- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

The Bull Case For Federated Hermes (FHI) Could Change Following New Active ETF Launches Learn Why

- Earlier in June 2026, Federated Hermes, Inc. launched two actively managed ETFs, the Ultrashort Bond ETF (CBOE: FUSD) and the International Leaders ETF, expanding its fixed income and international equity offerings and leveraging its existing sector expertise.

- These product launches highlight Federated Hermes’ push to build scale in actively managed ETFs, adding short-duration bond and international value equity tools alongside its established money market and mutual fund franchise.

- We’ll now explore how this expansion into ultrashort bond and international equity ETFs reshapes Federated Hermes’ investment narrative and growth drivers.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Federated Hermes Investment Narrative Recap

To own Federated Hermes, you need to be comfortable with an active asset manager that still leans heavily on its money market franchise while trying to broaden its toolkit. The new ultrashort bond and international equity ETFs modestly support the near term growth story, but do not change the central risk that fee pressure and competition from low cost passive products could weigh on margins if organic growth lags.

Among the latest moves, the Federated Hermes Ultrashort Bond ETF (FUSD) looks most aligned with current catalysts, because it extends the firm’s existing US$42.9 billion short duration fixed income capability into the ETF wrapper. That gives Federated Hermes another way to participate in demand for income and cash management solutions without relying solely on traditional funds, while still leaving it exposed to the broader risk of fee compression and intense ETF competition.

However, investors should also be aware that greater reliance on fee sensitive active ETFs could leave Federated Hermes more exposed if...

Read the full narrative on Federated Hermes (it's free!)

Federated Hermes’ narrative projects $2.0 billion revenue and $422.1 million earnings by 2029.

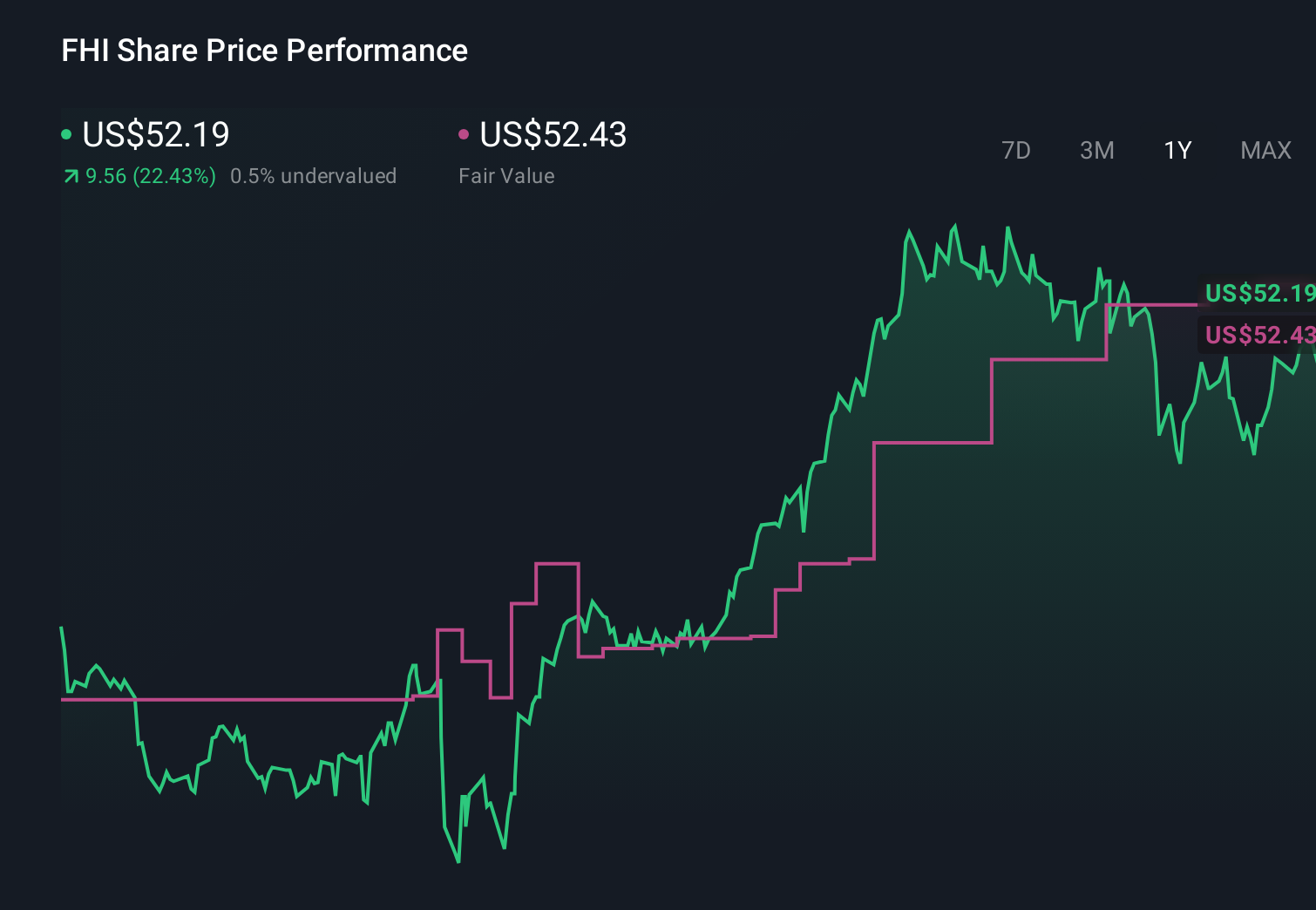

Uncover how Federated Hermes' forecasts yield a $55.00 fair value, a 4% downside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community valuations for Federated Hermes span roughly US$52 to US$70 per share, showing how far apart individual assessments can sit. As you weigh those views against the push into actively managed ETFs and the ongoing risk of fee compression, it is worth comparing several perspectives before forming your own stance.

Explore 3 other fair value estimates on Federated Hermes - why the stock might be worth as much as 21% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Federated Hermes research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Federated Hermes research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Federated Hermes' overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 30 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com