- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Air Products (APD) Is Up 12.2% After Axing U.S. Projects, Pivoting to NEOM Ammonia Deal

- In late June 2026, Air Products and Chemicals said it would stop the Louisiana Clean Energy Complex, a zero-carbon liquid hydrogen facility in Arizona, and several smaller clean energy projects, taking up to US$2.90 billion in pre-tax charges mainly for asset write-downs and contract terminations, while also pursuing other portfolio adjustments.

- At the same time, Air Products and Chemicals moved to finalize a global marketing and distribution agreement with Yara International ASA for renewable ammonia from the NEOM Green Hydrogen Project in Saudi Arabia, indicating a shift toward larger-scale opportunities where Yara’s global supply chain can help unlock demand.

- Next, we’ll examine how exiting the Louisiana Clean Energy Complex reshapes Air Products’ investment narrative and long-term clean energy focus.

Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

Air Products and Chemicals Investment Narrative Recap

To own Air Products and Chemicals, you need to believe that large, long-term hydrogen and clean ammonia projects can translate into durable earnings, while the company keeps tight control of capital spending. Exiting the Louisiana Clean Energy Complex and related projects sharpens that focus but also concentrates attention on the execution risk and cash flow timing of remaining megaprojects like NEOM, which is arguably the key near term catalyst and the biggest operational risk right now.

The most relevant recent announcement is Air Products’ decision to discontinue the Louisiana Clean Energy Complex and other smaller hydrogen projects, taking up to US$2,900 million in pre tax charges. This move directly affects how investors think about future capital intensity, potential write downs and the pace at which capital in process might convert into productive, earnings generating assets.

Yet with capital in process already weighing on returns and big projects still ahead, investors should be aware of how quickly those investments start to...

Read the full narrative on Air Products and Chemicals (it's free!)

Air Products and Chemicals' narrative projects $15.4 billion revenue and $3.7 billion earnings by 2029. This requires 7.3% yearly revenue growth and about a $1.6 billion earnings increase from $2.1 billion today.

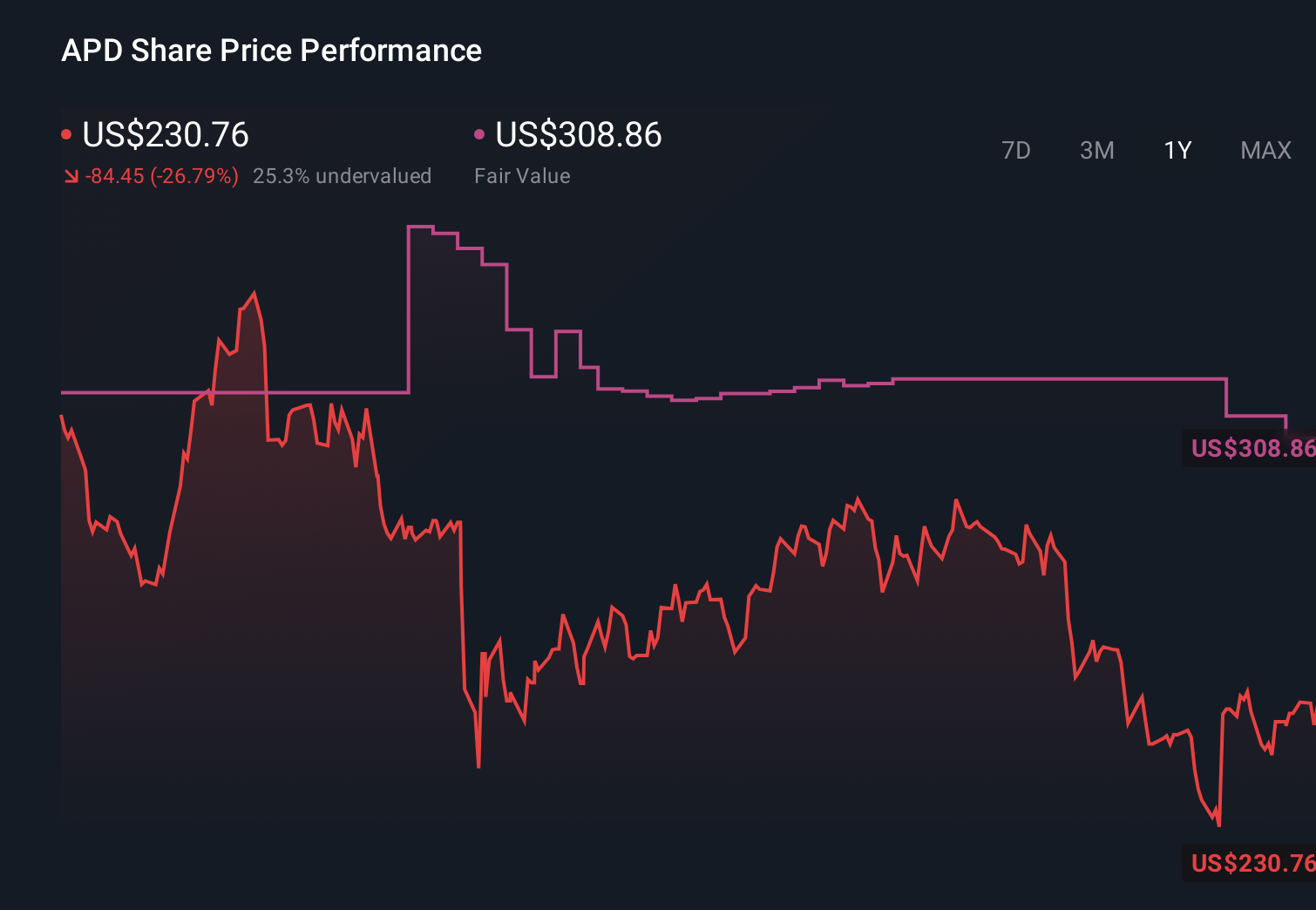

Uncover how Air Products and Chemicals' forecasts yield a $327.86 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community place Air Products’ fair value between US$229 and US$328 per share, underscoring a wide spread of expectations. Against that backdrop, the recent exit from LCEC and other clean energy projects puts even more focus on how effectively future hydrogen and ammonia investments might translate into returns, so it can be worth weighing several of these different views before forming your own.

Explore 3 other fair value estimates on Air Products and Chemicals - why the stock might be worth 27% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Air Products and Chemicals research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Air Products and Chemicals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Air Products and Chemicals' overall financial health at a glance.

Searching For A Fresh Perspective?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com