- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

CNB Financial (CCNE) On Shelf Filing And Capital Flexibility Looks Cheap, But Questions Remain

CNB Financial (CCNE) recently filed an omnibus shelf registration that covers common and preferred stock, depositary shares, and debt securities, a move that matters for how the bank might fund future plans.

See our latest analysis for CNB Financial.

CNB Financial's shelf registration lands at a time when the share price has climbed 9.5% over the past month and 30.9% year to date. The 1 year total shareholder return of 41.7% and 3 year total shareholder return of about 2.1x signal that momentum has been building over a longer horizon and that investors have been rewarding the stock beyond price moves alone.

If this kind of capital raising flexibility has caught your attention, it can be a good moment to broaden your search and check out 20 top founder-led companies

With CNB Financial’s stock up sharply over multiple time frames and trading only slightly below analyst price targets, the key question is whether its valuation still leaves meaningful upside or whether the market is already pricing in future growth.

Preferred P/E of 12.9x: Is it justified?

On the numbers available, CNB Financial’s current valuation screens as inexpensive, with a P/E of 12.9x alongside indicators that suggest the market is not fully pricing in its earnings profile.

The P/E ratio compares the share price to earnings per share and is a common way to see how much investors are paying for current profits. For a bank like CNB Financial, where earnings and balance sheet strength are central, the P/E helps you judge how the stock is being weighed against both its own history and the broader sector.

Here, the stock is flagged as good value on several fronts. The 12.9x P/E is below the estimated fair P/E of 14.7x. This points to some room for the valuation to move closer to that level if the market reassesses what it is willing to pay for CNB Financial’s earnings. At the same time, the P/E is identified as slightly expensive relative to the US Banks industry average of 12.4x. This suggests investors are already paying a small premium versus peers even though the stock is still assessed as good value versus the fair ratio benchmark.

Explore the SWS fair ratio for CNB Financial

Result: Price-to-Earnings of 12.9x (UNDERVALUED)

However, CNB Financial’s recent share price momentum, along with the possibility of future equity or debt issuance, could both limit upside and introduce dilution risk for existing shareholders.

Find out about the key risks to this CNB Financial narrative.

Another view on CNB Financial’s value

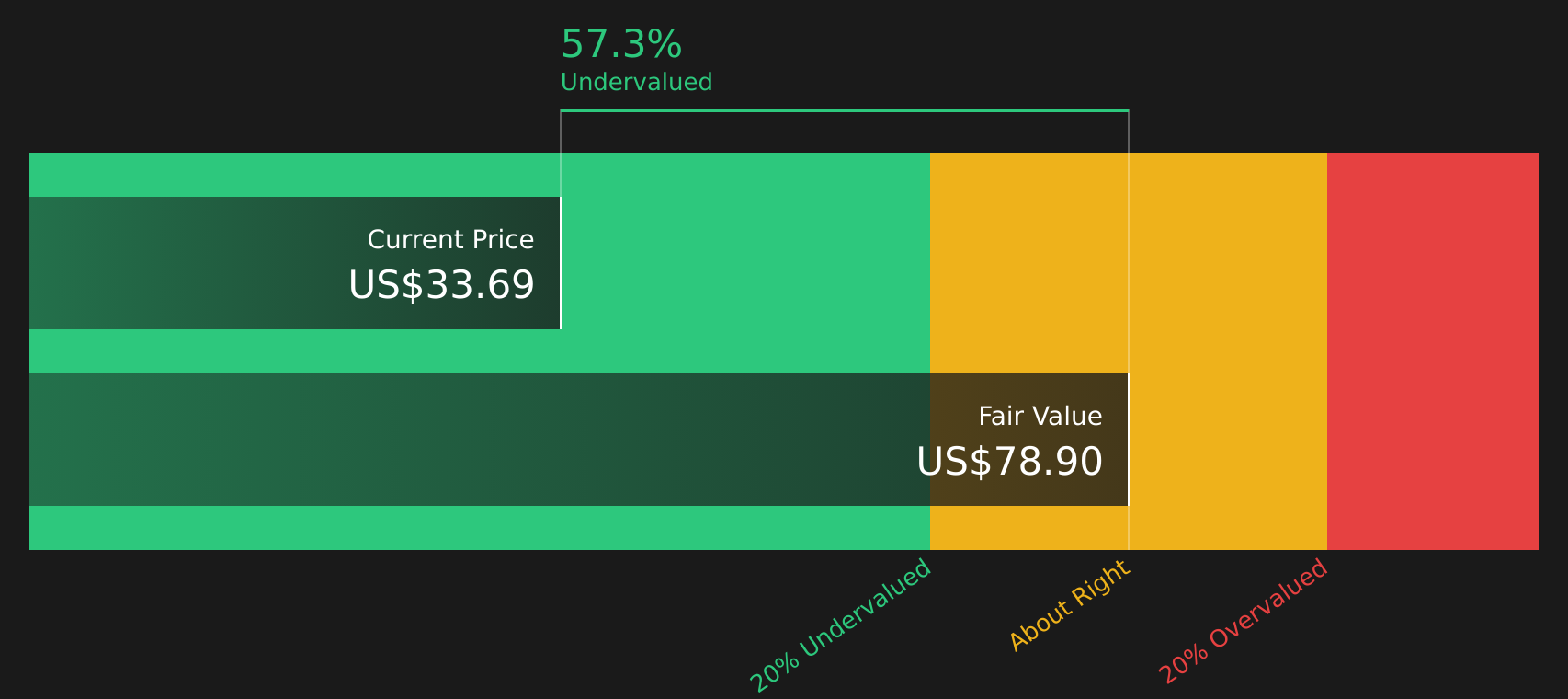

The P/E suggests CNB Financial looks inexpensive, but the SWS DCF model paints an even starker picture, with the stock at $33.69 versus an estimated future cash flow value of $78.90, implying it is trading 57.3% below that fair value estimate.

If one method flags CNB Financial as cheap and another calls it deeply undervalued, an investor may want to consider how much weight to place on any single valuation yardstick.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out CNB Financial for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With CNB Financial presenting both clear risks and appealing rewards, it is worth checking the data for yourself and deciding where you stand. To see the full balance of possible upsides and concerns in one place, review the 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond CNB Financial?

If CNB Financial has sharpened your focus on valuation and risk, do not stop here. Broaden your watchlist with targeted stock ideas built from the same data-driven approach.

- Zero in on quality at a discount by scanning 43 high quality undervalued stocks that combine attractive pricing with solid fundamentals.

- Strengthen your income stream by reviewing 7 dividend fortresses that emphasize higher yields with a focus on resilience.

- Prioritize stability and staying power by checking solid balance sheet and fundamentals stocks screener (46 results) that highlight companies with stronger financial footing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com