- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

How Investors May Respond To Coty (COTY) Moving From Russell 1000 To Russell 2000 Indexes

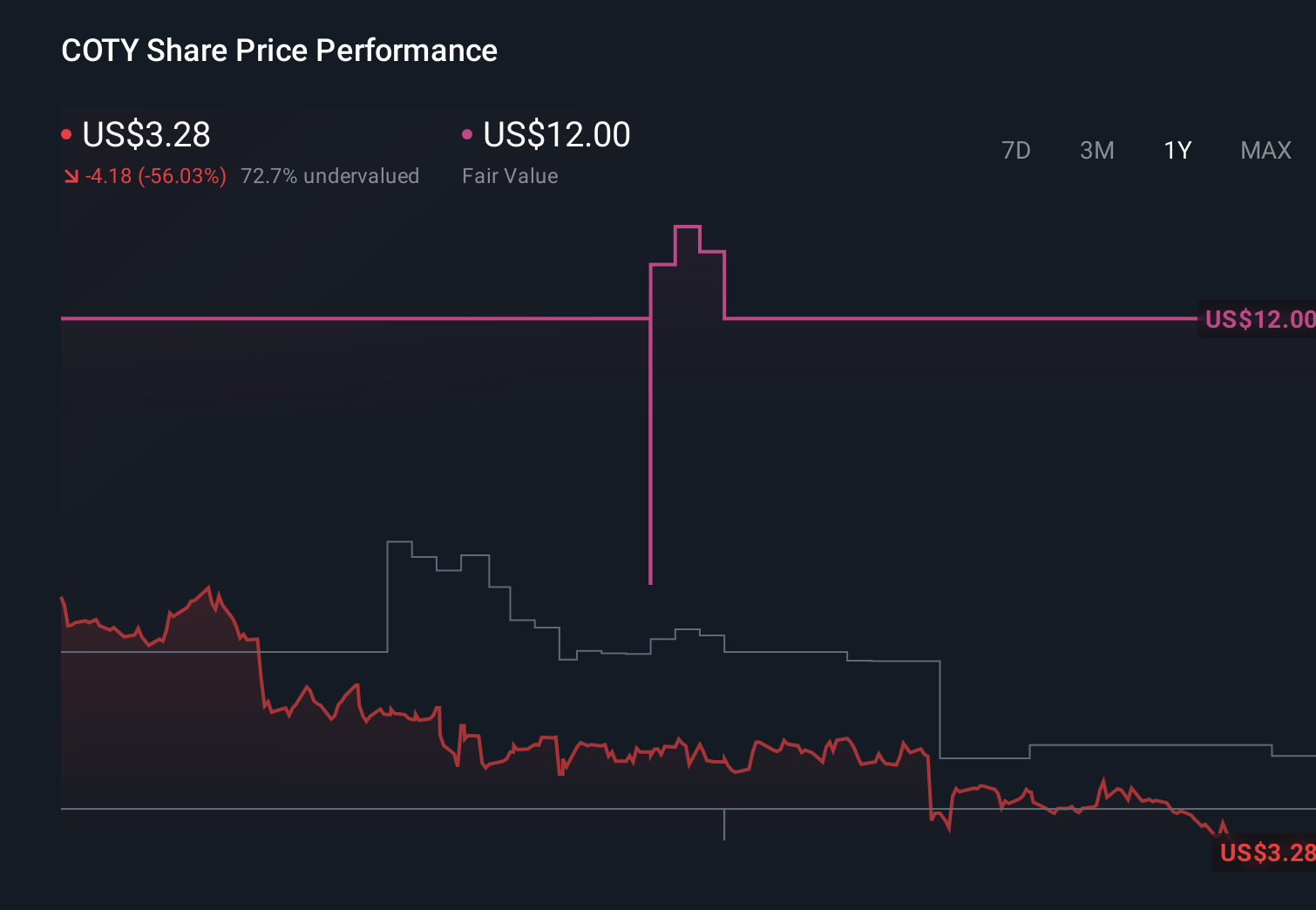

- Coty Inc. (NYSE:COTY) was removed from the Russell 1000, Russell Midcap, and related value benchmarks and added to the Russell 2000, Russell 2000 Dynamic, and Russell 2000 Value indexes in the latest Russell index rebalancing on 27 June 2026.

- This shift effectively reclassifies Coty from a larger-cap to a smaller-cap value constituent, potentially changing which index-tracking and benchmark-aware investors hold the stock.

- We’ll now explore how Coty’s move from the Russell 1000 to the Russell 2000 could influence its existing investment narrative.

Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

Coty Investment Narrative Recap

To own Coty today, you need to believe its fragrance and beauty brands can convert innovation and premiumization into sustainable profitability despite ongoing losses and slow revenue growth. The Russell index shift itself does not change the core near term story: progress on retailer destocking and margin recovery remains the key catalyst, while high leverage and refinancing needs still look like the most immediate risk.

The index move lands just months after Coty refreshed its board with five new independent directors and transitioned to an interim CEO, Markus Strobel. That governance reset could prove important if the smaller cap classification alters Coty’s shareholder base or raises pressure to accelerate decisions on debt reduction, portfolio focus, and underperforming Consumer Beauty assets.

Yet beneath the index reshuffle, investors should be aware of how Coty’s high debt load could limit its flexibility if...

Read the full narrative on Coty (it's free!)

Coty's narrative projects $5.9 billion revenue and $411.8 million earnings by 2029. This assumes fairly flat yearly revenue and an earnings increase of about $957.6 million from -$545.8 million today.

Uncover how Coty's forecasts yield a $3.17 fair value, a 65% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were projecting revenue of about US$6.2 billion and earnings near US$688.6 million by 2029, which contrasts sharply with concerns about continued retailer destocking and uneven regional performance; with Coty’s shift into smaller cap indexes, you should expect that both the bullish and cautious narratives may need revisiting as new information comes through.

Explore 5 other fair value estimates on Coty - why the stock might be worth just $3.13!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Coty research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Coty research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Coty's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

- Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com