- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Did Copay Allegations and New Director Equity Awards Just Shift Tarsus Pharmaceuticals' (TARS) Investment Narrative?

- In late June 2026, short seller Culper Research disclosed a short position in Tarsus Pharmaceuticals and alleged concerns over the company’s Medicare copay practices, while shareholders at the June 25, 2026 annual meeting re-elected Class III directors, approved executive pay on an advisory basis, and ratified Ernst & Young LLP as auditor.

- A series of new equity awards to non-employee directors, vesting over time and tied to continued board service, underscores Tarsus’s emphasis on aligning director incentives with longer-term shareholder interests as regulatory and reimbursement-related questions emerge.

- We’ll now examine how Culper Research’s Medicare copay allegations and the new director equity awards may influence Tarsus’s existing investment narrative.

We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Tarsus Pharmaceuticals Investment Narrative Recap

To own Tarsus today, you generally need to believe XDEMVY can sustain broad adoption while the pipeline adds meaningful, diversified revenue over time. The Culper Research short report on Medicare copay practices squarely targets reimbursement risk, which already sits at the center of the story, but it does not clearly alter the near term commercial catalyst around XDEMVY’s uptake until regulators or payers respond in a concrete way.

The most relevant development here is the June 25, 2026 director equity awards, which tie non employee director compensation to the share price and continued board service over the next year. For investors watching the Medicare copay allegations, this structure can focus attention on how the board oversees reimbursement, compliance, and payer relationships at a time when gross to net pressures are already a key concern.

Yet investors should also weigh the risk that heightened scrutiny of drug pricing and Medicare support programs could...

Read the full narrative on Tarsus Pharmaceuticals (it's free!)

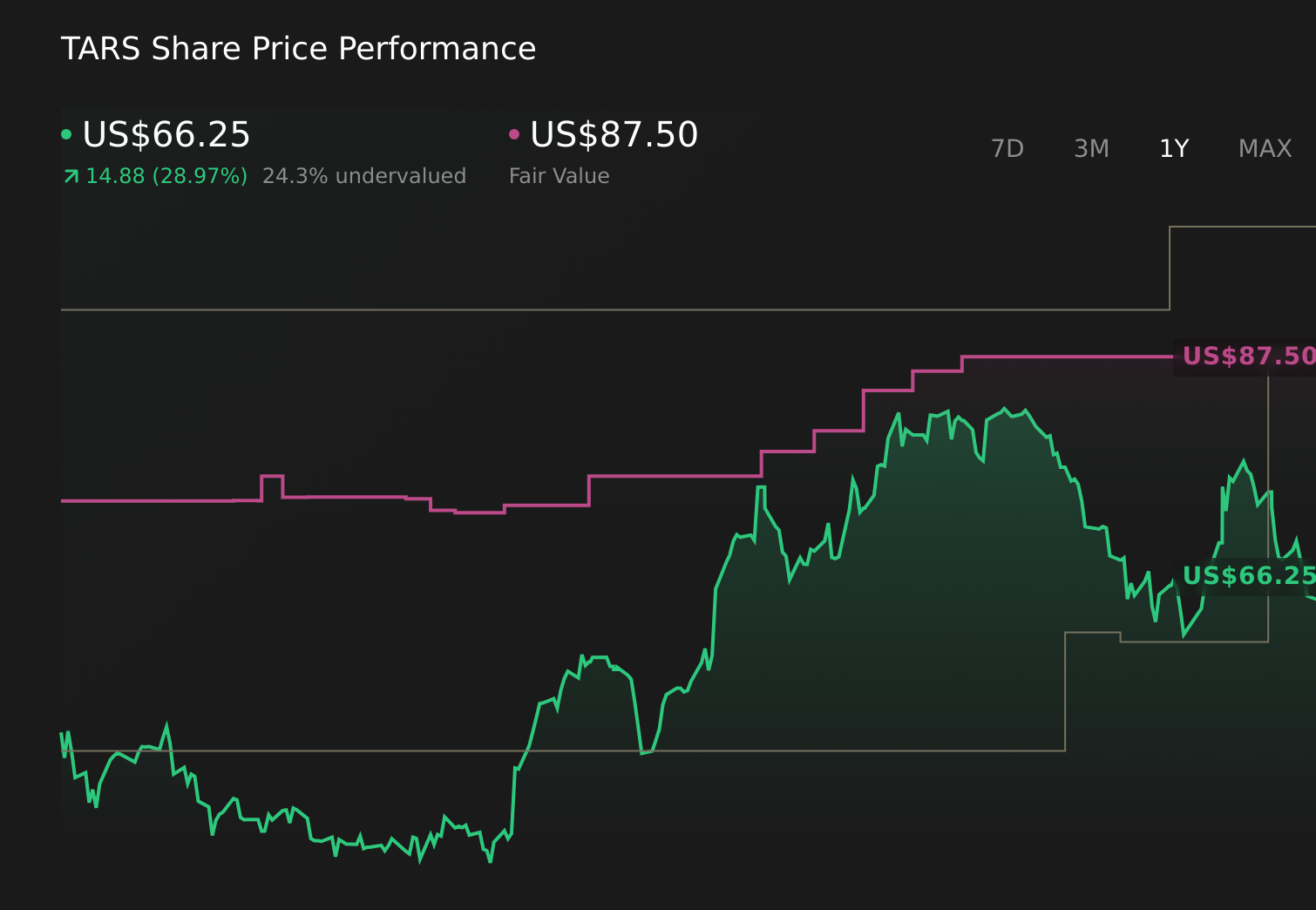

Tarsus Pharmaceuticals' narrative projects $1.1 billion revenue and $632.5 million earnings by 2029. This requires 28.3% yearly revenue growth and about a $681 million earnings increase from -$48.3 million today.

Uncover how Tarsus Pharmaceuticals' forecasts yield a $94.11 fair value, a 44% upside to its current price.

Exploring Other Perspectives

Before Culper’s report, the most optimistic analysts were modeling about US$1.4 billion of 2029 revenue and US$473.5 million of earnings, which sits in sharp contrast to the reimbursement and pricing pressure risks that could meaningfully alter those expectations once this new controversy is fully reflected in forecasts.

Explore 4 other fair value estimates on Tarsus Pharmaceuticals - why the stock might be worth over 5x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Tarsus Pharmaceuticals research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Tarsus Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Tarsus Pharmaceuticals' overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com