- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

United Parks & Resorts (PRKS) On Russell Index Exit And The Valuation Debate

United Parks & Resorts (PRKS) recently dropped out of several Russell value and small cap indices, an event that can shift how index funds and benchmark-aware investors approach the stock.

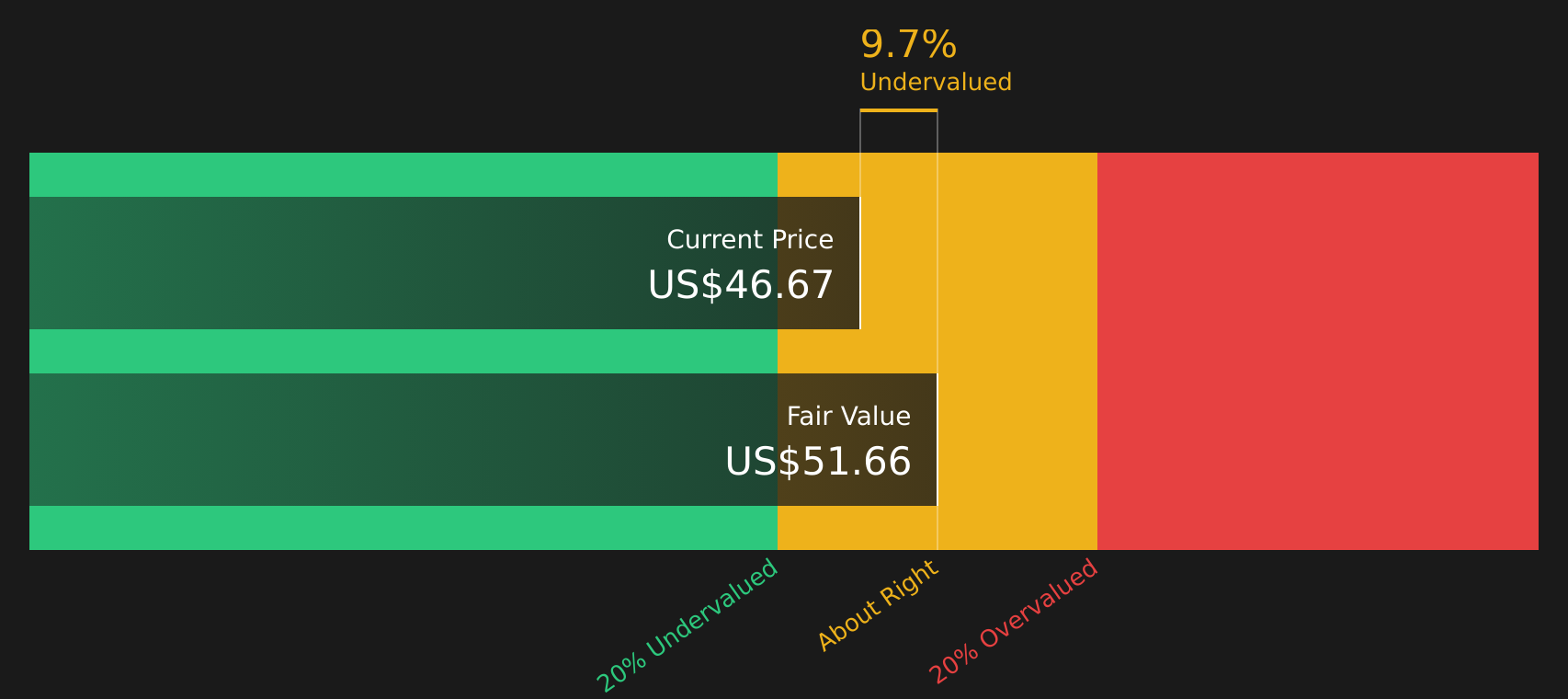

See our latest analysis for United Parks & Resorts.

At a share price of $47.12, United Parks & Resorts has seen strong recent momentum, with a 30 day share price return of 17.42% and a 90 day share price return of 44.27%. However, the 1 year total shareholder return is broadly flat and longer term total shareholder returns over 3 and 5 years are weaker, which hints that some investors may be reassessing both future growth potential and risk after its removal from several Russell value and small cap indices.

If the index changes around United Parks & Resorts have you rethinking your watchlist, it could be a good moment to broaden your search with 20 top founder-led companies

So with United Parks & Resorts trading above the average analyst price target yet screening at an estimated 22% intrinsic discount, should you see this as mispricing to exploit, or as a sign that the market already expects stronger growth?

Most Popular Narrative: 6.9% Overvalued

Compared with the last close of $47.12, the most followed narrative places United Parks & Resorts fair value at $44.09, using a detailed long term earnings and cash flow framework.

The analysts have a consensus price target of $57.455 for United Parks & Resorts based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $81.0, and the most bearish reporting a price target of just $46.0.

Want to see what sits behind that wide range of outcomes? The narrative leans on measured revenue gains, thicker margins and a higher future earnings multiple. The exact mix of growth, profitability and discounting assumptions might surprise you.

Result: Fair Value of $44.09 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, United Parks & Resorts still faces pressure from softer recurring revenue signals and higher promotion and operating costs, which could challenge the current narrative of overvaluation.

Find out about the key risks to this United Parks & Resorts narrative.

Another View: United Parks & Resorts Through Earnings Multiples

The SWS DCF model points to United Parks & Resorts trading at an estimated 21.5% discount to a $60.06 fair value, which stands in clear contrast to the 6.9% overvaluation signal from the narrative based on long term earnings and cash flow assumptions. Which framework do you find more convincing when those inputs differ so much?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With mixed signals on fair value and sentiment around United Parks & Resorts, it helps to see the evidence for yourself and decide where you stand. If you want a balanced snapshot of what investors see as the key upsides and downsides right now, take a look at the 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond United Parks & Resorts?

If United Parks & Resorts has sharpened your focus on valuation and risk, do not stop here. Expand your opportunity set with focused stock ideas.

- Spot potential bargains early by scanning screener containing 19 high quality undiscovered gems that pair solid fundamentals with lower market attention.

- Strengthen your core holdings with solid balance sheet and fundamentals stocks screener (48 results) that prioritize financial resilience and dependable fundamentals.

- Aim for steadier returns by reviewing 69 resilient stocks with low risk scores designed to help keep overall portfolio volatility in check.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com