- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Kinsale Capital Group (KNSL) Could Be 36% Undervalued On Russell Value Index Shift

Kinsale Capital Group (KNSL) has just been shifted across the Russell style spectrum, removed from several growth benchmarks and added to multiple value and value defensive indices, a change that can directly influence index-linked fund flows.

See our latest analysis for Kinsale Capital Group.

The reclassification comes as Kinsale Capital Group’s share price has rebounded in the short term, with a 7 day share price return of 15.05% and a 30 day share price return of 20.13%. However, the year to date share price return is down 9.58% and the 1 year total shareholder return is down 25.30%. Recent momentum is therefore improving but sits against weaker longer term performance.

If this shift in style category has you reassessing where to find potential opportunities, it can help to broaden the search and uncover 20 top founder-led companies

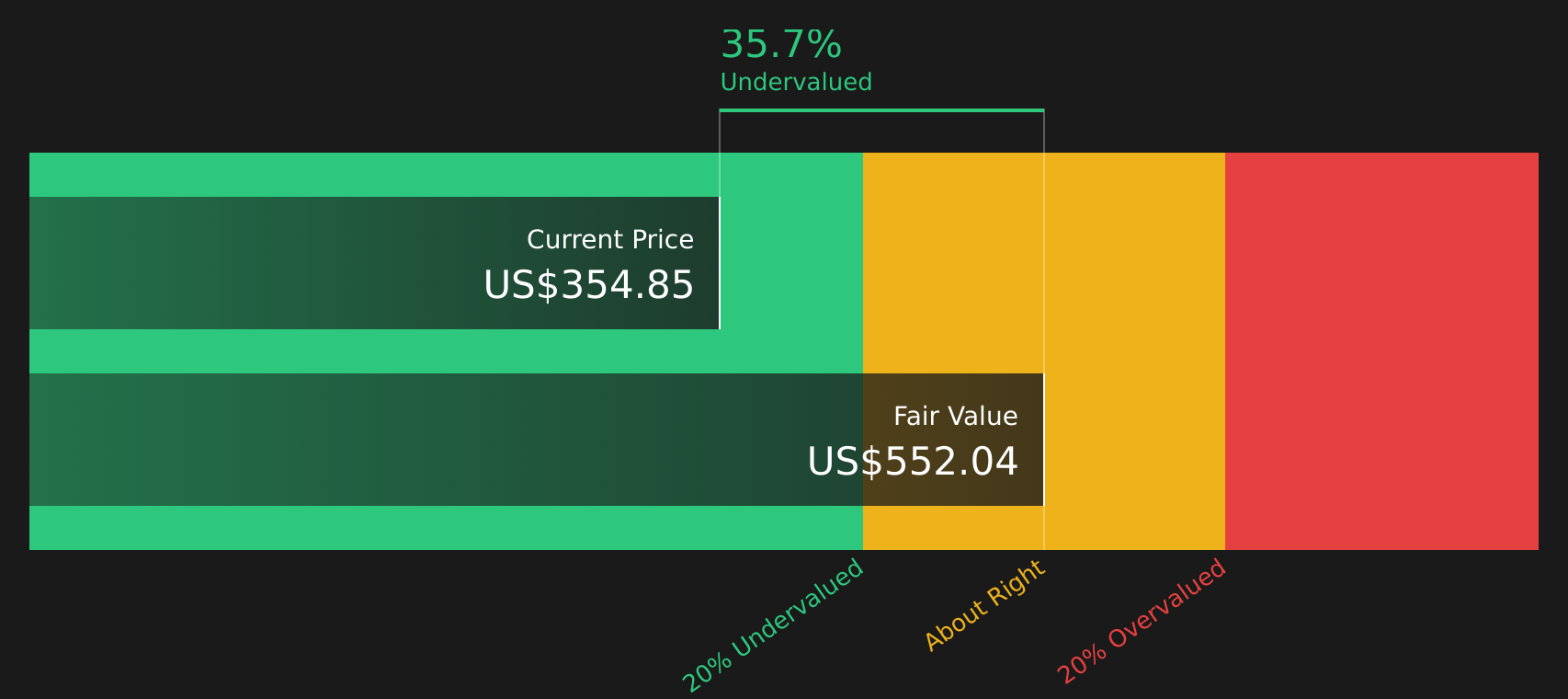

With Kinsale Capital Group now grouped with value stocks and trading at a 35.72% discount to one intrinsic value estimate, yet sitting slightly above the average analyst price target, are you looking at a genuine value opportunity or a market that is already pricing in future growth?

Most Popular Narrative: 10% Overvalued

The most followed narrative for Kinsale Capital Group compares a fair value of $354.67 to a last close of $354.85. This suggests the stock sits slightly above that reference point and rests on a detailed long term earnings story.

The secular shift of risks from standard markets into the E&S channel, particularly for homeowners and catastrophe-exposed lines (e.g., in California, Texas, and coastal regions), is broadening Kinsale's long-term premium base and enabling sustainable top-line growth even as competition intensifies in select lines.

Curious what powers that fair value? The narrative leans on measured revenue expansion, slightly thinner profit margins, and a future earnings multiple above the broader insurance sector. The exact mix behind those assumptions is where the story gets interesting.

Result: Fair Value of $354.67 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the Kinsale Capital Group story could shift quickly if competition further erodes premium growth or if catastrophe exposed lines produce larger than expected losses.

Find out about the key risks to this Kinsale Capital Group narrative.

Another View on Kinsale Capital Group's Valuation

The first narrative suggests Kinsale Capital Group looks about 10% overvalued against a $354.67 fair value. Our DCF model tells a different story, with a future cash flow value of $552.04, implying the current $354.85 price sits well below that estimate. Which set of assumptions do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Kinsale Capital Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 42 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seeing mixed signals around Kinsale Capital Group's valuation and risk reward trade off? Act quickly. Review the underlying data and assess the balance of 2 key rewards and 1 important warning sign

Looking for more investment ideas beyond Kinsale Capital Group?

If Kinsale Capital Group has sharpened your thinking, do not stop there. Use the screener to spot other stocks that could fit your portfolio before others notice.

- Target long term compounding potential by reviewing companies on the 42 high quality undervalued stocks that combine quality fundamentals with prices below one estimate of fair value.

- Strengthen income potential by scanning for reliable payers in the 7 dividend fortresses that may align with your yield and stability goals.

- Prioritise resilience by focusing on companies in the 75 resilient stocks with low risk scores that appear to pair steadier profiles with measured risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com