- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Target's Stock Is Up Over 30% This Year. Is It Still a Good Buy?

Key Points

Target's growth has been looking strong in recent quarters.

The company, however, has also been going up against some soft performances in recent years.

The stock's valuation remains incredibly light compared to Walmart.

In recent years, Target (NYSE: TGT) has struggled to win over investors, with its larger rival Walmart being the hotter buy. But this year, the tide seems to have turned, with the former rising by around 33% and the latter being up just 2%.

What's behind Target's sudden surge this year, and can this trend continue? Here's a closer look at whether the retail stock is still a good buy right now, or if it may be running out of steam.

Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a "Double Down" signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same "Total Conviction" signal is flashing for a company 1/100th the size of Nvidia. Continue »

Image source: Getty Images.

Target's improving growth rate doesn't tell the whole story

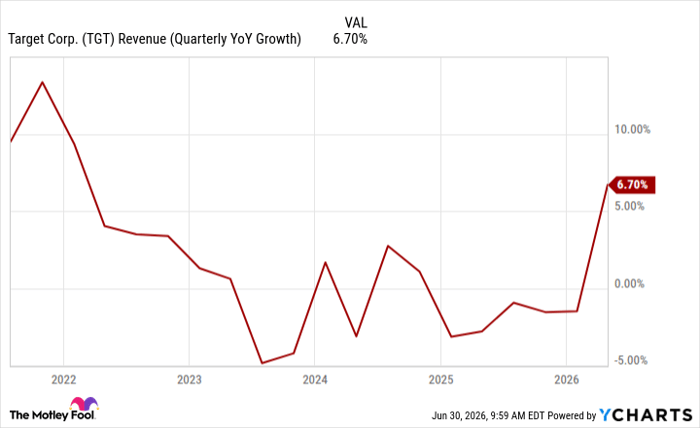

A major problem for Target in recent years has been a lack of consistent growth. Unlike Walmart, it relies more heavily on discretionary purchases, so when the economy isn't in great shape, the business isn't likely to do well. That being said, the economy arguably isn't doing all that well now, and yet, Target's growth rate has been rising, as you can see from the chart below.

TGT Revenue (Quarterly YoY Growth) data by YCharts

The recent results may look impressive and have you thinking that new CEO Michael Fiddelke, who took over this year, may have fixed what has been ailing the business. But the reality is that changes in management are unlikely to solve problems this quickly. The reality is that Target has been going up against some particularly soft numbers, so while it has been generating some positive growth, that's also after many periods of declining sales.

In its most recent quarterly results, which went up until May 2, net sales totaled $25.4 billion. While that's up nearly 7% from a year ago, that's barely any improvement from the $25.3 billion in revenue that it reported just three years earlier.

The stock's valuation may have more to do with its impressive gains this year

Target has been a much cheaper stock to own than Walmart, and it hasn't even been close. Even as of now, Target's stock is trading at just 17 times its trailing earnings versus a multiple of 40 for Walmart. Its low valuation may be the big reason for Target being a hotter buy relative to its rival this year, as the delta between the two stocks has been massive, and I believe, unwarranted.

For long-term investors, Target's stock may still be the better option to consider these days. Although its growth rate may not be as impressive in future quarters as it laps its current results, in the long run, as economic conditions improve, it should get back to generating much better numbers. With its value still being fairly modest, it may still be a good stock to add to your portfolio and hold on to for the long haul.

David Jagielski, CPA has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Target and Walmart. The Motley Fool has a disclosure policy.