- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Entergy (ETR) Could Be 6% Below Fair Value Following Its Growth Narrative

Community engagement spotlight and why it matters for Entergy stock

Entergy (ETR) recently highlighted its role in the community as Chair and CEO Drew Marsh helped lead a United Way of Southeast Louisiana campaign that raised more than $7.7 million for local initiatives.

United Way recognized Entergy executive Michelle Delery with its Edward J. Krause Volunteer of the Year Award, underscoring the company’s broader employee participation in programs focused on education, financial stability and health across Southeast Louisiana.

See our latest analysis for Entergy.

Entergy’s share price has gained 22.37% year to date to US$114.86, with a 5.33% 1 month share price return and a 42.74% 1 year total shareholder return, pointing to building momentum over both shorter and longer periods.

If Entergy’s recent move has you thinking about where the next opportunity might come from, this is a good moment to scan 35 power grid technology and infrastructure stocks for ideas across the wider grid and infrastructure space.

With Entergy’s share price sitting at US$114.86 and recent returns running strong, the big question now is whether investors are still looking at an undervalued utility stock or if the market is already baking in future growth.

Most Popular Narrative: 6% Undervalued

Entergy’s most followed narrative puts fair value at $121.88 against the current $114.86 share price, framing the stock as modestly discounted on long term assumptions.

Capital investment of $40 billion over four years (with an expanded pipeline for renewables, grid modernization, and resilience upgrades) is expected to grow the company's rate base and support above-average EPS and earnings growth for several years.

Want to understand why this capital plan supports that fair value? The narrative leans on compounding revenue, wider margins, and a higher future earnings multiple.

Result: Fair Value of $121.88 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the Entergy narrative still hinges on smooth execution, with large Gulf South storm risks and heavy financing needs both capable of pressuring future assumptions.

Find out about the key risks to this Entergy narrative.

Another view on Entergy’s valuation

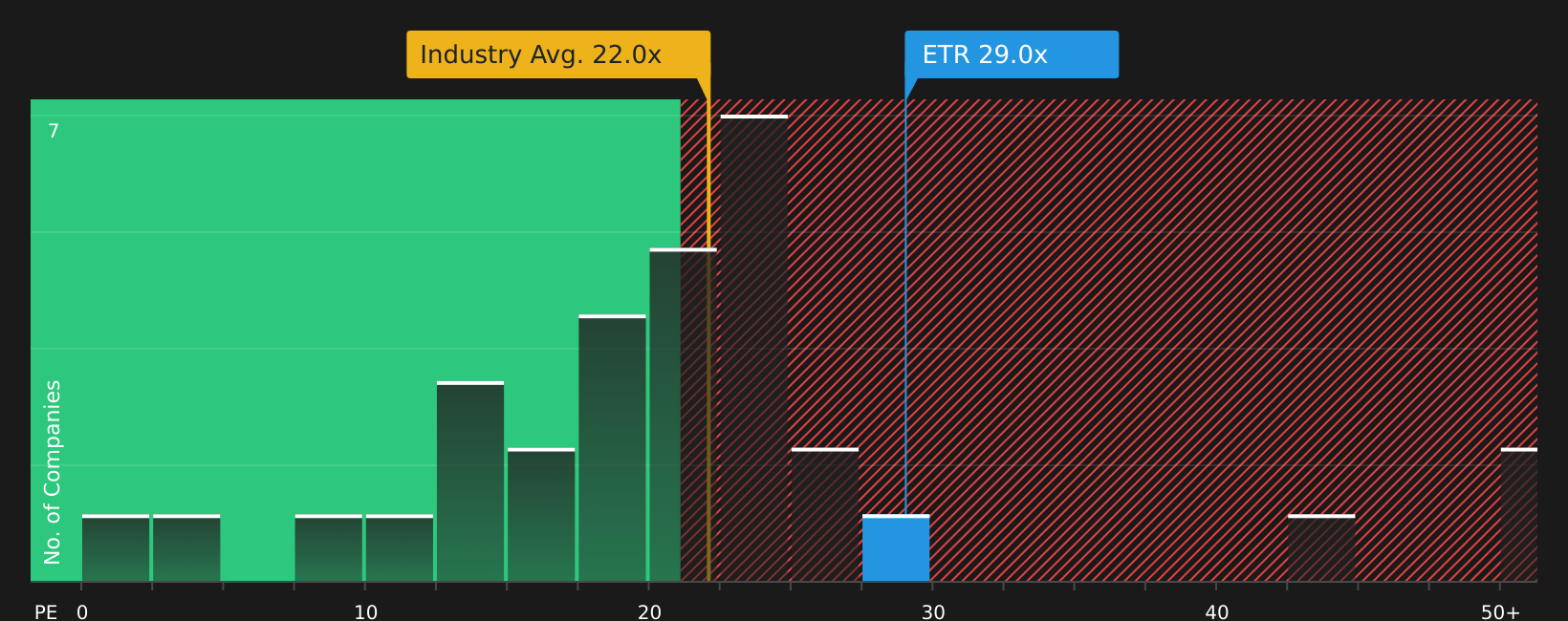

The fair value narrative suggests Entergy is about 6% undervalued at $121.88 versus the $114.86 share price, but the market is pricing the stock at a P/E of 29.5x. That is higher than the US Electric Utilities industry at 22.6x, peers at 18.6x, and above a fair ratio of 26.8x.

This gap points to a richer pricing profile that could limit how much room there is if sentiment cools, even if earnings keep progressing. For you, the question is whether current growth expectations justify paying more than both the sector and the fair ratio.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of optimism and caution around Entergy leaves you on the fence, it is worth moving quickly to weigh the upside against the risks and form your own view with 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Entergy?

If Entergy has sharpened your focus, do not stop there. Broaden your watchlist now so you are not relying on a single utility story.

- Target resilient cash generators by checking out companies in the 43 high quality undervalued stocks that pair quality fundamentals with prices below intrinsic estimates.

- Prioritise stability and capital preservation by reviewing stocks in the 74 resilient stocks with low risk scores that score well on balance sheet strength and business risk.

- Spot potential early movers by scanning the 22 elite penny stocks with strong financials where smaller companies show healthier financial profiles than many investors expect.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com