- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

How Investors Are Reacting To Woodward (WWD) Russell Growth Reclassification And Dividend Declaration

- In late June 2026, Woodward, Inc. was shifted across multiple Russell indexes, moving into several growth benchmarks while being removed from corresponding value benchmarks, and also confirmed a quarterly cash dividend of US$0.32 per share payable on September 3, 2026 to shareholders of record on August 20, 2026.

- This broad reclassification toward growth indexes could reshape how quantitative and index-linked investors view Woodward, potentially affecting trading flows and the shareholder base more than the routine dividend declaration.

- Next, we’ll examine how Woodward’s broad move into Russell growth indexes reshapes its existing investment narrative and perceived growth profile.

AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Woodward Investment Narrative Recap

To own Woodward, you have to believe its aerospace and industrial control technologies can keep benefiting from decarbonization, electrification, and long-lived aftermarket demand, while heavy capex and integration efforts are managed without eroding margins or cash flow. The broad shift from Russell value to growth indexes does not materially change those fundamentals in the near term, but it could influence short term trading around the key catalyst of execution on new programs and the persistent risk of supply chain and capital intensity missteps.

The most relevant recent announcement is Woodward’s confirmed quarterly cash dividend of US$0.32 per share, payable on September 3, 2026. For investors focused on the company’s growth reclassification, this steady dividend policy provides a counterbalance, reminding you that the investment case is not only about multiple expansion or index flows, but also about Woodward’s ability to convert its electrification and aerospace backlog story into distributable cash while funding its elevated capex and acquisitions.

Yet beneath the growth reclassification, investors should also be aware of how heavy upcoming manufacturing investments could pressure cash flows and margins if returns underperform...

Read the full narrative on Woodward (it's free!)

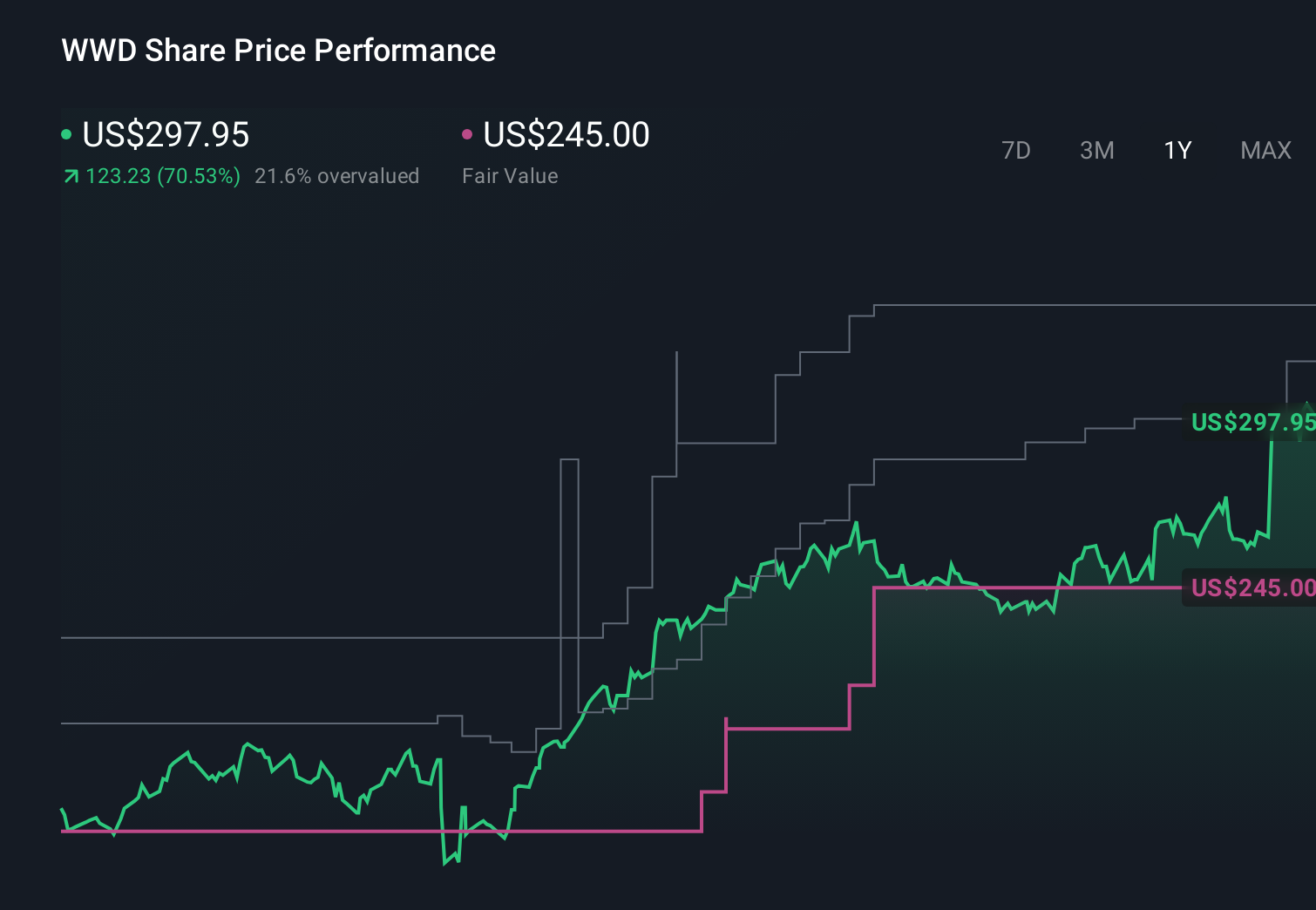

Woodward’s narrative projects $4.9 billion revenue and $719.4 million earnings by 2029. This requires 9.1% yearly revenue growth and about a $230.7 million earnings increase from $488.7 million today.

Uncover how Woodward's forecasts yield a $421.33 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling earnings near US$885.7 million by 2029, and if they are right, this growth reclassification plus rising electrification pressure on legacy products could either reinforce or challenge that bullish view, reminding you that reasonable investors can look at the same numbers and reach very different conclusions.

Explore 6 other fair value estimates on Woodward - why the stock might be worth as much as $437.09!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Woodward research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Woodward research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Woodward's overall financial health at a glance.

No Opportunity In Woodward?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com