- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Carrier Global (CARR) Could Be 4% Undervalued As Europe Leadership Changes

Leadership transition at Carrier Global’s European climate unit

Carrier Global (CARR) has drawn fresh attention after appointing Thomas Donato as President of Climate Solutions Europe, succeeding Thomas Heim, whose tenure included integrating Viessmann Climate Solutions into the wider business.

The change comes at a time when Climate Solutions Europe contributes a meaningful share of Carrier Global’s US$21.9b in revenue. This is prompting investors to consider how Donato’s industrial technology background might influence priorities across the European HVAC and energy solutions portfolio.

See our latest analysis for Carrier Global.

Carrier Global’s recent appointment at Climate Solutions Europe comes against a backdrop of strong share price momentum, with a 30 day share price return of 14.08% and a 90 day share price return of 35.65%. The 5 year total shareholder return of 62.22% shows how the stock has rewarded longer term holders, despite a more modest 1 year total shareholder return of 1.36%.

If this kind of energy transition story interests you, it could be a useful moment to look across the sector and scan 35 power grid technology and infrastructure stocks

With Carrier Global stock showing strong recent returns and trading only slightly below analyst price targets, yet with a modelled intrinsic discount still flagged, the key question is whether there is genuine value left or if the market is already pricing in future growth.

Most Popular Narrative: 3.6% Undervalued

Carrier Global’s most followed narrative puts fair value at $76.31, only slightly above the last close at $73.59. This keeps the focus on what is driving that gap rather than a dramatic mispricing call.

Carrier's introduction of differentiated products, such as air-cooled commercial heat pumps and the integration of HEMS technology with Google Cloud's AI, positions them to capture the growing demand for sustainable and smart energy solutions, potentially driving future revenue growth.

Want to see what sits behind that fair value line? The narrative leans heavily on compounding revenue, rising margins and a future earnings profile that needs a higher quality multiple. The specific mix of growth, profitability and discount rate assumptions may surprise you.

Result: Fair Value of $76.31 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Carrier Global’s thesis still leans on assumptions that could be tested if European margins remain under pressure or if tariff exposure and FX swings weigh more heavily on earnings.

Find out about the key risks to this Carrier Global narrative.

Another View on Carrier Global’s Valuation

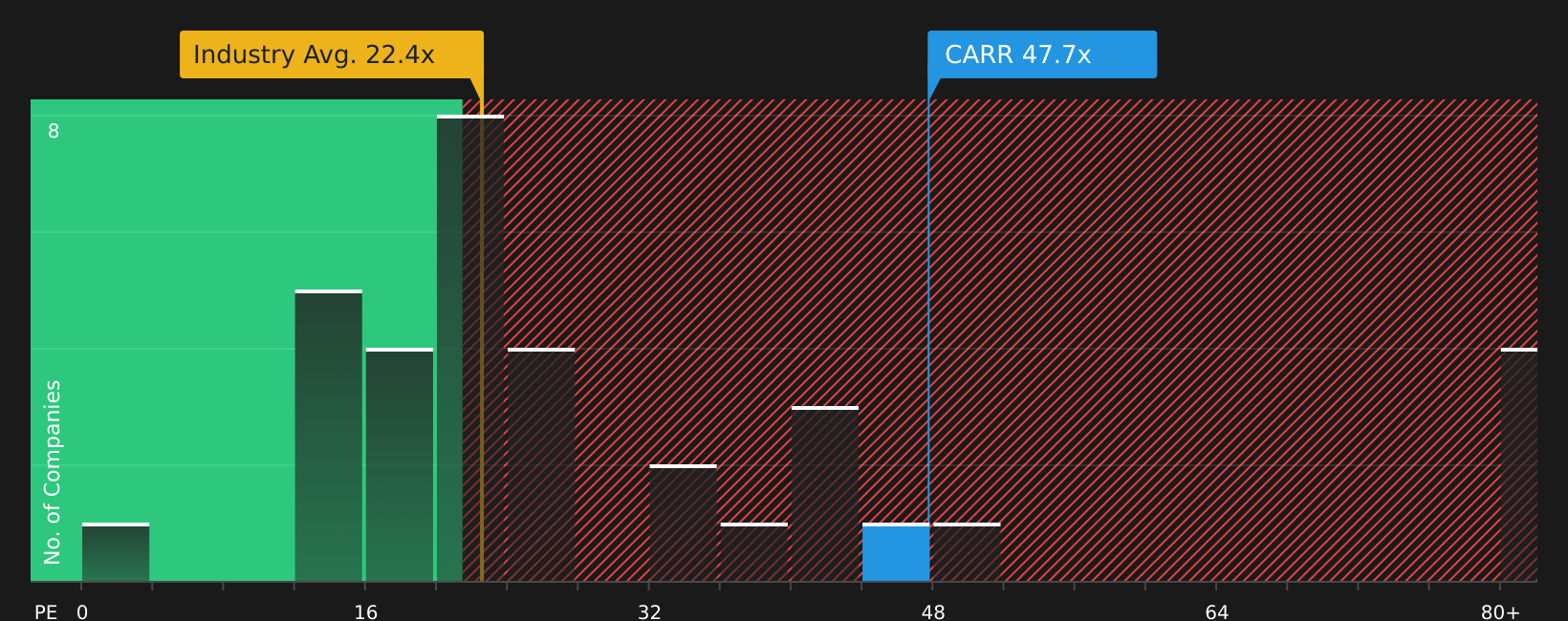

The first take on Carrier Global leans on fair value estimates that point to a 3.6% discount, but the earnings multiple tells a different story. The stock trades on a P/E of 47.7x, versus 22.2x for the US Building industry and a fair ratio of 38.8x. That gap suggests investors are already paying a premium, so how comfortable are you with that extra valuation risk if expectations are tested?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Given the mix of optimism and caution around Carrier Global, it makes sense to look past the headlines and examine the data directly. To weigh those cross currents properly, review the balance of potential upside and downside by checking the 2 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Carrier Global?

If you like the Carrier Global story but do not want to rely on a single stock, it is worth lining up a few more ideas on your watchlist.

- Target potential mispricings early by scanning 44 high quality undervalued stocks that combine solid fundamentals with prices that may not fully reflect their current profile.

- Strengthen your income stream by reviewing 8 dividend fortresses that focus on higher yielding payouts from companies with established distributions.

- Reduce portfolio stress by filtering for 71 resilient stocks with low risk scores that prioritize resilient balance sheets and steadier risk scores over short term excitement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com