- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Does nVent Electric’s (NVT) Russell Growth Inclusion Reframe Its Electrification And AI Infrastructure Narrative?

- In late June 2026, nVent Electric plc (NYSE:NVT) was added to several Russell growth benchmarks, including the Russell 1000 Growth, 3000 Growth, 2500 Growth, Midcap Growth, Small Cap Comp Growth, and 3000E Growth indices.

- This broad inclusion across the Russell growth family strengthens nVent Electric’s presence in key institutional portfolios and may increase passive fund ownership tied to these benchmarks.

- Next, we’ll examine how this broad Russell growth index inclusion could influence nVent Electric’s existing investment narrative around electrification and AI infrastructure.

Find 44 companies with promising cash flow potential yet trading below their fair value.

nVent Electric Investment Narrative Recap

To own nVent, you have to believe in its role as a core enabler of electrification and AI data center infrastructure, with execution and capital allocation as the main swing factors. The broad June 2026 Russell growth index additions increase visibility and potential passive ownership, but they do not materially change the key near term catalyst around AI and power infrastructure spending, nor the main risk from concentration in these high-growth, potentially cyclical end markets.

The most relevant recent development alongside the index adds is the leadership transition in the finance organization, with a new Chief Accounting Officer taking over in September 2026. For a company investing heavily in acquisitions and capacity, this type of role is central to managing integration risk and maintaining reporting quality, both of which matter for how investors weigh nVent’s backlog driven growth story against the risk of margin pressure.

Yet beneath the strong electrification and AI narrative, one risk investors should be very aware of is how quickly hyperscalers could move to in house solutions if...

Read the full narrative on nVent Electric (it's free!)

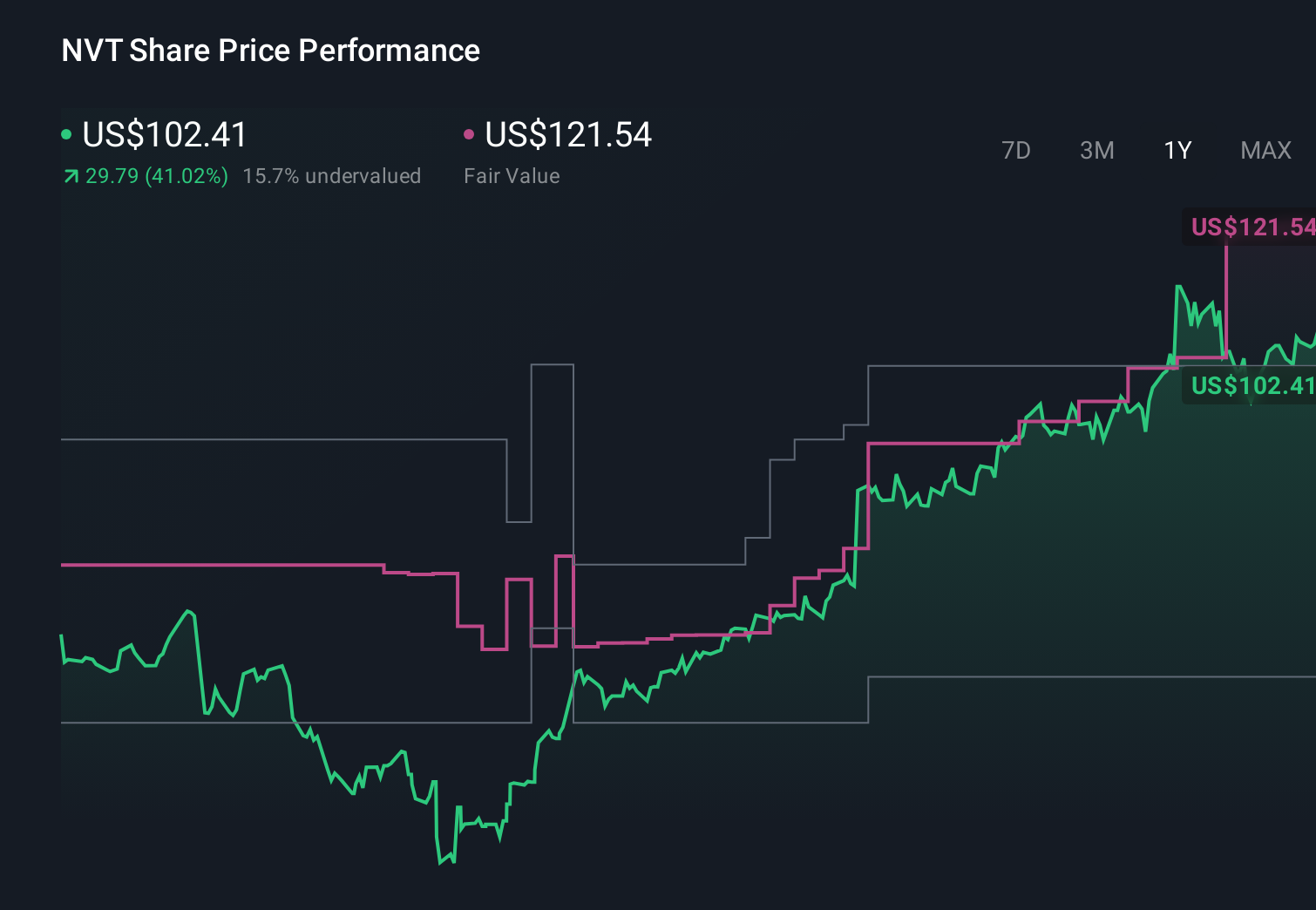

nVent Electric's narrative projects $6.7 billion revenue and $995.2 million earnings by 2029.

Uncover how nVent Electric's forecasts yield a $185.79 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts are far more cautious than consensus, even before this index news, assuming revenue of about US$5.8 billion and earnings of roughly US$842.0 million by 2029, which frames a very different risk profile than the current AI and electrification optimism.

Explore 5 other fair value estimates on nVent Electric - why the stock might be worth 38% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your nVent Electric research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free nVent Electric research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate nVent Electric's overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com