- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Will New Morningstar Houlihan CLO Benchmarks Redefine Houlihan Lokey's (HLI) Role in Private Credit?

- On 24 June 2026, Morningstar, Inc. announced a collaboration with Houlihan Lokey to create the Morningstar Houlihan CLO Indexes, a new suite of daily valuation benchmarks for collateralized loan obligations.

- This partnership blends Morningstar’s index design and governance with Houlihan Lokey’s credit and valuation expertise to offer investors clearer performance and risk benchmarks in a growing corner of private credit.

- We’ll now examine how this new CLO index suite, built on Houlihan Lokey’s valuation framework, may influence the company’s broader investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Houlihan Lokey Investment Narrative Recap

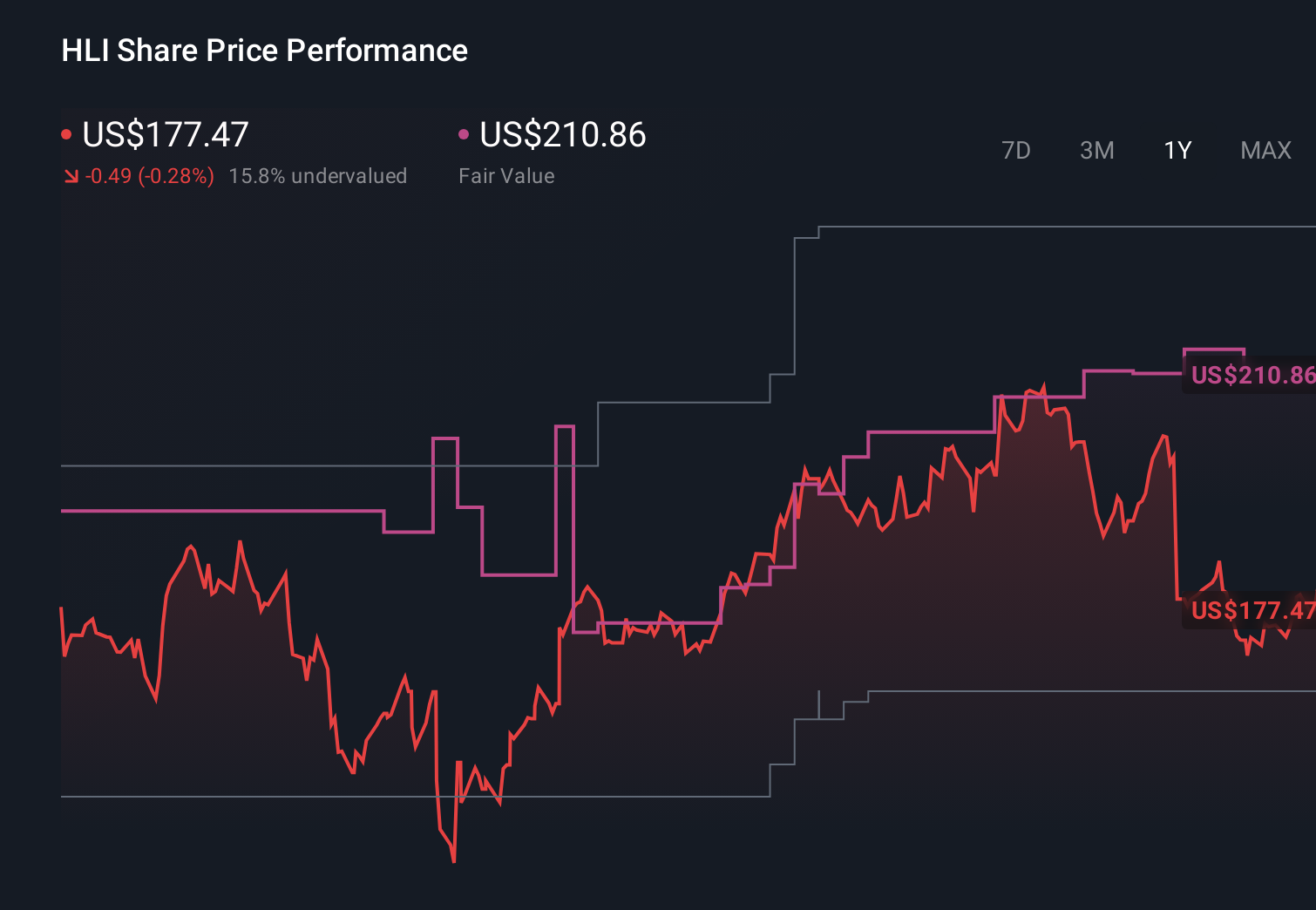

To own Houlihan Lokey, you need to believe it can keep monetizing its advisory and valuation expertise across cycles while managing high compensation and macro‑driven deal volatility. The Morningstar CLO index collaboration reinforces its valuation credentials in private credit, but does not materially change the near term dependence on M&A recovery or the cost base risk that could pressure margins if revenue growth slows.

The recent dividend increase to US$0.70 per share, alongside ongoing buybacks totaling about US$269.7 million since 2022, stands out in this context. It signals confidence in cash generation and capital return capacity even as earnings growth remains modest and restructuring revenues may normalize, framing the CLO index partnership as another potential support to fee stability rather than a primary earnings catalyst.

Yet beneath this, investors should still weigh how rising costs and uneven global deal activity could quietly reshape Houlihan Lokey’s margin profile over time...

Read the full narrative on Houlihan Lokey (it's free!)

Houlihan Lokey’s narrative projects $3.6 billion revenue and $583.7 million earnings by 2029. This requires 11.0% yearly revenue growth and about a $158 million earnings increase from $425.7 million today.

Uncover how Houlihan Lokey's forecasts yield a $172.50 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Viewed against the Morningstar CLO tie up, the more pessimistic analysts who saw revenue reaching only about US$3.5 billion and earnings around US$636.0 million by 2029 highlight how much opinions differ and why it is worth comparing that cautious view on commoditization and fee pressure with more optimistic takes.

Explore 2 other fair value estimates on Houlihan Lokey - why the stock might be worth as much as 42% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Houlihan Lokey research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free Houlihan Lokey research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Houlihan Lokey's overall financial health at a glance.

Want Some Alternatives?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com