- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is Conagra’s Index Exit And Product Blitz Altering The Investment Case For Conagra Brands (CAG)?

- In late June 2026, Conagra Brands was removed from the S&P 500 and related indices and added to smaller-cap benchmarks, while launching nearly 100 new frozen and grocery products focused on high protein, convenience and value across brands like Banquet, Healthy Choice and Marie Callender’s.

- This combination of index reclassification and an unusually broad product rollout highlights how Conagra is repositioning itself with investors and consumers at the same time.

- We’ll now examine how Conagra’s shift into small-cap indices, alongside its aggressive new product slate, may reshape its existing investment narrative.

Find 44 companies with promising cash flow potential yet trading below their fair value.

Conagra Brands Investment Narrative Recap

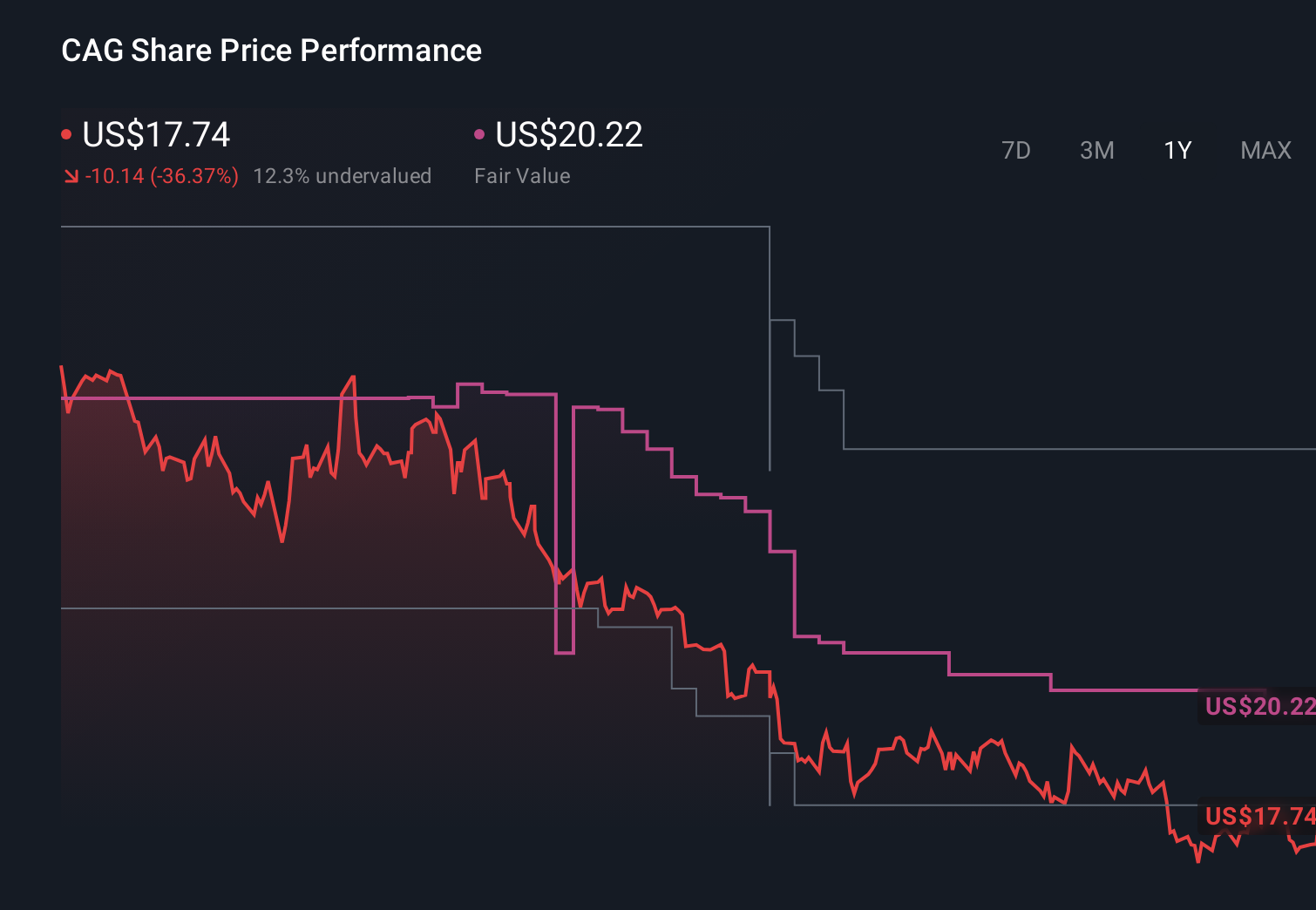

To own Conagra Brands today, you need to believe its large packaged food portfolio can translate steady demand into healthier margins and a return to sustainable profitability. The key short term catalyst is whether operational improvements and price mix can lift earnings from recent losses, while the biggest risk remains ongoing cost inflation and shifting consumer preferences away from processed foods. The recent index changes and product launches do not materially alter those near term drivers on their own.

The most relevant recent announcement is Conagra’s launch of nearly 100 new frozen and grocery items across Banquet, Healthy Choice, Marie Callender’s and other brands, many with higher protein and value pricing. If these products gain traction, they could support the consensus catalyst of better capacity utilization and productivity gains, helping to offset inflation and supply chain pressures that still threaten margins and cash flow.

Yet behind the new products, investors should be aware that rising regulatory scrutiny on additives and ingredients could...

Read the full narrative on Conagra Brands (it's free!)

Conagra Brands' narrative projects $11.3 billion revenue and $834.3 million earnings by 2029. This requires flat yearly revenue growth and a $877.6 million earnings increase from -$43.3 million today.

Uncover how Conagra Brands' forecasts yield a $14.59 fair value, in line with its current price.

Exploring Other Perspectives

Some analysts take a much more optimistic view than consensus, assuming revenue of about US$11.5 billion and earnings near US$980 million by 2029, but the same concerns about heavy exposure to processed foods and potential regulatory pressure on ingredients show how differently you and other investors can interpret the June product surge and index shift, and why these pre news forecasts may need a fresh look.

Explore 10 other fair value estimates on Conagra Brands - why the stock might be worth just $14.00!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Conagra Brands research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Conagra Brands research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Conagra Brands' overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com