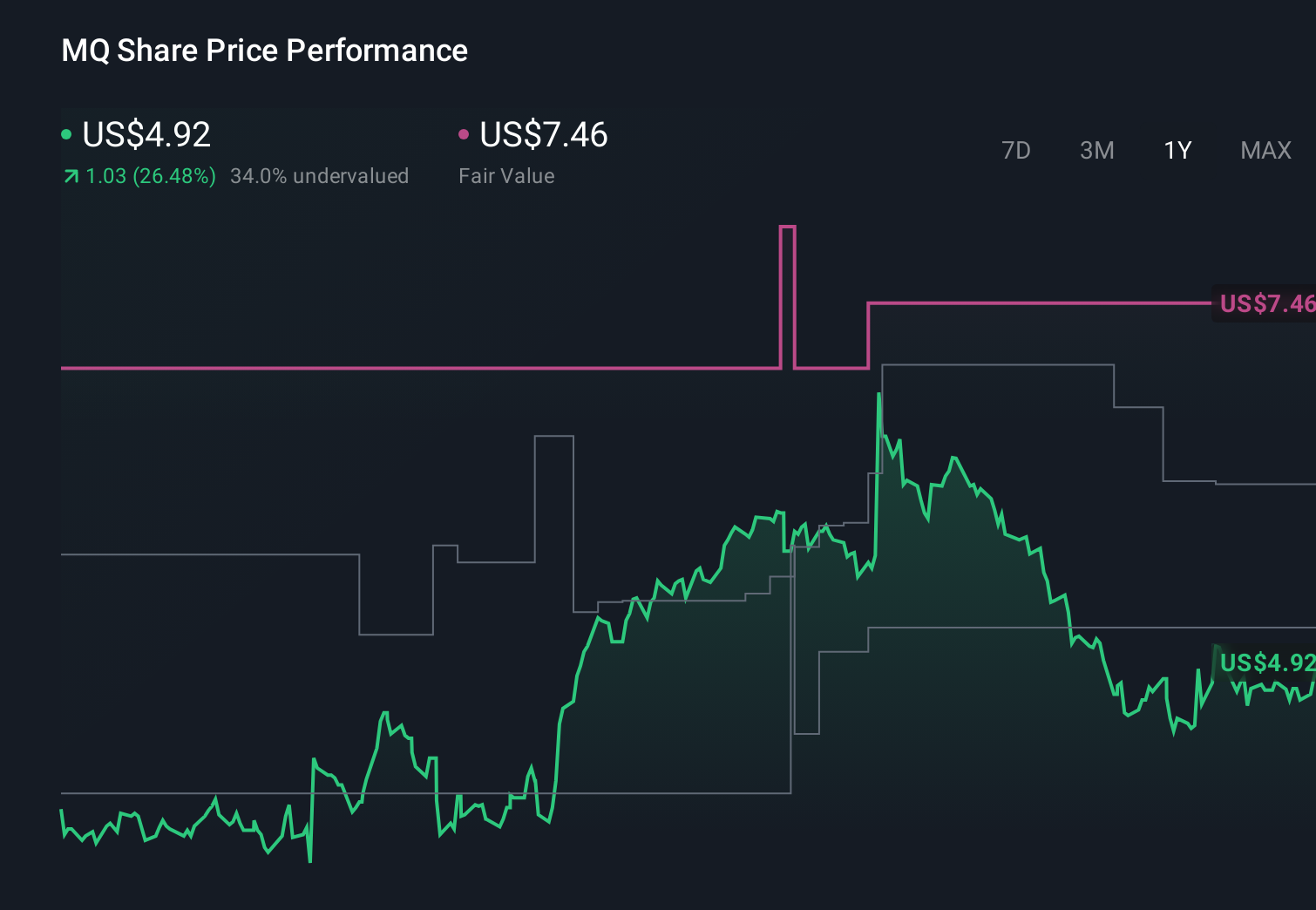

- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Does Marqeta’s Reverse Split and Index Shuffle Reframe Its Global Payments Ambitions for MQ Investors?

- Marqeta, Inc. has completed a 1-for-4 reverse stock split of its Class A and Class B Common Stock and Preferred Stock, with shares beginning to trade on a split-adjusted basis on Nasdaq under the ticker "MQ" on July 1, 2026.

- At the same time, Marqeta was removed from several Russell value benchmarks but added to the Russell 2000 Defensive and Growth-Defensive indices, signaling a shift in how the company is classified by index providers and some institutional investors.

- Now we’ll examine how Marqeta’s reverse stock split could influence its previously outlined investment narrative around global payments expansion.

The latest GPUs need a type of rare earth metal called Terbium and there are only 31 companies in the world exploring or producing it. Find the list for free.

Marqeta Investment Narrative Recap

To own Marqeta, you need to believe its card issuing platform can keep riding global digital payments and embedded finance adoption, despite customer concentration and rising competition. The reverse split and index reshuffle do not materially change those fundamentals in the near term, but they may influence short term trading flows, which could amplify the impact of any news around key clients or regulatory shifts.

The recent expansion of Marqeta’s account and money movement tools into 30 additional European countries through its Banking Circle collaboration ties directly into its payments expansion story. This move supports the existing catalyst of international growth and broader embedded finance use cases, while also testing the risk that card based models could be pressured over time by alternative payment rails and regional regulatory requirements.

However, investors should also be aware that concentration in a small number of large customers means that...

Read the full narrative on Marqeta (it's free!)

Marqeta's narrative projects $969.2 million revenue and $73.1 million earnings by 2029. This requires 14.2% yearly revenue growth and a $70.9 million earnings increase from $2.2 million today.

Uncover how Marqeta's forecasts yield a $5.24 fair value, a 69% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming revenue of about US$941.4 million and only 3.7 percent margins by 2029, which contrasts with the more optimistic view that Marqeta’s diversification and value added services could ease its dependence on Block and other large clients, and the latest reverse split and index changes may push both narratives to be revisited.

Explore 3 other fair value estimates on Marqeta - why the stock might be worth less than half the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Marqeta research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Marqeta research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Marqeta's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com