, brain and other solid tumours across key markets including the United States, Europe, China and Japan.

Operations: Telix generates most of its revenue from Precision Medicine at about US$621.9m, with additional contributions from Manufacturing Solutions at about US$245.1m and Therapeutics at about US$9.3m, partly offset by US$72.5m of inter segment eliminations, and the United States contributing about US$784.9m of geographic revenue.

Market Cap: A$5.7b

Telix Pharmaceuticals stands out in this screener because it already sells prostate cancer imaging agents globally while investing heavily in a therapeutic pipeline that targets prostate, kidney and brain cancers, so you are not just looking at a pre revenue story. Some investors may find it notable that the stock trades on a lower P/S than many peers and sits well below some fair value estimates, which can appeal to those seeking exposure to companies with growth pipelines at a more measured entry price. At the same time, unprofitability, rising R&D spend, pricing pressure in PSMA imaging, SEC scrutiny and high dependence on clinical trial outcomes mean that risk remains elevated. For investors who can tolerate that mix of potential opportunity and execution risk, Telix may warrant a much closer look.

Telix’s commercial sales and broad cancer pipeline are attracting attention, but the real question is how that story lines up with its valuation and insider alignment in the analysis report for Telix Pharmaceuticals

Lindian Resources (ASX:LIN)

Overview: Lindian Resources is a Perth based minerals explorer focused on rare earths, bauxite and gold across Africa and Australia, with its key asset being the Kangankunde Rare Earths project in Malawi.

Market Cap: A$1.7b

Lindian Resources is attracting attention because it is moving from exploration into active rare earths mining at Kangankunde, with first production targeted for Q4 2026 and a new Singapore hub set up to handle in house sales and logistics. Analysts expect very fast revenue and earnings growth, with forecasts for triple digit revenue growth and a potential shift to profitability within three years. This is what earns Lindian a place in a growth focused screener. On the other side of the ledger, the company is still loss making, has seen meaningful shareholder dilution, carries funding risk and has a very new board and management team. Investors therefore need to weigh the promise of a high growth critical minerals project against material execution and governance risks.

Accelerating rare earths ambitions at Lindian Resources sit alongside shareholder dilution, funding needs and a new leadership team. The real story sits in how those pieces fit together in the 1 key reward and 2 important warning signs (2 are major!)

GemLife Communities Group (ASX:GLF)

Overview: GemLife Communities Group develops, builds, owns and operates resort style land lease communities for over 50s across Australia, combining home sales with community management and recreational facilities to support active, socially engaged living.

Operations: GemLife Communities Group generates A$259.8m from Development and A$21.9m from Community Operations, with all A$281.7m of reported revenue coming from Australia.

Market Cap: A$1.7b

GemLife Communities Group catches the eye because it couples a long pipeline of around 8,300 homesites and a vertically integrated building model with a growing base of recurring site rental income indexed to CPI or a 3.5% floor. Analysts expect revenue and earnings growth ahead, yet the stock carries a high P/E multiple and has recently faced a decline in profit margins, one off losses and funding that relies entirely on external borrowings. Add in a relatively young board and gearing expected in the 25% to 35% range, and this suggests a business with meaningful growth ambitions but real balance sheet and execution risks that investors need to weigh carefully.

GemLife Communities Group looks like a growth story that could be masking deeper questions around gearing, margins and that premium P/E. See how those pieces line up in the 3 key rewards and 2 important warning signs (1 is major!)

The 3 stocks here are only a starting point. The full Fast Growing Stocks With High Insider Ownership screener surfaces 98 more companies where insiders and analysts appear aligned on growth potential in the Fast Growing Stocks With High Insider Ownership screener. Use Simply Wall St to identify, filter and analyze the specific catalysts and narratives that matter to you so you can focus on the highest conviction opportunities that fit your own criteria.

Take Control of Your Investment Journey

If Telix Pharmaceuticals or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd Moves?

Fresh breakouts, shifting momentum and under the radar stocks do not stay quiet for long. Scan these ideas before the data goes stale and consider your options early.

- Spot companies quietly building momentum and solid financials by running the list of solid balance sheet and fundamentals (20 results), which filters for strength before the crowd notices.

- Target cash generative AI opportunities, not just hype driven stories, with the curated 62 profitable AI stocks that aren't just burning cash that highlights businesses already turning technology into earnings.

- Zero in on income ideas that aim to hold up when sentiment drops by reviewing the hand picked 6 dividend fortresses built for more resilient yield hunters.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com