- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Does STERIS (STE) Insider Option Exercise Quietly Reframe the Cash Flow and Spending Debate?

- On July 1, 2026, STERIS plc director Mohsen Sohi exercised options to acquire 3,781 Ordinary Shares at US$71.40 each via a net cashless transaction, increasing his direct holding to 26,142 shares.

- This insider move comes as STERIS attracts renewed attention for its steady cash flow and recurring healthcare service demand amid ongoing valuation debate.

- With insider equity exposure rising alongside questions about cash flow strength and spending needs, we’ll now assess how this shapes STERIS’s investment narrative.

Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

STERIS Investment Narrative Recap

To own STERIS, you need to believe in long term demand for infection prevention products and services, supported by recurring revenue and disciplined capital deployment. The latest option exercise modestly increases insider equity exposure but does not materially change near term catalysts around cash flow resilience or the key risk of rising input costs and healthcare customer budget pressure.

The most relevant recent announcement here is STERIS’s US$500 million share repurchase program, with about US$424.3 million already deployed by March 31, 2026. Ongoing buybacks, combined with consistent dividends, highlight management’s focus on shareholder returns, which sits against the ongoing debate about cash flow strength, spending requirements and how much tariff and reimbursement pressure the business can absorb.

Yet while cash generation and capital returns look supportive today, investors should still be aware of rising tariff exposure and potential margin pressure if...

Read the full narrative on STERIS (it's free!)

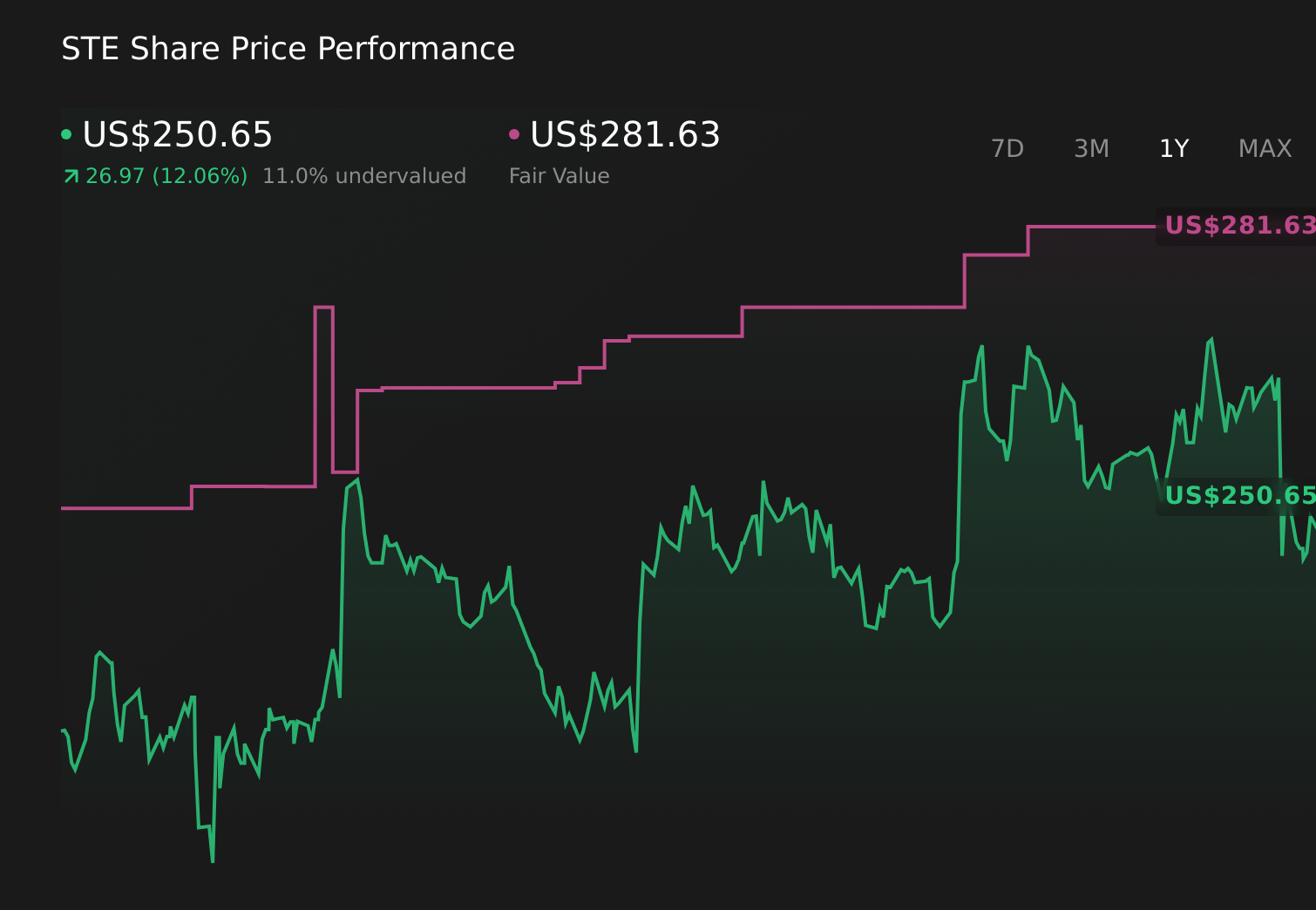

STERIS' narrative projects $7.2 billion revenue and $1.1 billion earnings by 2029. This requires 6.6% yearly revenue growth and about a $0.3 billion earnings increase from $782.3 million.

Uncover how STERIS' forecasts yield a $256.86 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates for STERIS cluster between US$230 and about US$256.86 per share, showing that individual views can spread across a wide band. You should weigh these against the risk that higher metal tariffs and healthcare reimbursement pressure could compress margins and alter how the market values STERIS over time, and explore how other investors frame those trade offs.

Explore 3 other fair value estimates on STERIS - why the stock might be worth just $230.00!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your STERIS research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free STERIS research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate STERIS' overall financial health at a glance.

Looking For Alternative Opportunities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com