- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Starwood Property Trust (STWD) Launches Sustainable Notes, Is The Discount Too Wide?

Why Starwood Property Trust’s New Sustainable Notes Matter for Investors

Starwood Property Trust (STWD) has launched a private offering of US$500 million in unsecured senior notes due 2029, tying the proceeds to eligible green and social projects alongside refinancing existing debt.

This financing move sits at the intersection of balance sheet management and sustainability commitments. It gives investors fresh information on how the company may handle upcoming maturities, project funding and overall capital structure in the coming years.

See our latest analysis for Starwood Property Trust.

Starwood Property Trust’s latest sustainable note issuance comes after a period where the share price has eased, with a 1-month share price return down 4.10% and year-to-date share price return down 11.07%, while the 3-year total shareholder return of 13.91% points to a more resilient longer-term picture.

If this type of financing story has you thinking about where else capital is flowing, it could be a good time to scan opportunities in infrastructure and grid-linked plays using our 35 power grid technology and infrastructure stocks

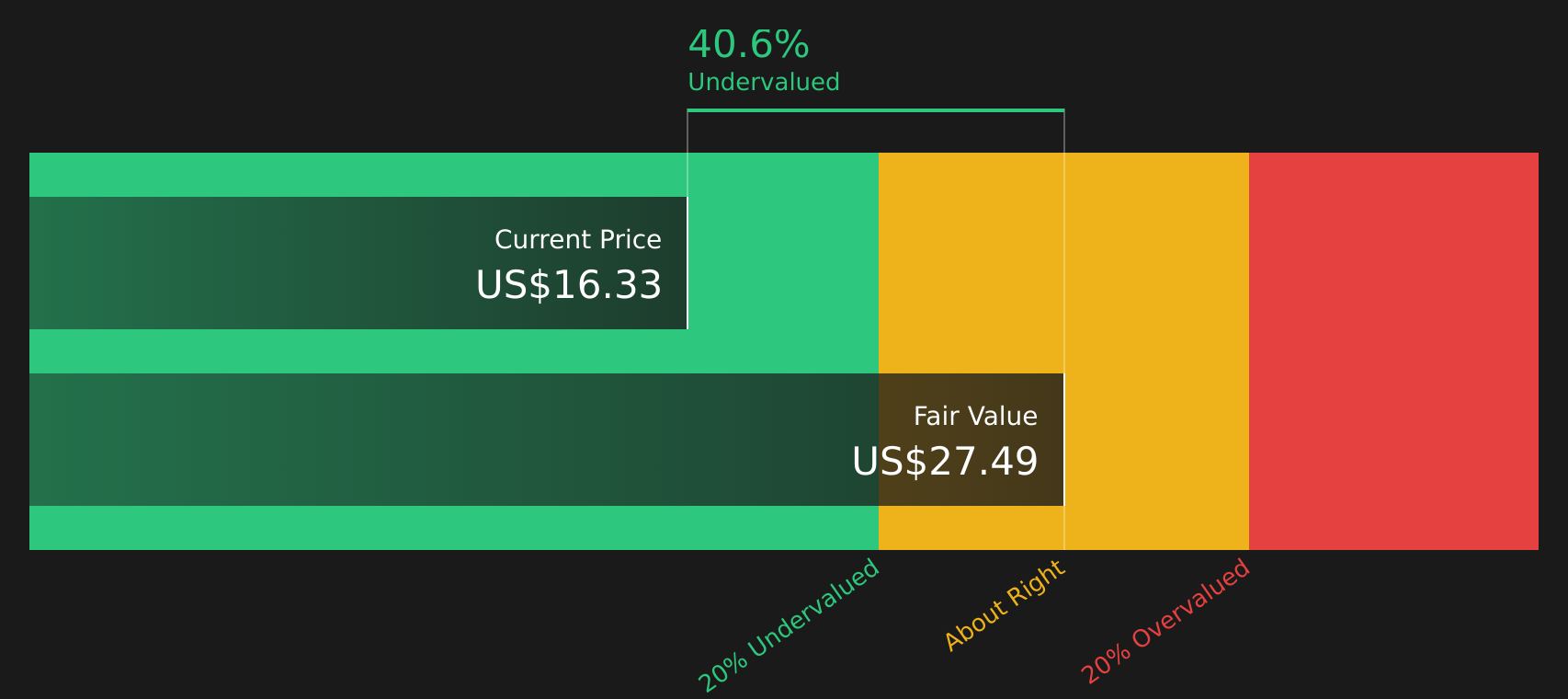

With Starwood Property Trust trading at US$16.38 and sitting at a sizeable discount to the US$20.25 analyst price target and an indicated intrinsic discount of 45.37%, investors have to ask whether there is genuine value here or whether the market is already weighing future risks and growth prospects.

Most Popular Narrative: 19.1% Undervalued

Against a last close of $16.38, the most widely followed narrative for Starwood Property Trust points to a fair value of $20.25, framing the sustainable notes within a broader earnings and valuation story.

Growing demand for alternative income from an aging population is expected to support strong, sustained appetite for mortgage REITs like Starwood, potentially lifting future revenue and share valuations as income-seeking investors expand allocations to the sector.

Curious what underpins that higher fair value for Starwood Property Trust? Revenue expansion, margin resets, and a future profit multiple all sit at the core of this narrative, with detailed assumptions that could surprise you.

Result: Fair Value of $20.25 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the bullish Starwood Property Trust story still depends on execution, with credit issues in commercial real estate and reliance on capital markets remaining key risks to watch.

Find out about the key risks to this Starwood Property Trust narrative.

Another View on Starwood Property Trust’s Valuation

The earlier story presents Starwood Property Trust as materially undervalued, with the current $16.38 price sitting 45.4% below an estimated fair value of $29.99 using the SWS DCF model. That represents a wide gap, so the key question is whether the cash flow assumptions behind it seem realistic to you or too optimistic.

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With mixed signals running through the Starwood Property Trust story, you may want to act now and weigh the upside and downside yourself using the 4 key rewards and 3 important warning signs

Looking for more investment ideas beyond Starwood Property Trust?

Before moving on, take a moment to broaden your watchlist with fresh ideas using the Simply Wall Street Screener, so you are not relying on just one stock story.

- Spot potential bargains early by checking companies that currently look mispriced on fundamentals through the 43 high quality undervalued stocks.

- Prioritize resilience and financial strength by scanning stocks filtered for robust balance sheets and solid fundamentals using the solid balance sheet and fundamentals stocks screener (48 results).

- Add a yield angle to your research by reviewing companies focused on income potential via the 10 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com