- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is Primerica (PRI) A Bargain After Its Index Removal And Credit Facility Extension?

Index removal puts Primerica stock back in focus

Primerica (PRI) has come back onto investor radar after its recent removal from the Russell 1000 Dynamic Index, alongside news that the company extended a US$200,000,000 unsecured revolving credit facility to 2031.

See our latest analysis for Primerica.

The latest moves around the Russell 1000 Dynamic Index and the extended credit facility come against a backdrop of stronger momentum in Primerica’s stock, with a 1 month share price return of 9.39% and a 3 year total shareholder return of 55.02%.

If this kind of steady compounding interests you, it can be worth widening your search and seeing what stands out in our 20 top founder-led companies

Primerica’s recent index exit, solid long term shareholder returns and sizeable intrinsic discount estimate raise a familiar question for investors: is this stock still trading below what it is worth, or is the market already pricing in future growth?

Most Popular Narrative: 2.3% Undervalued

Primerica's most followed valuation narrative pegs fair value at $298.50, slightly above the last close at $291.63, which puts more weight on long term cash generation than short term price moves.

Strong demographic drivers, especially the large cohort of Baby Boomers and Gen X approaching retirement, are fueling sustained demand for retirement planning products, annuities, and investment solutions, providing a multi-year tailwind for Primerica's ISP segment and supporting double-digit sales growth, which should boost top-line revenue and client assets.

Analysts are anchoring this fair value on measured revenue growth, firm profit margins, and a future earnings multiple that edges above the broader insurance sector. Curious which assumptions matter most, and how they link back to that $298.50 figure.

Result: Fair Value of $298.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, investors still need to weigh risks such as pressure on new term life policy sales and higher operating expenses, which could challenge the current Primerica narrative.

Find out about the key risks to this Primerica narrative.

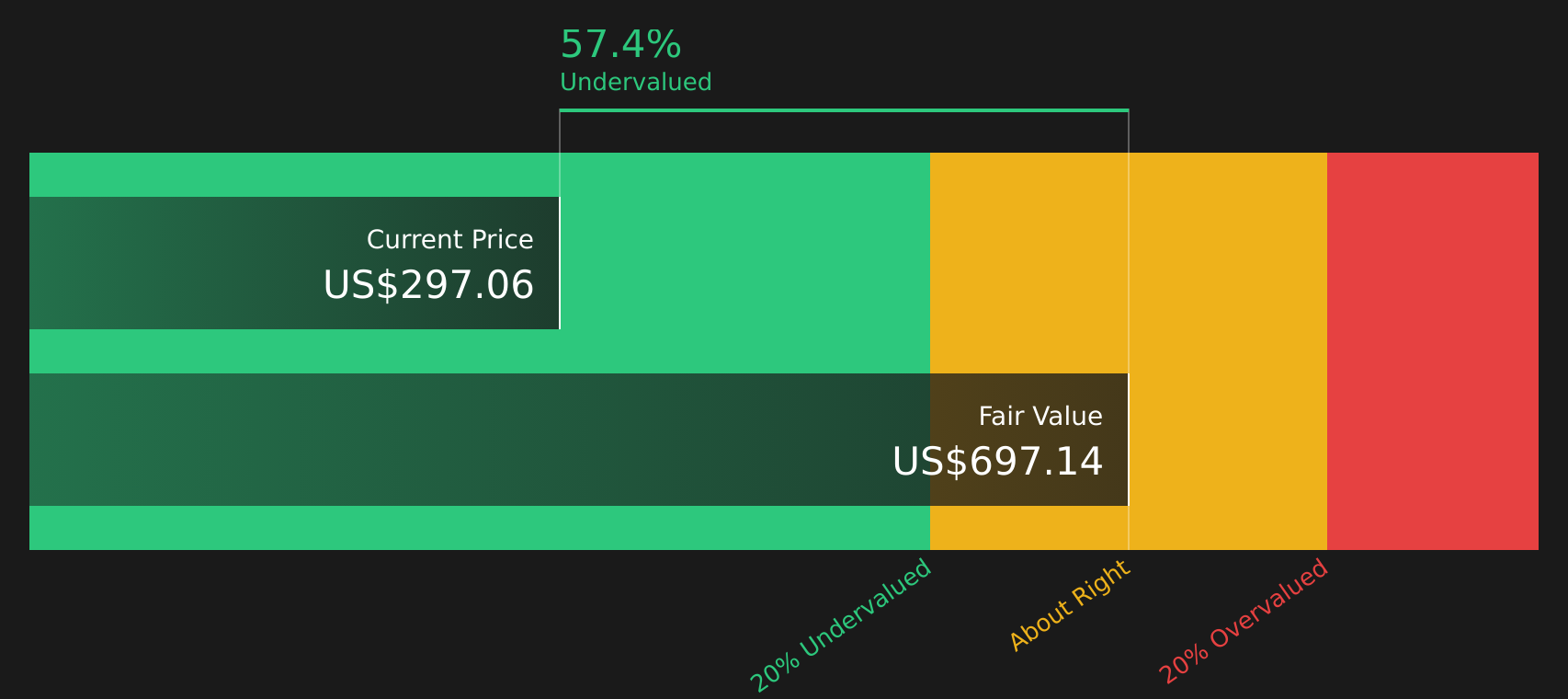

Another View on Primerica’s valuation

While the consensus fair value for Primerica sits close to the market price, our DCF model presents a very different picture, with an estimate of $697.14 per share compared with the current $291.63. That gap suggests a lot more optimism baked into cash flow assumptions, so which story do you trust?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With Primerica showing both potential rewards and flagged risks, it makes sense to move quickly and check the underlying data yourself rather than relying on headlines alone. To see how those positives and concerns stack up side by side, start with the 3 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Primerica?

If you are serious about building a stronger portfolio, do not stop at Primerica. Use the Simply Wall Street Screener to quickly surface fresh, data driven stock ideas.

- Spot potential mispricings early and review 41 high quality undervalued stocks that align with the kind of valuation edge you are seeking.

- Strengthen your portfolio’s foundation by scanning the solid balance sheet and fundamentals stocks screener (48 results) and focus on companies with financials that can handle tougher conditions.

- Aim to get ahead of the crowd with the screener containing 19 high quality undiscovered gems before these businesses move onto everyone else’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com