- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Will Index Additions and New Offshore Awards Change TechnipFMC's (FTI) Narrative?

- In late June 2026, TechnipFMC was added to multiple Russell growth, value, and defensive indices while also securing two offshore contracts worth between US$75,000,000 and US$1.00 billion across North Sea and Angola projects.

- These index inclusions and sizable awards broaden TechnipFMC’s investor visibility and reinforce its position as a key provider for complex subsea developments.

- We’ll now examine how the large North Sea integrated contract reshapes TechnipFMC’s investment narrative and future project pipeline outlook.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

TechnipFMC Investment Narrative Recap

To own TechnipFMC, you need to believe in a long-lived offshore and subsea project cycle that supports its order book and margins. The key near term catalyst is continued Subsea order momentum, while a major risk remains exposure to oil and gas spending cycles and longer term decarbonization. The new Russell index inclusions and June contract wins modestly reinforce visibility around that order story but do not fundamentally change the central risk around future fossil-fuel project demand.

The most relevant update here is the “large” integrated iEPCI award from Vår Energi in the North Sea, valued between US$500,000,000 and US$1,000,000,000. This contract adds scale to TechnipFMC’s backlog and directly ties into the consensus catalyst of integrated offshore awards supporting Subsea revenue guidance, while also concentrating execution and commodity cost risk in a single, complex multi-year project.

Yet even with these contract wins, investors should be aware of how margin pressure from volatile input costs could...

Read the full narrative on TechnipFMC (it's free!)

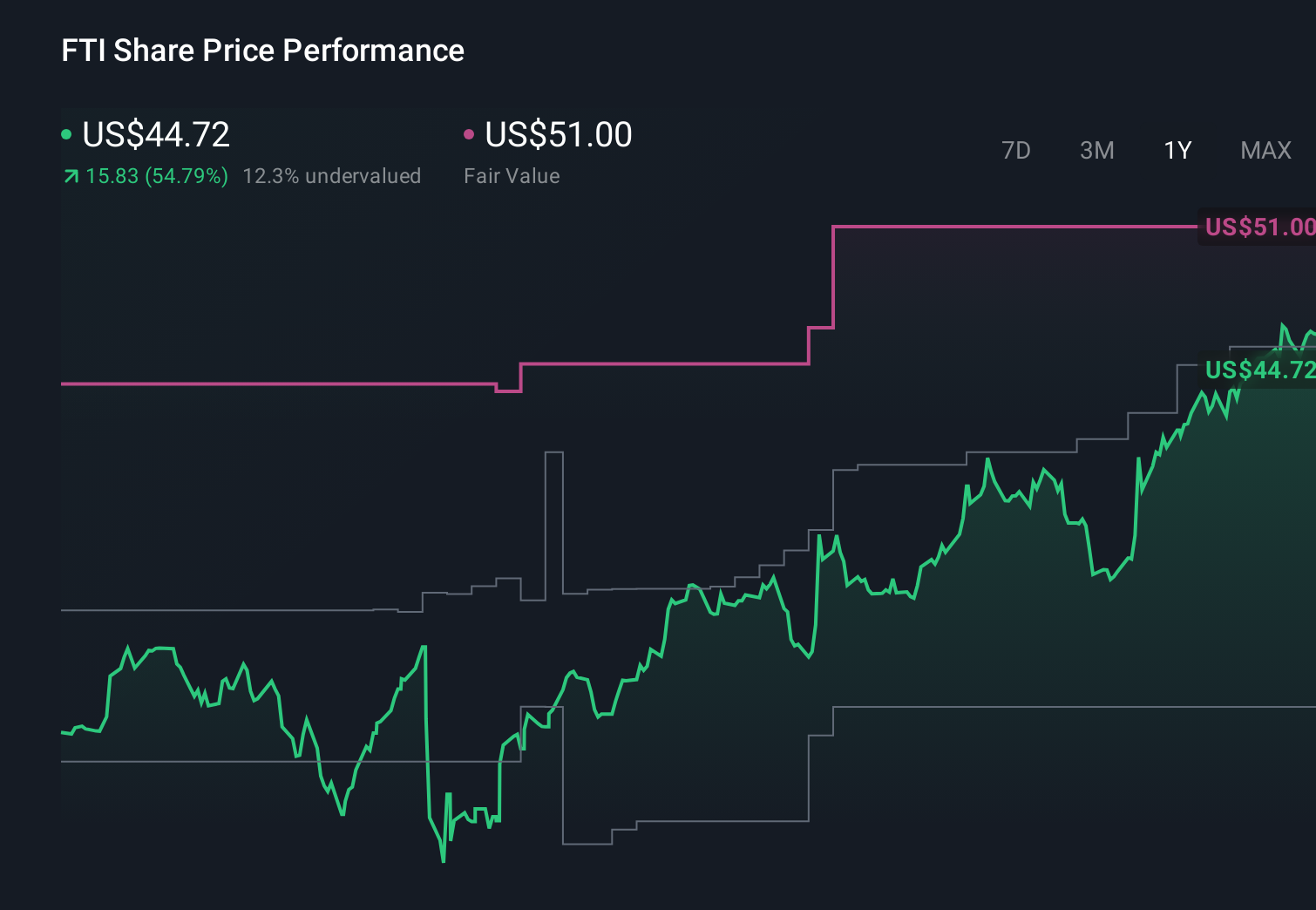

TechnipFMC's narrative projects $12.1 billion revenue and $1.4 billion earnings by 2029. This requires 5.9% yearly revenue growth and roughly a $0.3 billion earnings increase from $1.1 billion today.

Uncover how TechnipFMC's forecasts yield a $76.00 fair value, a 17% upside to its current price.

Exploring Other Perspectives

By contrast, the most pessimistic analysts worried that volatile commodity prices could squeeze subsea margins, even as they expected revenue of about US$10.5 billion and earnings near US$936 million before this news. Their view highlights how opinions can differ sharply, and why you may want to compare these more cautious assumptions with how new index inclusions and fresh offshore awards could eventually reshape both the risk and the opportunity.

Explore 5 other fair value estimates on TechnipFMC - why the stock might be worth just $75.81!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your TechnipFMC research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free TechnipFMC research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate TechnipFMC's overall financial health at a glance.

No Opportunity In TechnipFMC?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com