- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Why Vestis (VSTS) Is Up 8.8% After Raising EBITDA Outlook on Transformation Progress – And What's Next

- Vestis Corp recently reported that its second-quarter adjusted EBITDA rose about 19% year over year to approximately US$75 million, marking its first earnings growth in more than two years and prompting an increase in full‑year fiscal 2026 EBITDA and free cash flow guidance.

- This improvement was driven by progress on its Business Transformation Plan, including better on‑time delivery, higher plant productivity, and a lower cost per pound, which collectively signal early traction in reshaping the company’s operational profile.

- Now we’ll explore how this improved EBITDA performance and upgraded full‑year guidance could influence Vestis’s earlier, more cautious investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Vestis Investment Narrative Recap

To own Vestis, you need to believe its Business Transformation Plan can offset soft demand and stabilize a still-fragile revenue base. The latest 19% year over year adjusted EBITDA increase and higher fiscal 2026 guidance support the near term catalyst of improving profitability, but they do not eliminate the key risk that customer churn, pricing pressure, and revenue declines could persist, especially with management still calling for flat to slightly down sales this year.

Against this backdrop, the recent appointment of Steve Cochran as Executive Vice President, Chief Commercial and Supply Chain Officer stands out. With more than three decades in apparel, uniform, and business services, his remit across both commercial and supply chain functions directly links to the transformation efforts that helped drive better on time delivery, higher plant productivity, and lower cost per pound, making execution on retention and margin recovery a critical area to watch.

Yet behind the improved EBITDA and upgraded free cash flow guidance, investors should still be aware of the risk that concentrated customer losses and elevated leverage could...

Read the full narrative on Vestis (it's free!)

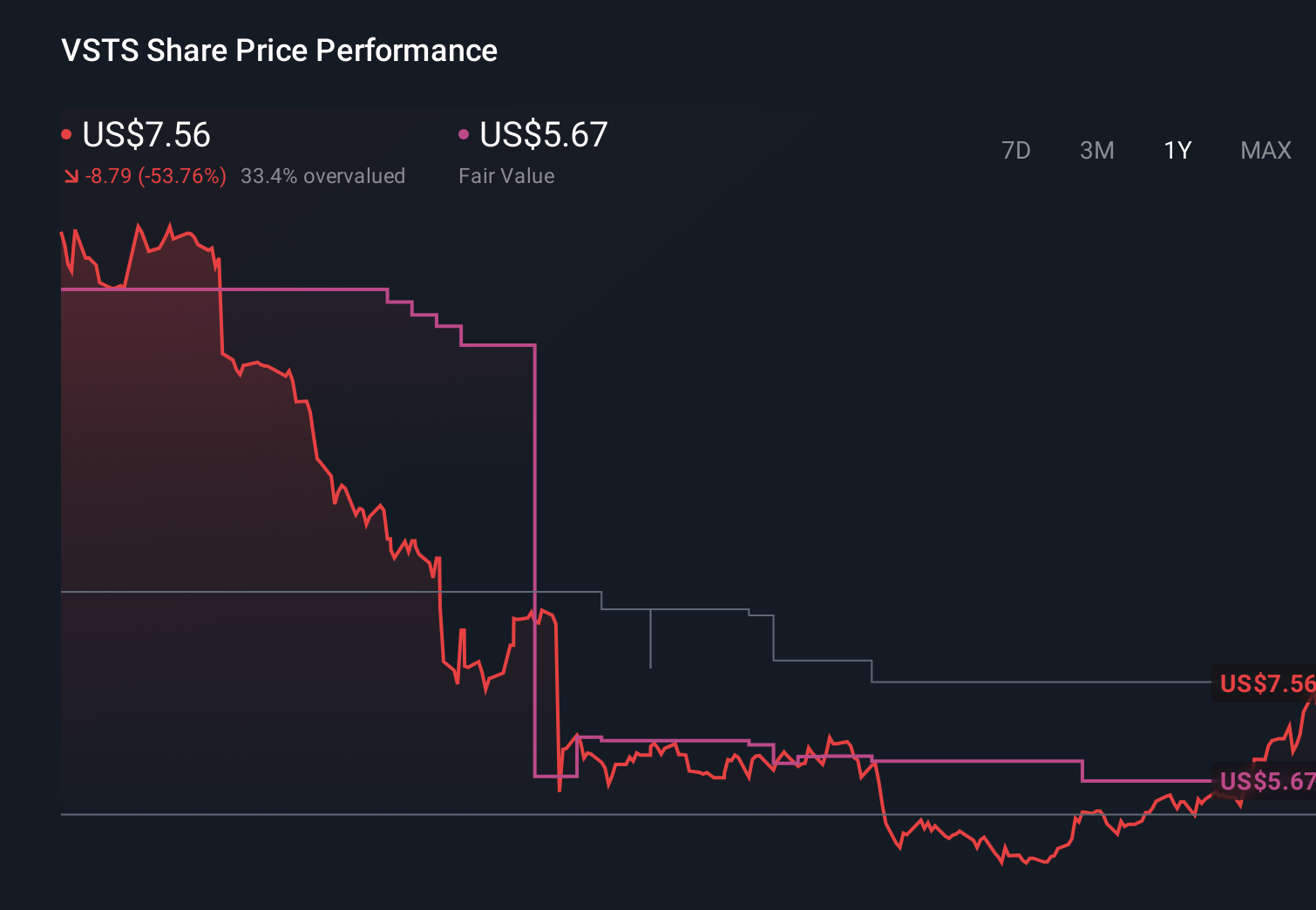

Vestis' narrative projects $2.8 billion revenue and $110.4 million earnings by 2029. This requires fairly flat yearly revenue growth and about a $127.4 million earnings increase from -$17.0 million today.

Uncover how Vestis' forecasts yield a $10.16 fair value, a 31% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming Vestis could reach about US$2.9 billion in revenue and roughly US$125 million in earnings by 2029, which is a far brighter path than the baseline view that focuses on customer churn and debt constraints; after this EBITDA surprise, you now have to weigh whether that bullish scenario, and the risk of further customer attrition highlighted in earlier research, still feels too optimistic or perhaps closer to where the story may be heading.

Explore another fair value estimate on Vestis - why the stock might be worth just $14.00!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Vestis research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vestis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vestis' overall financial health at a glance.

Curious About Other Options?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com