- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

NVIDIA Stock Leads 3 High ROE Picks Backed By Strong Balance Sheets

Global inflation, shifting central bank policies and uneven consumer trends are pushing many investors to focus on quality first. In this setting, stocks with high return on equity, resilient past performance and solid balance sheets can help you stay focused on fundamentals instead of short term headlines. This article looks at three stocks from the Solid Balance Sheet and Fundamentals screener, highlighting companies that combine financial strength with efficient use of shareholder capital. You will see how this theme fits with today’s macro backdrop and which types of solid balance sheet stocks might deserve a closer look.

NVIDIA (NVDA)

Overview: NVIDIA is a US-based chip and software company that provides the computing engines behind AI data centers, gaming PCs and professional graphics, selling its GPUs and platforms to cloud providers, car makers and hardware manufacturers around the world.

Operations: NVIDIA generates about US$25.1b from its Graphics segment and around US$228.4b from Compute & Networking, with the United States contributing roughly US$187.7b of revenue and Taiwan about US$46.7b.

Market Cap: US$4,740.9b

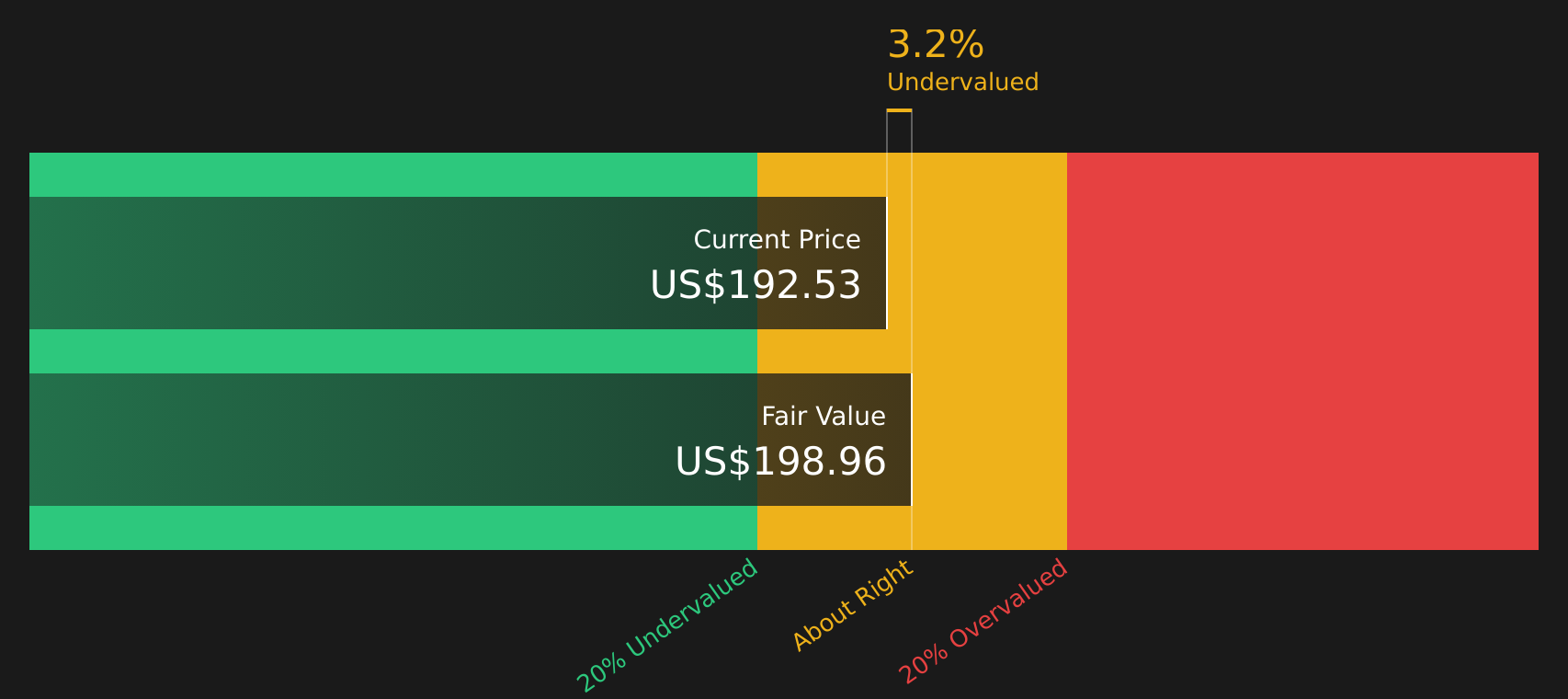

NVIDIA stands out in this screener because it combines very high profitability, with net margins around 63% and an ROE close to 81.7%, with a central role in AI infrastructure through its data center GPUs, CUDA software ecosystem and Vera Rubin platform. Forecast revenue and earnings growth are expected to run well ahead of the broader US market. Yet the P/E of 29.2x sits below both peer and sector averages and close to the Simply Wall St cash flow estimate. The story is not risk free, with heavy dependence on external funding, high non cash earnings, regulatory pressure on AI and export controls to China, plus rising competition from Broadcom and OpenAI’s Jalapeño chip. All of these factors could reshape how much value investors ultimately capture from this AI cycle.

NVIDIA’s strong margins and ROE indicate significant earning power, while its 29.2x P/E remains below peers and the sector. To evaluate whether that difference reflects potential upside or a possible risk, review the DCF valuation analysis for NVIDIA

TJX Companies (TJX)

Overview: TJX Companies is a global off price retailer that sells discounted branded apparel and homewares through banners such as T.J. Maxx, Marshalls, HomeGoods and international chains, offering a constantly changing assortment that aims to keep value focused shoppers returning regularly.

Operations: TJX generates about US$37.2b from its US Marmaxx segment, US$10.4b from US HomeGoods, US$5.8b from TJX Canada and US$8.2b from TJX International.

Market Cap: US$171.4b

TJX Companies attracts attention because it pairs a very high 55.7% ROE and rising profit margins with strong customer appetite for off price goods, reflected in broad based transaction growth, 6% comparable store sales growth in Q1 fiscal 2027 and raised full year guidance. At the same time, the stock trades on a rich earnings multiple and relies fully on external borrowing, while management and directors have sold stock recently, which are all signals investors may want to weigh carefully. Analysts expect earnings and margins to grow over time, and TJX continues to lean on its global buying scale and “treasure hunt” in store experience. The key question is whether the current valuation leaves enough room for those qualities to be rewarded.

TJX Companies has accelerating comps and a high 55.7% ROE, yet a rich earnings multiple and insider selling raise questions about what is already priced in, so walk through the 2 key rewards and 1 important warning sign

Microsoft (MSFT)

Overview: Microsoft is a global software and cloud company that sells Windows, Office and Microsoft 365, LinkedIn, Azure cloud services, GitHub, gaming through Xbox and a wide range of AI powered Copilot tools to consumers, enterprises and governments.

Operations: Microsoft generates about US$135.3b from Productivity and Business Processes, US$128.4b from Intelligent Cloud and US$54.6b from More Personal Computing, with revenue fairly balanced between the United States and other countries.

Market Cap: US$2,620.97b

Microsoft sits at the center of AI and cloud spending, pairing very high profitability with a large cash generating core in Office, Azure and Windows that is now being layered with Copilot and OpenAI powered services. At the same time, heavy capital expenditure on data centers, a funding mix reliant on external borrowings, significant insider selling and active antitrust and DMA scrutiny mean this is not a risk free story. The real question for investors is whether Microsoft’s cash flow strength and AI ecosystem justify staying patient through that regulatory and spending cycle.

Microsoft’s cash engine in Office, Azure and Windows is now tied closely to AI. However, the full trade off between heavy data center spending, regulatory scrutiny and long term opportunity is not obvious in the headline story, so walk through the analysis report for Microsoft

The three stocks in this article are just a starting point, as the full Solid Balance Sheet and Fundamentals screener highlights 45 more companies with high return on equity, resilient past performance and sound balance sheets that could have equally compelling narratives waiting to be unpacked in the Solid Balance Sheet and Fundamentals screener. Use Simply Wall St to identify and analyze the specific catalysts, risk flags and business narratives that fit your own criteria so you can focus on the highest conviction ideas for your portfolio.

Take Control of Your Investment Journey

If Microsoft or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Beyond Your Current Watchlist?

Fresh stock ideas do not stay under the radar for long, and attractive entry points can slip away while momentum is building. Acting early can help you evaluate opportunities before they become widely followed.

- Identify early momentum in smaller AI-focused companies by reviewing the curated 34 AI small caps before they are fully in the spotlight and pricing becomes more constrained.

- Explore companies with strong cash generation by using the hand picked 8 dividend fortresses while yields and fundamentals appear appealing and sentiment remains more measured.

- Take a closer look at companies involved in modernizing power infrastructure by checking the focused 35 power grid technology and infrastructure stocks while interest in this theme is still developing and attention is directed elsewhere.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com